Analysis of Price Competitiveness of Korean Tourist Cities: An International Comparison

Kwanyoung Lee, Associate Research Fellow at Yanolja Research / [email protected]

Suckwon Hong, Principal Researcher at Yanolja Research / [email protected]

Soocheong Jang, Professor at Purdue University & Director at Yanolja Research / [email protected]

Kyuwan Choi, Professor at Kyung Hee University & Director at H&T Analytics Center / [email protected]

The South Korean tourism industry stands at a significant turning point, as outbound travel demand is projected to surpass 30 million in 2026, while the country simultaneously approaches an era of 20 million inbound tourists. However, despite these quantitative growth forecasts, a widespread perception that "tourism in Korea is expensive" has taken root domestically. This perception acts as a psychological factor that stifles domestic tourism consumption and accelerates the outflow of travel demand to overseas destinations. A 2025 survey by the Federation of Korean Industries (FKI) identified "high prices at tourist destinations" as the primary reason why domestic travel is perceived as less satisfying than overseas travel. Notably, the sentiment "I might as well go to Japan for the price of a trip to Jeju Island" has emerged as a prevailing consumption frame, especially among the younger generation.

However, it is imperative for industry stakeholders and policymakers to objectively distinguish whether this "emotional perception of high prices" aligns with actual macroeconomic data and global market price indicators. While controversies over price gouging in specific regions during domestic travel are a painful reality, there is a possibility that this phenomenon is influenced by the "Availability Heuristic" from behavioral economics—where a small number of extreme negative cases are amplified by media, creating an illusion that distorts the reality of the broader market. Generalizing exceptional price spikes at popular "hot spots" during peak seasons to the fundamentals of Korea’s entire tourism infrastructure is a logical fallacy. It is akin to concluding that an entire nation's public transportation system is overpriced based solely on the cost of scalped tickets during a major holiday.

To objectively evaluate these potential biases, the most crucial step is to understand Korea's price levels from the perspective of inbound tourists. Considering the recent depreciation of the Korean Won, with the KRW/USD exchange rate fluctuating between the mid-1,400s and 1,500, the perceived price level in Korea for foreigners may differ significantly from the concerns voiced by domestic travelers.

Consequently, this report aims to empirically verify Korea's tourism price competitiveness by utilizing not only price data from global OTA but also the World Bank's price level ratio (PLI). By analyzing actual expenditure levels across different stages of the travel journey (accommodation, dining, and transportation) where tourists directly spend their money, and subsequently presenting macroeconomic price levels by country (relative to the U.S.), we intend to cross-validate Korea's travel price competitiveness in the global market from multiple angles. Through this, we aim to determine the price advantage that major domestic cities, such as Seoul and Busan, hold in the global tourism market. Furthermore, by conducting a multi-dimensional comparison with the Japanese tourism market—which has recently been at the center of controversy over the introduction of dual-pricing systems—we intend to derive the strategic competitive positioning that Korea should adopt. Additionally, based on objective data, this report examines the concerns of domestic travelers regarding travel costs—concerns often fueled by a few negative cases—and explores whether such analysis can serve as a logical foundation for creating a virtuous cycle leading to the revitalization of domestic tourism.

Micro-level Price Analysis by Travel Itinerary

Before delving into macroeconomic price indicators, the most critical metric in the tourism industry—one that immediately dictates tourist satisfaction—is the scale of direct expenditure across individual segments of the journey. Travel is a consumption chain that begins with accommodation, proceeds to transportation, and culminates in dining and shopping. The lower the cost resistance at each node of this chain, the higher a nation's actual tourism price competitiveness. However, as shopping involves a diverse array of goods, there are limitations to aggregating it into a single price level alongside accommodation, transportation, and dining. Therefore, this study aims to indirectly assess the price level of shopping by utilizing the macroeconomic price levels of the respective countries, which will be discussed later.

This study analyzes the average accommodation prices in major global tourist cities listed on the global OTA, Klook, and data on local transportation and dining costs for global travelers provided by the global cost-of-living statistics platform, Numbeo. Through this, we have analyzed how the travel costs in Seoul and Busan stand in comparison to global megacities and competing Asian cities.

Accommodation Prices: Premium Infrastructure at Competitive Rates

Accommodation costs serve as an anchor cost, accounting for 30~40% of the total travel budget. When these costs are high, tourists inevitably tend to shorten their length of stay or drastically reduce additional consumption, such as shopping and dining.

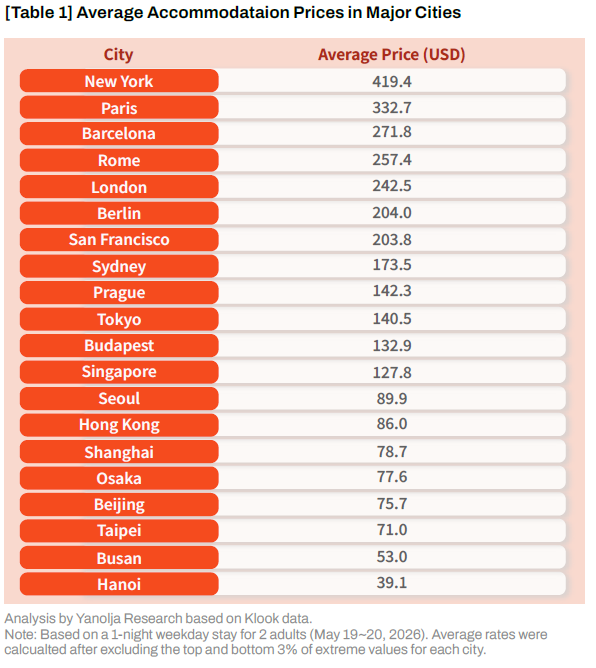

An analysis of average accommodation prices in major global tourist cities listed on Klook reveals that Seoul and Busan possess a distinct price competitive advantage compared to Western megacities, and maintain a competitive position within Asia. The data indicates that major tourist cities in the Americas and Europe demand accommodation prices that are incomparable to those of Korean cities.

New York’s average accommodation cost ($419.4) is approximately 4.7 times higher than Seoul’s ($89.9), while Paris ($332.7), Barcelona ($271.8), and Rome ($257.4) are also roughly three times more expensive than Seoul. This means that for Western tourists, the budget required for accommodation alone when traveling domestically or within neighboring European countries would be sufficient in Korea to cover airfare, plus several days of lodging and fine dining. Metaphorically speaking, in the global accommodation market, Seoul and Busan are attractive options where one can enjoy the comfort and safety of a luxury sedan at the maintenance cost of a compact car.

Within the Asian market, while Seoul’s average accommodation prices are higher than those in cities such as Taipei ($71.0), Shanghai ($78.7), Beijing ($75.7), and Hanoi ($39.1), they are over 30% lower than those in key competing cities like Tokyo ($140.5) and Singapore ($127.8), and comparable to Hong Kong ($86). Although it is true that Seoul sits at the higher end of the accommodation price spectrum within Asia, considering the world-class safety, tourism infrastructure, and service quality, its price competitiveness is excellent by international standards. Advanced amenities often provided in Korean motels or mid-range business hotels—such as large smart TVs, high-speed free Wi-Fi, and complimentary clothing care systems (e.g., Stylers)—are options rarely found even in 4-star hotels in the West. Taking these hidden value-added services into account, the actual cost-effectiveness is likely greater than what simple price indicators suggest.

The most notable data in this analysis is the average accommodation price in Busan ($53.0). Despite being South Korea’s second-largest city and a hub for marine tourism—densely packed with luxury resorts and large hotel chains—its accommodation prices were the lowest among the examined major cities, with the exception of Hanoi. This signifies that Busan is at the pinnacle of overwhelming cost-effectiveness, offering global tourists 5-star hardware on a 3-star budget. This objective data refutes the notion that local accommodation is universally expensive; it suggests that the "price gouging" perceived by domestic travelers during peak seasons or specific events is an abnormal phenomenon that does not represent the broader statistical reality.

This analysis carries significant implications for domestic travelers as well. Rather than generalizing the entire domestic accommodation market as expensive based solely on perceptions of a few famous tourist spots or peak-season hotel rates, providing average price data and global comparisons can help objectify the perception of domestic accommodation costs. Ultimately, what is important is to couple self-corrective efforts to rectify aberrant pricing behavior in certain market segments with the consistent provision of such average and comparative information to domestic consumers, thereby alleviating the distorted perception of domestic travel costs.

Public Transportation and Mobility Costs: Ultra-Low-Cost Infrastructure Fueling Tourist Mobility

Once accommodation is secured, the convenience and economic efficiency of urban mobility to reach tourist attractions become core pillars of tourism price competitiveness. Transport infrastructure functions as the circulatory system of a destination; when the “blood pressure” of travel costs rises, the tourist's range of movement narrows to the immediate vicinity of their accommodation. This obstructs the “blood flow”—the movement of tourists throughout the local community—that generates additional consumption such as shopping, dining, local experiences, and the utilization of small, neighborhood businesses. In this regard, the price competitiveness of transportation, particularly public transit, is paramount.

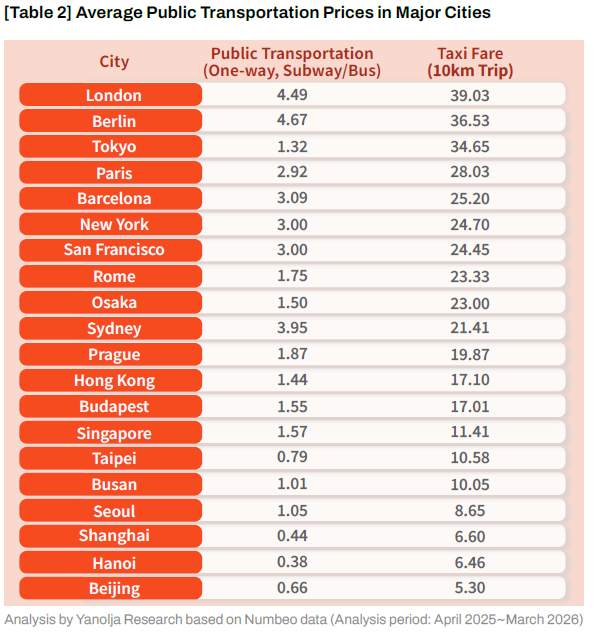

In this context, we analyzed data from Numbeo, which compiles mobility costs—including subway, bus, and taxi fares—based on experiences recorded by travelers worldwide. The analysis reveals that South Korea possesses world-class price competitiveness.

Taxi services are the primary means of handling the last mile of tourist movement. Analyzing the cost of a 10km trip (inclusive of base and distance fares), the fare systems in Seoul ($8.65) and Busan ($10.05) remain uniquely low compared to major global cities. Taxi fares in London ($39.03) and Berlin ($36.53) are approximately four times higher than in Korea, and even when compared to nearby competing cities like Tokyo ($34.65), Seoul’s taxi fares are remarkably affordable.

South Korea also demonstrates top-tier price competitiveness in one-way public transportation (subway and bus) fares. Fares in Seoul ($1.05) and Busan ($1.01) are lower than those in Tokyo ($1.32) or Hong Kong ($1.44), and hold an overwhelming advantage over major Western cities. The affordability of both public transit and taxi fares means that foreign tourists face no psychological burden in exploring every corner of Seoul and Busan. This suggests that the transportation budget saved during the trip facilitates greater spatial movement, leading to substantial additional consumption that revitalizes the local economy, thereby generating a high economic multiplier effect.

Furthermore, it is important to note that Korea's public transportation goes beyond simple affordability. It offers top-tier service quality—including cleanliness, punctuality, multilingual guidance, and free Wi-Fi—at these low fares, creating a level of competitiveness rarely found globally. With the government recently allowing the conditional overseas transfer of high-precision map data, digital barriers, such as the limitations on Google Maps’ wayfinding and navigation functionality, are gradually being resolved. Consequently, competitiveness in the mobility sector is expected to be the most effective instrument for maximizing tourism satisfaction.

Dining Costs: Price Elasticity and Hidden Value of K-Food Beyond the 'Big Mac Index'

Dining costs are an indicator that tourists experience multiple times per day, making it one of the most sensitive factors that shape overall travel satisfaction and perceived price. According to data from Numbeo, which records the cost of a single meal in general restaurants based on the experiences of travelers worldwide, dining costs in South Korea (particularly in Seoul) maintain a highly competitive level from a global perspective—including Western countries—though they occupy a relatively upper-mid-range position within the Asian market.

The cost of a meal in a typical restaurant in Seoul ($8.79) is approximately one-third of the costs in major Western cities such as London ($26.80), New York ($25.00), and San Francisco ($25.00), demonstrating clear competitiveness in absolute price levels. This structure reveals a dual price-competitiveness model, where Korean tourism functions differently in global (Western) markets versus the Asian market. For tourists from the Americas and Europe holding USD or EUR, the threshold for Korean dining is remarkably low. Furthermore, with the recent depreciation of the Korean Won to the 1,400 KRW range per US dollar, tourists can enjoy premium experiences—such as Hanwoo beef or high-end traditional Korean dining—for a price equivalent to a standard burger combo meal in their home countries.

In contrast, the landscape within the Asian market differs. Seoul’s dining cost ($8.79) is among the higher end, trailing only Singapore ($9.81) and exceeding that of Tokyo ($7.57) and Hong Kong ($7.66). It shows a significant gap when compared to major tourist cities like Taipei ($5.04), Shanghai ($4.39), and Hanoi ($2.09). A similar trend is observed in Busan ($6.76); when comparing general dining costs, Seoul averages around 13,000 KRW, while Busan averages around 10,000 KRW, placing Busan approximately 30% lower than Seoul.

However, there is a critical point that the industry must never overlook: the non-price competitiveness regarding the quality and quantity of the service provided, which is not captured by numerical data. Korea’s unique culture of complimentary side dish refills, free drinking water, and, most importantly, policies of "no tipping" and "no service charges" represents hidden value not reflected in the unit price of a single meal. In Western countries or neighboring Japan, side dishes, extra servings, or even a glass of water often incur additional fees, and it is standard practice to pay a 15–20% tip. Conversely, the Korean dining ecosystem provides these services entirely free of charge. This essentially returns economic value exceeding the numerical $8.79 to the tourist, acting as a key driver that elevates the "value-for-money" of the K-food experience to a top-tier global level. When these non-price competitive factors are integrated with the actual dining costs in Seoul and Busan, Korea can be considered to possess sufficient price competitiveness even within the Asian region.

This perspective warrants a re-evaluation by domestic travelers as well. While dining costs may feel high in certain instances, when compared to overseas markets based on the total Cost of Dining Experience—which includes tips, service charges, and other hidden incidental costs—dining in Korea still holds strong competitiveness. Therefore, if domestic travelers approach this not merely by looking at nominal prices but through the lens of the total cost of the dining experience, there is little ground to evaluate domestic dining costs as excessively high. In other words, even when looking strictly at food, it is inaccurate to categorize the current pricing as a rip-off.

Macroeconomic Price Indicator Comparative Analysis

Having confirmed price competitive advantage of Korea tourism at the micro-level across accommodation, transportation, and dining, we now aim to determine whether this phenomenon stems from fundamental macroeconomic fundamentals of the nation rather than specific industries or short-term events. For this purpose, we have examined the World Bank’s macroeconomic data, the “Price Level Index,” alongside recent trends in exchange rates, which serve as a key macroeconomic variable.

The Objective Status of Korean Prices as Reflected by the PLI

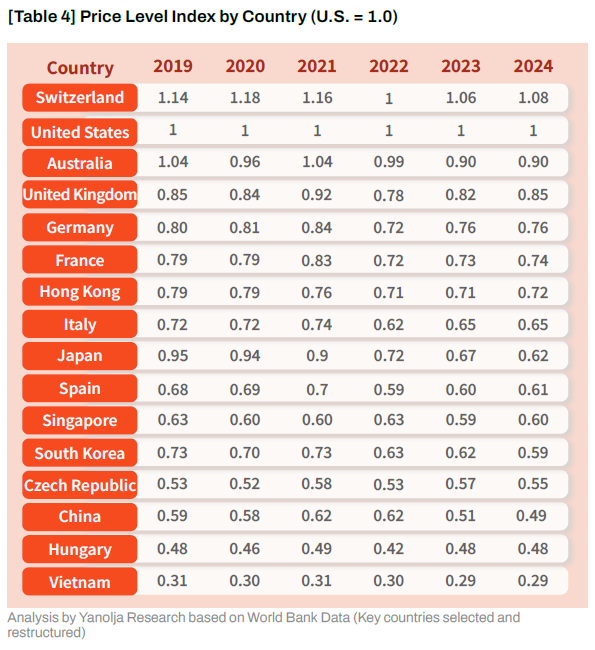

The most reliable indicator for discussing Korea's tourism price competitiveness is the Price Level Index (PLI)—the price level ratio of the PPP conversion factor to the market exchange rate index—published by the World Bank. This index quantifies the overall price level of each country based on the United States (index = 1.0), intuitively demonstrating the cost of purchasing the same goods and services in a specific country relative to the U.S.

A critical feature of this index is that it directly reflects changes in market exchange rates. While the Purchasing Power Parity (PPP) exchange rate is calculated based on the actual price level of identical products and services within each country, the market exchange rate fluctuates according to global financial market factors—such as supply and demand in foreign exchange markets, U.S. Federal Reserve interest rate policies, and geopolitical risks. Therefore, even for a country with the same price level, if the exchange rate rises, the PLI will decline. From this perspective, the PLI serves as the most objective indicator representing the real price level experienced by foreign tourists.

As of 2024, South Korea recorded a PLI of 0.59. This signifies that the economic utilityobtained for $1 in New York or Los Angeles can be enjoyed in Seoul or Busan for an exceptionally low cost of approximately $0.59. Korea maintains a level firmly lower than Western developed nations such as Switzerland (1.08), Australia (0.90), the United Kingdom (0.85), Germany (0.76), and France (0.74), as well as key Asian competitors like Hong Kong (0.72), Japan (0.62), and Singapore (0.60).

Contrary to the self-deprecating complaints of some domestic travelers on social media claiming that Korean prices are the most expensive in the world or are murderous, these macroeconomic indicators—which synthesize purchasing power and market exchange rates—quantitatively prove that South Korea holds a solid low-price advantage among major global tourism competitors. In particular, the fact that Korea’s index is lower than those of representative European tourist destinations such as France (0.74), Italy (0.65), and Spain (0.61) indicates that the real purchasing power experienced by tourists from the Americas or Europe is significantly amplified when visiting Korea.

Macroeconomic Booster Effect in the Era of High Exchange Rates: Driving Inbound Tourism

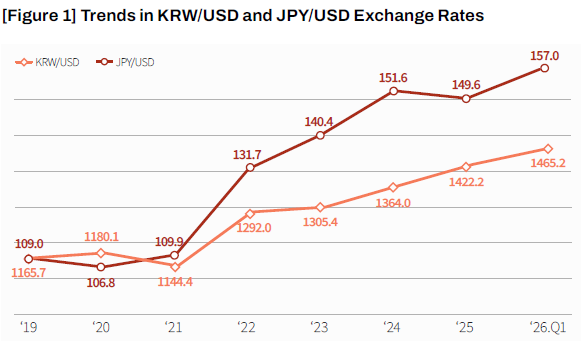

A time-series analysis of the data reveals that Korea's price competitiveness has strengthened after COVID-19. Korea’s PLI, which stood at approximately 0.73 in 2019, fell to 0.59 in 2024, representing a substantial decline of 19%. The underlying driver of this rapid change is the macroeconomic trend of Won depreciation. The recent KRW/USD exchange rate has entered an unprecedented phase of a “high exchange rate and strong dollar,” currently hovering in the mid-to-high 1,400 KRW range. Although ceasefire discussions are underway in the Middle East, a complex interplay of factors—including rising oil prices due to the fallout from the U.S.-Iran conflict, a retreat in expectations for interest rate cuts by the U.S. Federal Reserve, and the concentration of foreign investment in the U.S. driven by the global Artificial Intelligence (AI) boom—suggests the possibility that this high exchange rate in the 1,400 KRW range may be solidifying into a new normal.

In fact, during the same period, the JPY/USD exchange rate peaked at 152 JPY in 2024, declined to 150 JPY in 2025, and has shown signs of increasing again in the first quarter of 2026. However, the KRW/USD exchange rate has continued to face depreciation pressure, rising further from an annual average of 1,364 KRW in 2024 to 1,422 KRW in 2025, and to 1,465 KRW in the first quarter of 2026. This indicates that the trend of strengthening the Won's price competitiveness is becoming structurally more entrenched.

It is an undeniable reality that high exchange rates act as a severe burden on domestic industries struggling with rising import costs and on students abroad who must remit living expenses. The duty-free sector, in particular, is facing significant hardships as the surge in KRW-denominated prices for dollar-based goods has led domestic consumers to tighten their spending. However, when viewing this phenomenon through the lens of inbound tourists, it is akin to the issuance of an invisible global discount coupon that effectively puts the entire nation on a 30% clearance sale—reminiscent of the late 1990s, when the tourism industry emerged as a vital means of securing foreign currency during the financial crisis.

The moment a tourist holding USD, EUR, or CNY opens a wallet in Gangnam or Myeong-dong, the depreciation of the KRW inflates the value of their $100 from 110,000 KRW to over 140,000 KRW. This drastically reduces the real, dollar-denominated prices of nearly all goods and services—including dining, accommodation, K-Beauty, and medical/wellness tourism—serving as a catalyst that makes Korea’s travel costs, as analyzed earlier, appear even more affordable to foreign visitors.

In short, we must not dismiss the weak Won as merely an economic crisis. Instead, we should actively promote Korea’s price competitiveness to navigate the waves of global inflation, dramatically improve the tourism balance, and utilize this currency situation as a strategic booster to accelerate the era of 20 million inbound tourists. Furthermore, this should serve as a pivotal turning point for domestic travelers as well; by highlighting the surge in the perceived cost of overseas travel due to the high exchange rate, it can help mitigate the tourism deficit while encouraging a fact-based re-evaluation of the economic viability of domestic travel.

A Multi-dimensional Comparison with the Japanese Tourism Industry and Korea’s Positioning

Currently, the most formidable competitor and benchmark for the Asian tourism market—particularly for Korea’s inbound and outbound industries—is undoubtedly Japan. Weaponizing the historic weakness of the Yen, Japan has attracted over 30 million foreign tourists annually, effectively elevating tourism to the nation's second-largest export industry. As previously noted, it is not uncommon to witness Korea’s younger generation turning away from domestic travel, claiming, "I’d rather go to Japan with that money than visit the expensive Jeju Island". However, a closer examination of the relevant information and data reveals that these established perceptions may be flawed, or that the local situation in Japan is gradually changing. Recently, the introduction of a dual-pricing system within Japan is creating opportunities for the Korean tourism market to benefit from a rebound effect.

South Korea: Still More Affordable Than Japan Based on Macroeconomic Indicators

The public belief that Japan is cheaper than Korea is likely a psychological frame formed by the dramatic media coverage of Japan's long-standing deflation and the weak Yen. As confirmed in Table 4, even though Japan's PLI fell to an all-time low of 0.62 in 2024, it still records a higher figure than South Korea's (0.59).

The gap widens significantly when looking at micro-level travel expenditures. As evidenced by our previous analysis of public transportation fares (10km taxi ride: Seoul $8.65 vs. Tokyo $34.65) and accommodation costs (Seoul $89.9 vs. Tokyo $140.5), Japan's key metropolitan tourist destinations are by no means cheaper than Korea's. The perception that Japan is cheap is merely limited to specific, narrow consumption categories, such as convenience store bento boxes or certain chain pubs. In terms of average national tourism price competitiveness, Korea maintains a clear advantage.

Therefore, to divert domestic outbound travel demand back to the domestic market, we must not simply appeal to patriotic consumption. Instead, we must consistently present empirical data comparing accommodation, transportation, and dining costs between Korea and Japan, empowering consumers to make more rational decisions. Only by doing so can we move beyond the simplistic frame that "domestic is unconditionally expensive and Japan is unconditionally cheap," allowing tourism destination choices to be made based on economic facts rather than distorted perceptions.

The Side Effects of Overtourism in Japan and the Backlash of Dual Pricing Policies

Even more critical is the recent approach by Japanese local governments to address overtourism, which has arisen from an influx of tourists exceeding the capacity of local infrastructure. As damage to local communities continues to mount, Japan has begun erecting barriers of discriminatory pricing targeting foreign tourists throughout the country.

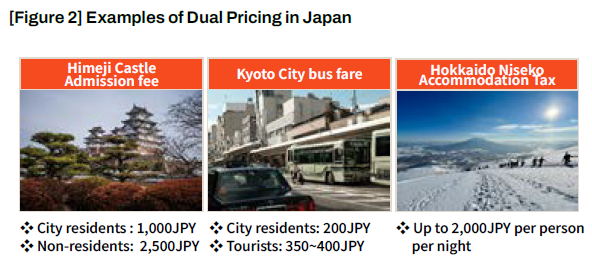

• Differential Pricing at Himeji Castle: Himeji city in Hyogo prefecture has implemented a dual pricing system for entry to the Himeji Castle. While local residents continue to pay the 1,000 JPY (approx. 9,300 KRW), visitors, including foreign tourists, are now charged 2,500 JPY (approx. 23,000 KRW)—2.5 times the standard rate.

• Public Transportation Differentiation in Kyoto: Kyoto is currently pursuing differential fare structures for its city buses. Plans are underway to lower fares for local citizens to 200 JPY, while charging tourists between 350 and 400 JPY.

• Rush to Introduce Accommodation and Tourism Taxes: Niseko, a famous ski resort destination in Hokkaido, has decided to levy an accommodation tax of up to 2,000 JPY (approx. 18,000 KRW) per a tourist per night. Furthermore, Tokyo and Osaka are considering raising existing accommodation taxes or establishing new types of tourism levies specifically targeting foreign tourists.

Such dual pricing systems are common in developing countries with limited infrastructure, such as Egypt (for the Pyramids) or India (for the Taj Mahal), often intended to subsidize welfare for the local population. However, it is highly unusual by global standards for Japan, which markets itself as a leading tourism superpower, to apply higher prices to foreigners for daily public infrastructure, such as national museums or public transportation.

These measures are creating cracks in the brand value of Omotenashi (sincere hospitality), which is the heart and most potent asset of the Japanese tourism industry. Once damaged, this core value is extremely difficult to restore. Complaints and negative narratives are already emerging in global media and among international travelers, suggesting that they are being treated as walking wallets to extract Yen rather than as welcomed guests. While regulating the number of foreign tourists in areas suffering from extreme overtourism is necessary, implementing discriminatory pricing may be a strategic blunder in the long term, as it risks fostering negative sentiment in exchange for short-term tax revenue.

Strategic Positioning for Korea: "High-Quality Tourism Based on Transparent and Equal Value for Money"

With Japan currently erecting barriers by implementing discriminatory pricing for foreigners, now is the optimal moment for South Korea to leap forward as a tourism powerhouse in Asia. To date, Korea has consistently maintained a uniform and transparent pricing structure for both domestic and foreign visitors. We do not charge foreigners triple the fare for the Seoul subway, nor do we inflate entry fees for Gyeongbokgung Palace. Furthermore, backed by the world’s leading ICT environment, fixed-price systems—from app-based taxi payments to kiosk-based restaurant ordering—are fully systematized and transparent. This aligns with Korea’s top-tier global rankings in ICT readiness and Safety and Security, as evaluated by the World Economic Forum’s (WEF) Travel & Tourism Development Index (TTDI).

For global smart consumers who feel slighted by Japan's dual pricing, Korea serves as the premier alternative market. With the depreciation of the Korean Won, absolute prices have become even more affordable, and Korea remains free from price discrimination between domestic and international visitors. We must view Japan’s dual pricing policy as a cautionary tale; we should eradicate the stigma of price gouging in certain local commercial areas through rigorous self-corrective efforts and establish transparent, honest pricing policies as the cornerstone of K-Tourism marketing.

Simultaneously, the principle of "high-quality tourism based on transparent and equal value for money" is not a message intended solely for foreign visitors. Domestic travelers must also experience fair trade—characterized by fixed pricing, predictability, and the absence of excessive price gouging—to restore trust in domestic travel. Ultimately, the competitiveness of Korean tourism does not lie in the separate paths of inbound growth and intrabound revitalization; both can be strengthened together on the foundation of price transparency and market self-purification. Generalizing the isolated instances of price gouging by a few unscrupulous operators and reacting impulsively does not serve the development of Korean tourism.

Conclusion: The Renaissance of K-Tourism, Enhancing Diverse Charms with ‘Price Competitiveness’

Synthesizing the empirical data from this study, the identity of South Korea as a tourism destination is defined by its ability to offer world-class hardware and software experiences at transparent and reasonable costs. While air accessibility was once cited as a limiting factor for price competitiveness, the recent structural depreciation of the Korean Won (mid-to-high 1,400 KRW range per USD) combined with a relatively stable macroeconomic price level (PLI 0.59) has significantly bolstered the price competitiveness of Korean tourism. In this regard, South Korea can be evaluated as a nation possessing a clear competitive advantage in terms of satisfaction per cost in the international tourism market.

Consequently, K-tourism forms a structure that combines unrivaled soft power in the form of Hallyu content, hard power represented by high public safety standards and digital-based transportation and mobility convenience, and price competitiveness backed by recent macroeconomic conditions. The combination of these three elements serves as a core foundation that allows international tourists to experience the charms of Korea with a lower cost burden, acting as a vital catalyst for expanding inbound demand.

This strength becomes even more evident when compared to the recent trajectory of Japan, Asia's largest competitor. While Japan, facing the challenges of overtourism, is expanding discriminatory pricing systems such as dual pricing for foreigners—thereby creating tension regarding the value of hospitality—South Korea maintains a transparent and predictable pricing structure for both domestic and international visitors. This acts as a comparative advantage that highlights the reliability and accessibility of Korean tourism to global travelers who prioritize value-based consumption and fairness.

However, this price competitiveness should not be understood solely as an asset for expanding inbound tourism. Restoring market trust and improving perceptions among domestic travelers are also critical policy tasks that determine the sustainability of Korean tourism. The criticism from domestic travelers that "domestic travel is expensive and prone to price gouging" is an issue that cannot be ignored; intensive self-corrective efforts by the industry and local governments must accompany any aberrant pricing behavior observed in certain commercial areas or during peak seasons. Nevertheless, we must not allow such isolated cases to be generalized into a perception that denies the average price structure and competitiveness of the entire Korean tourism market.

As this study demonstrates, accommodation prices in Seoul and Busan, the tipping-free dining ecosystem, and world-class, ultra-low-cost mobility options are sufficiently competitive even when compared to major global tourist cities and key Asian competitors. Therefore, going forward, we must continuously accumulate and provide data and information that allow for an objective comparison of the real costs of domestic versus overseas travel, inducing domestic travelers to perceive the cost structure of domestic tourism based on facts. Through this, we can mitigate the superficial perception that "domestic travel is an unconditional loss" and promote the restoration and revitalization of a healthy intrabound ecosystem where domestic consumption flows back into local regions.

The tourism industry is a comprehensive industry that extends beyond mere foreign currency acquisition; it is a means of diffusing a nation's charm and likability. The industry and policymakers should no longer remain confined to the exhaustive domestic frame that "Korea is expensive." Instead, they need to simultaneously restore the trust of domestic consumers through market self-purification efforts, while actively promoting the relative price competitiveness of Korean tourism—as evidenced by macroeconomic data and global OTA indicators—to the outside world. When this dual approach—restoring price trust for domestic travelers and strategically leveraging price competitiveness for foreign tourists—is pursued in parallel, Korean tourism will secure a more powerful and sustainable momentum to leap beyond the era of 20 million visitors and become a global mega-tourism powerhouse with over 30 million visitors.