South Korea’s Medical and Wellness Tourism: Strategies for Scalability and Integration

SooCheong Jang / Professor, Purdue University & Director, Yanolja Research / [email protected]

Kyuwan Choi / Professor, Kyung Hee University & Director, H&T Analytics Center / [email protected]

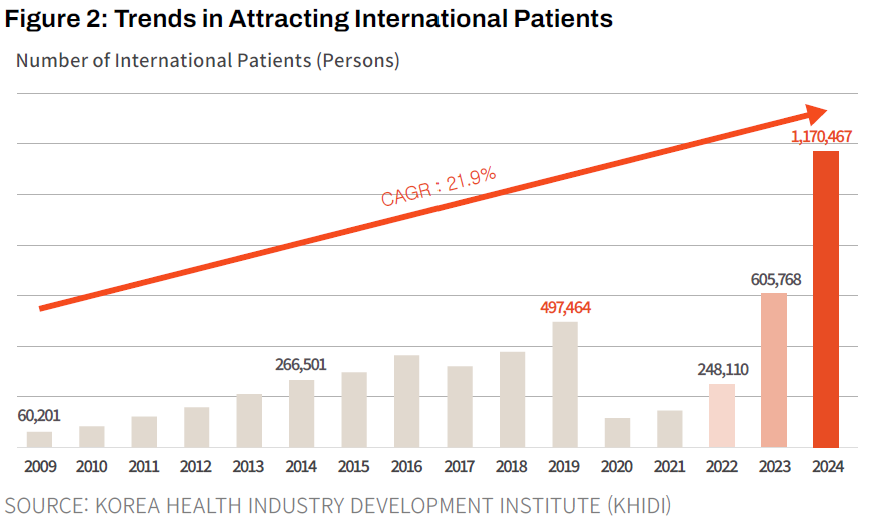

South Korea’s medical tourism industry has emerged from the unprecedented crucible of the COVID-19 pandemic, entering a new era of structural transformation that goes far beyond a mere recovery of demand. In 2024, the number of international patients visiting the country surpassed 1.17 million, generating upwards of $1 billion in medical revenue. This is not only a historic peak since the sector was formally institutionalized in 2009, but a performance that more than doubles the pre-pandemic record of 497,000 set in 2019. Such quantitative expansion serves as a testament that South Korea is no longer a peripheral player valued only for its potential; it has become a central provider capable of absorbing the global appetite for medical and wellness services.

Yet, a closer diagnostic look at this growth through an industrial lens reveals structural fragilities that suggest the ecosystem is far from complete. The primary engine of the 2024 surge was the aesthetic sector—dermatology (56.6%) and plastic surgery—fueled by the global resonance of K-Culture and K-Beauty. Currently, more than 70 percent of all foreign patients are concentrated in these specific fields. Geographically, the imbalance is equally stark: 85.4 percent of patients are clustered in specific Seoul districts like Gangnam and Myeong-dong. This mirrors a precarious architectural feat where the weight of a massive skyscraper rests upon a single pillar. While advantageous for maximizing short-term revenue, this reliance creates a fundamental vulnerability; a shift in K-Beauty trends, sharp currency fluctuations, or a global economic downturn could cause the entire market to buckle.

The landscape of global tourism is evolving rapidly. It is moving past simple leisure or one-off cosmetic procedures toward an organic fusion of "Wellness"—the active pursuit of physical, mental, and environmental health—and "Medical" services requiring professional clinical care. In modern society, the concept of health has expanded beyond the absence of disease to encompass a holistic process of enhancing life satisfaction and overall well-being. Consequently, medical tourism must pivot from a fragmented model focused solely on clinical treatment to a "full-cycle" integrated system. This system should encompass everything from preliminary remote consultations to entry, primary treatment, and post-operative recovery linked with South Korea’s natural resources and specialized infrastructure. Building this "Medical-Wellness Fusion" ecosystem is an indispensable task for securing the nation’s next-generation export engine.

Grounded in these critical observations and macro-level insights, this report proposes a systematic strategy to overcome current limitations and propel South Korea into a top-tier global hub. To this end, we first analyze the macroeconomic mechanisms driving the demand for integrated global tourism and identify core target nations based on empirical data. Furthermore, we dissect the success factors of competitors such as Thailand and Turkey, which have established unique ecosystems by blending medical procedures with resort-style tourism. Ultimately, this study aims to expand the spatial and industrial horizons of South Korean medical tourism—currently confined to specific specialties and the capital region—providing actionable policies and practical strategies to transform it into a diversified, high-value-added industry..

Why Medical and Wellness Tourism: South Korea’s Structural Dilemma

"Poverty Amidst Abundance": Deficits and the Decline in Spending Quality

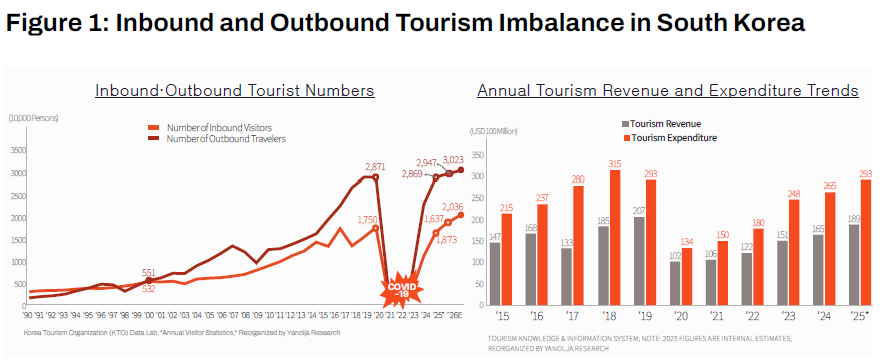

In 2025, South Korea’s tourism sector reached a remarkable milestone, welcoming a record 18.93 million international visitors. Yet, beneath this headline success lies a deepening structural paradox. That same year, the number of outbound Korean travelers reached 29.55 million, far outstripping inbound figures. The result is a persistent tourism deficit that has exceeded $10 billion for three consecutive years—a sign of a chronic imbalance in the nation’s travel economy.

More troubling is the steady erosion of per-capita spending. Despite the surge in the "headcount" of visitors, the average daily expenditure has been on a downward trajectory, slipping from $359.90 in 2022 to $332.90 in 2023, and falling further to $320.60 in 2024. While the seats are filled, the "premiumization of experience"—the ability to convert visits into high-value economic activity—appears to be waning.

A High-Value Solution for a Deficit-Ridden Market

Amidst this structural dilemma, the most potent and pragmatic remedy for South Korea to escape its deficit trap lies in the cultivation of high-value medical and wellness tourism. This sector offers two decisive structural advantages.

First is its extraordinary capacity for spending and its subsequent economic multiplier effect. As of 2024, the average expenditure of a medical tourist stood at approximately 2.26 million KRW, surpassing the 1.87 million KRW spent by general tourists by more than 20 percent. Credit card data reveals that this capital does not remain confined within hospital walls. While the primary purpose of entry is clinical, medical fees account for only 38.3 percent of total spending. The remaining 61.7 percent flows into lodging, shopping, and dining, creating a broad ripple effect across local economies. In practical terms, the economic impact of a single medical tourist is equivalent to that of 6.8 domestic tourists.

Second is the assurance of extended stays and robust return rates. By its nature, medical and wellness tourism—which spans acute treatment, post-operative recovery, and long-term health management—necessitates longer visits than traditional sightseeing. Furthermore, because these services are intimately tied to personal well-being, the trust established during a visit fosters profound customer loyalty. This creates a stable market anchored by continuous follow-up care and reliable repeat visits.

The empirical evidence for this potential is already clear. In 2024, the number of foreign patients in South Korea surpassed 1.17 million, a staggering ascent from the 60,000 recorded when the sector was first institutionalized in 2009. This represents a compound annual growth rate (CAGR) of 21.9 percent. These visitors generated at least 1.4 trillion KRW in direct medical revenue, while their total economic footprint—including the expenditures of accompanying family members—is estimated at approximately 7.5 trillion KRW.

In conclusion, for the South Korean tourism industry to overcome its chronic deficits and pivot from quantitative expansion to a qualitative leap, it must decisively move away from the low-value mass tourism model. The imperative to focus national resources on medical and wellness tourism—as a next-generation engine that guarantees high per-capita spending, longer stays, and enduring loyalty—has never been more urgent.

The Great Convergence: Structural Drivers Behind the Explosion in Global Medical and Wellness Tourism

As established, the imperative for South Korea to cultivate medical and wellness tourism as a high-value sector—characterized by disproportionately high per-capita spending—is a clear solution to the nation’s structural tourism dilemma. But does this sector possess sufficient growth potential on the global stage? The evidence suggests that "Healthcare Tourism" is currently undergoing the most remarkable structural expansion in the modern global travel market.

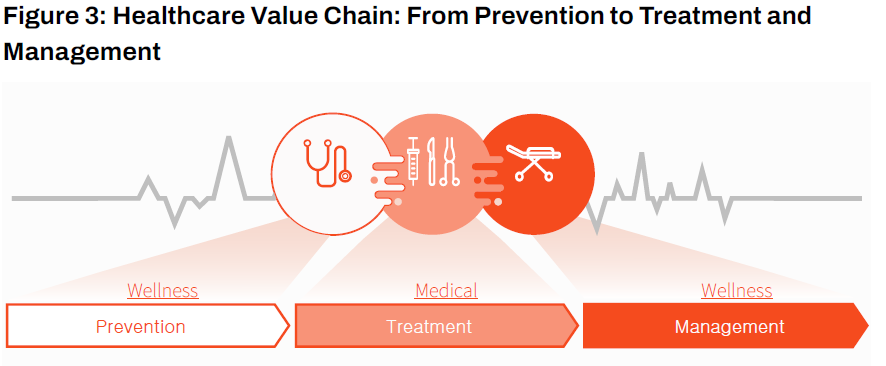

In the past, medical tourism (focused on clinical treatment) and wellness tourism (focused on recuperation and health promotion) were viewed as strictly bifurcated markets. However, the current global megatrend is an organic fusion of these realms into a vast "Healthcare Value Chain": a seamless progression from Prevention (Wellness) to Treatment (Medical) and finally to Recovery and Long-term Management (Wellness). To visualize this ecosystem, one might look to the metaphor of an iceberg. Medical tourism is the visible, urgent peak rising above the water to address immediate clinical needs, while wellness tourism is the massive, submerged body that stabilizes the entire structure and serves as the primary engine for creating inexhaustible value.

The Tip of the Iceberg, Medical Tourism vs. The Submerged Giant, Wellness

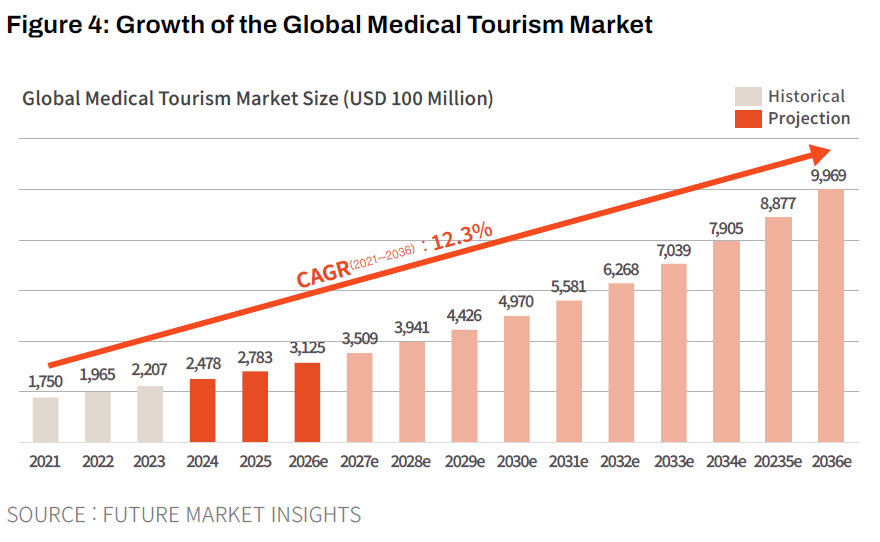

The global medical tourism market, driven by the search for direct clinical intervention, is on a steep upward trajectory. According to Future Market Insights (FMI), this market is projected to grow from approximately $278.3 billion in 2025 to nearly $1 trillion by 2036, sustained by a high annual growth rate of 12.3 percent.

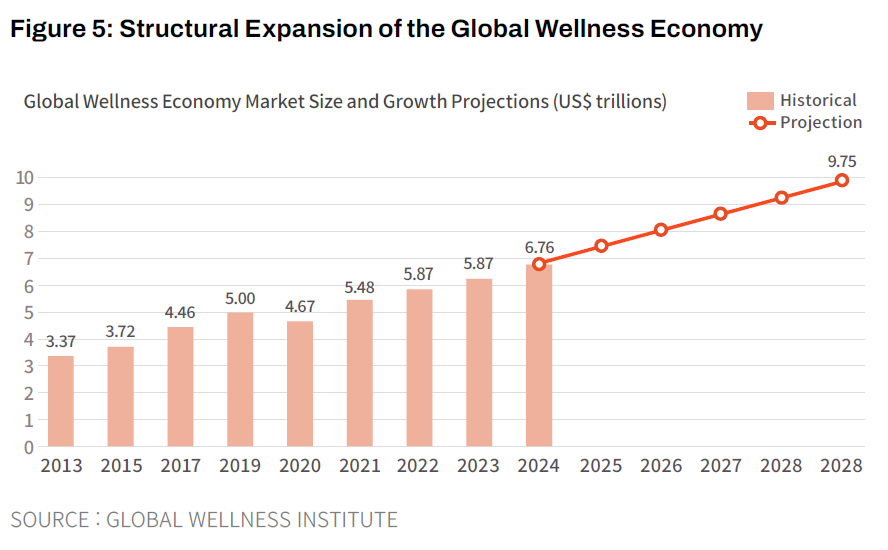

In contrast, while medical tourism is often a mission-driven journey to cure a specific ailment, Wellness is a holistic, daily pursuit of physical, mental, and social health that goes beyond the mere absence of disease. According to the Global Wellness Institute (GWI), the global wellness economy surpassed $6.8 trillion in 2024. This figure dwarfs the global IT industry ($5.3 trillion) and is 2.5 times the size of the sports industry. If the wellness economy were a nation, it would rank as the third-largest economy in the world, trailing only the United States and China, and it is expected to reach $9.75 trillion by 2029.

Completing the Ecosystem: The Organic Fusion

The latest global megatrend involves guiding patients and their families—immediately following successful clinical treatment—into professional recovery programs (Wellness) such as meditation, yoga, tailored diets, and thermal therapies, set within natural landscapes or luxury resort infrastructures. This "Medical-Wellness Fusion" strategy does more than just extend the duration of a visitor's stay; it shifts the economic axis from the confines of the hospital to the broader regional economy, creating an unprecedented multiplier effect. Global capital flows are already pivoting toward this integrated ecosystem, where the technical expertise of medicine meets the long-term sustainability of wellness.

Tectonic Shifts: Why Demand is Exploding

The explosive growth of this market is not a transient phenomenon driven by cheap flights. Rather, it is a structural necessity born from the intersection of failing public health systems in developed nations, the contradictions of high-cost medical models, a lack of infrastructure in emerging economies, and a global demographic shift toward aging. This surge in cross-border healthcare demand is driven by four key structural pillars:

Countries such as Britain, Canada and the Nordic nations, which built tax-funded universal public health care systems long celebrated as emblems of medical equality, are now increasingly seen as nearing a breaking point. As populations age and chronic disease surges, the strain on these systems has become impossible to ignore. In Britain, the National Health Service, or NHS, had more than 7.6 million people on waiting lists for treatment and surgery by mid-2023. That means roughly one in nine Britons was waiting for care. Local media outlets have gone so far as to warn that delayed treatment may be contributing to as many as 120,000 deaths a year.

Canada faces a similar predicament. According to a report by the Fraser Institute, patients there wait an average of 30 weeks — nearly seven months — to see a specialist.

For citizens of these countries, medical tourism is not a luxury holiday. It is often a desperate calculation. While waiting months for a supposedly free operation at home, patients may watch their condition deteriorate, risking death or permanent disability. Job loss, lost income and the heavy costs of family caregiving can turn “free” treatment into an irrecoverable economic loss. Under those circumstances, forfeiting the promise of no-cost care at home and instead flying to countries such as South Korea or Thailand — where surgery can be scheduled and completed within a week or two — may become the more rational, life-preserving choice. For these patients, medical tourism is not indulgence. It is a survival strategy aimed at reclaiming the vanishing golden time for treatment.

In countries defined by expensive, insurance-driven health care systems — above all the United States — staggering medical costs are pushing patients abroad in growing numbers. An analysis by The Commonwealth Fund found that in 2021, health spending in the United States amounted to 17.8 percent of gross domestic product, roughly double the OECD average. Annual per capita health expenditures reached about $12,318, more than three times the level in South Korea. More troubling still is the fact that roughly 60 percent of personal bankruptcies in the United States have been linked to overwhelming medical bills.

Within such a distorted structure, Americans who are uninsured or underinsured and need costly procedures — hip replacements, complex dental implants and other major interventions — often have little choice but to look beyond their borders. In medical tourism hubs such as South Korea, Thailand and parts of Latin America, even after adding first-class airfare, several weeks in a luxury hotel and the fees charged by world-class specialists, the total cost can still amount to only 30 to 50 percent of what a patient might pay for surgery alone in the United States. In the end, medical tourism becomes less a matter of preference than a rational economic alternative.

In parts of the Middle East — including the United Arab Emirates, Saudi Arabia and Qatar — as well as in Central Asia and emerging economies such as Vietnam and Indonesia, private wealth has expanded rapidly. But the development of advanced medical infrastructure and highly specialized clinical talent has not kept pace. In critical areas such as cancer treatment, organ transplantation and cardiovascular or cerebrovascular surgery — fields that require ultra-precise equipment and deep clinical experience — confidence in domestic hospitals often remains weak.

For the wealthy, for royal families and for government-sponsored patients from countries such as Saudi Arabia, crossing a border is not a form of leisure travel in pursuit of better service. It is, quite literally, a journey undertaken to prolong life and avert death. These patients rarely travel alone. They often arrive with extended family members and remain for months in upscale residences or five-star hotels. As a result, the foreign-exchange earnings and local economic spillovers they generate can far exceed those associated with ordinary inbound tourists.

Affluent patients and business elites from Southeast Asia are also drawn abroad for another reason: to avoid aging diagnostic systems and the fear of misdiagnosis at home. In South Korea, a battery of tests and expert interpretations that might take months in some Western countries can often be completed in a matter of days — sometimes even the same day — using cutting-edge equipment and highly experienced physicians. That combination of extraordinary speed and diagnostic precision has become one of the strongest drivers of medical exodus among VIP patients from emerging economies.

Beyond these explicitly medical drivers, the explosive rise of wellness travel for prevention and post-treatment care is broadening the very boundaries of medical tourism. As people become less focused on simply living longer and more concerned with living longer in good health, the wellness industry is undergoing a period of structural expansion. That growth is being propelled by three broad forces.

First, there has been a fundamental shift from treatment to prevention. Because 74 percent of deaths worldwide are now attributable to noncommunicable diseases closely tied to lifestyle — including obesity and cardiovascular disease — the logic of public health is moving away from reactive clinical intervention and toward preventive medicine and everyday health management.

Second, the rise of healthy aging is reshaping demand. As global aging accelerates, consumers are increasingly willing to spend on nutritious food, anti-aging programs and fitness in the hope not merely of extending life, but of extending healthy life expectancy.

Third, mental wellness has become a necessity rather than a luxury. In a world marked by chronic stress and burnout, activities designed to restore mental health — meditation, temple stays, spa therapies and forest healing, among them — are no longer seen as optional indulgences. They are becoming an essential part of modern recovery and care.

South Korea’s Strengths and the Structural Constraints in Medical and Wellness Tourism

South Korea’s medical and wellness tourism ecosystem has achieved remarkable growth, built on world-class infrastructure and formidable cultural appeal. But beneath that success lies a set of structural weaknesses that could stand in the way of long-term, sustainable expansion. Any honest assessment of South Korea’s health care tourism industry must therefore examine both sides of the ledger: the country’s singular competitiveness and the limitations that could erode it over time.

Four Core Strengths of South Korea’s Medical and Wellness Tourism

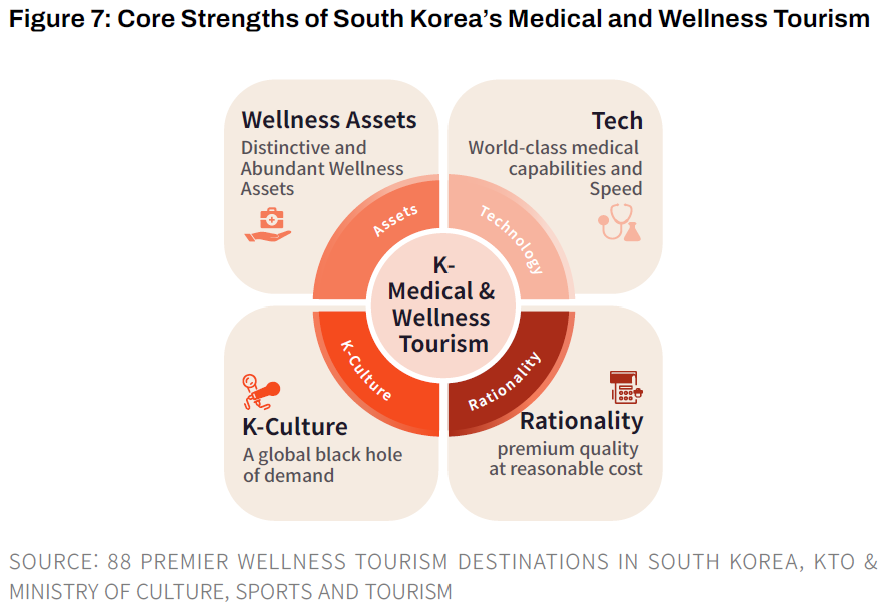

The quality of South Korea’s medical care is not merely anecdotal or reputational; it is borne out by international indicators that consistently place the country among the global leaders. Mortality-to-incidence ratios for major serious illnesses — including stomach, colorectal and breast cancer — rank among the lowest in the world across 185 countries. In highly complex fields of treatment, such as liver transplantation, South Korea has posted clinical outcomes, including five-year survival rates, that surpass those of many advanced Western nations, including the United States. At the same time, the country’s exceptionally high number of CT and MRI units per million people points to a clear edge in diagnostic precision.

Just as important is speed. In many Western countries, seeing a specialist or completing a comprehensive medical examination can take months. In South Korea, the same process can often be completed in a day, or within one to two weeks. For wealthy patients from emerging countries racing against time — or for Western patients worn down by the bottlenecks of public health care systems — that combination of sophistication and urgency has become one of South Korea’s most powerful draws.

From aesthetic procedures to the treatment of serious disease, South Korea offers extraordinary price competitiveness. In the United States, a single Botox treatment can cost more than $400; in Seoul, the same procedure may be available for roughly $30. High-cost surgeries, including knee replacements and coronary bypass operations, can often be performed at just 30 to 50 percent of the price charged in the United States, while still offering top-tier clinical care.

That advantage is not accidental. It reflects a cost structure that competitors would struggle to replicate: a strong domestic pharmaceutical and biotech base, anchored by firms such as Medytox and Hugel, combined with a high-volume, high-efficiency clinical system. Together, they have created an ecosystem capable of delivering both quality and value at a scale few others can match.

The Korean Wave — K-pop, K-dramas and K-beauty above all — has become not only a powerful marketing asset for South Korea’s medical tourism industry, but also one of its most effective gateways. According to the data, 20.2 percent of inbound foreign visitors decided to come to South Korea because of Korean cultural content. The constant global circulation of Korean entertainment through platforms such as Netflix has fueled a broad and growing fascination with Korean beauty, fashion and lifestyle.

That fascination does not remain at the level of passive admiration. It increasingly translates into concrete consumer behavior — appointments at dermatology clinics, plastic surgery consultations, and elective medical procedures. When celebrities such as Kim Kardashian publicly document their interest in Korean skin treatments, the K-culture pipeline becomes more than soft power. It becomes a conversion engine, turning cultural aspiration into medical demand.

South Korea also possesses a wide range of healing resources that set it apart in the global wellness tourism market. Forests cover roughly 63 percent of the country’s land area, creating a natural foundation for forest-healing programs and restorative retreats. Traditional Korean medicine, often regarded as one of the world’s great medical traditions, offers a distinctive therapeutic identity. K-food — especially fermented foods and medicinal cuisine — aligns neatly with the global rise of microbiome-centered wellness trends. And programs such as temple stays, meditation retreats and other forms of contemplative healing speak directly to a world grappling with psychological burnout.

These are not easily imitated assets. They are deeply rooted in Korea’s geography, history and culture. The government, for its part, has sought to cultivate this base more systematically by designating 88 premier wellness tourism destinations across the country.

The Structural Constraints on South Korea’s Medical and Wellness Tourism

Yet for all of these formidable strengths, the industry’s current structure also contains vulnerabilities that could weaken the broader health care tourism ecosystem over time.

The first problem is the extreme concentration of demand in a narrow set of medical specialties. As noted earlier, in 2024 the majority of foreign patients were clustered in just two cosmetic fields: dermatology, which accounted for 56.6 percent, and plastic surgery, which accounted for 11.4 percent. By contrast, the number of patients seeking high-value, high-complexity care — cancer treatment, organ transplantation and other serious interventions — remains comparatively limited.

That imbalance suggests that South Korea’s medical tourism industry has not yet fully moved into the high-end, high-value segment, and remains overly dependent on lower-priced cosmetic procedures. The analogy is instructive: just as Samsung balances mass-market smartphones with high-margin semiconductors, South Korea’s medical tourism portfolio must also find equilibrium between beauty services and advanced fields such as severe disease treatment and regenerative medicine.

The second problem is geographic concentration. An overwhelming 85.4 percent of foreign patients are concentrated in Seoul, especially in a handful of districts such as Gangnam, Seocho and Myeong-dong. That concentration is powerful evidence that the country’s rich regional assets — forests, coastlines, marine wellness resources and local medical services — have yet to be meaningfully integrated into the larger ecosystem.

The third is concentration by nationality. Patients from just three countries — Japan, China and the United States — make up more than 60 percent of the total. That leaves the market structurally vulnerable. A sudden shift in exchange rates, diplomatic relations or geopolitical risk in any one of those countries could send tremors through the entire sector.

Another weakness lies in distribution. South Korea has elite physicians on the supply side and substantial demand on the consumer side, but the connective tissue between them remains thin. There are still too few large-scale health care platforms capable of designing and managing integrated packages that combine flights, lodging, medical care and wellness services. Many of the existing agencies that recruit foreign patients remain small-scale operators, dependent on simple referral-fee models.

As a result, the patient journey often breaks down. Hospitals, understandably, focus on bed turnover and clinical revenue, giving them little incentive to channel post-treatment patients into longer-stay wellness facilities. That disconnect is starkly illustrated by one telling figure: only 5.7 percent of visitors to the government-designated premier wellness tourism destinations are foreign travelers. In practice, that means many patients leave the surgical bed only to head directly for the airport, rather than transitioning into a recovery-oriented wellness setting. The bridge between treatment and recuperation remains weak, and in many cases nonexistent.

In the end, South Korea possesses all the essential components: K-culture as a powerful navigational system, advanced medicine as a high-performance engine, and wellness as a sophisticated source of fuel. What remains underdeveloped is the assembly process that binds them into a coherent whole.

At present, medical tourism is governed largely through a policy framework focused on clinical outcomes and the export of medical services, while wellness tourism is managed through a separate framework centered on extending visitor stays and promoting balanced regional development. With authority and support dispersed across multiple ministries, the ecosystem lacks the institutional cohesion needed to function at full capacity.

What is urgently required is a more flexible and proactive model of interministerial cooperation — one in which agencies share performance indicators, align policy goals and establish the legal and institutional foundations needed to develop integrated medical-wellness tourism products. South Korea has already built the ingredients of a globally competitive industry. The challenge now is to make them work together.

Lessons From the World’s Leading Medical and Wellness Tourism Destinations

The countries that have taken an early lead in global health care tourism are no longer competing on price alone. Instead, they have captured the market by building distinctive ecosystem models that combine their own geographic, cultural and institutional advantages. Their success offers more than a collection of interesting examples; it provides an empirical roadmap for countries like South Korea as they seek to define the future of medical and wellness tourism. By examining how these leading nations have structured their ecosystems, one can draw clearer lessons about the direction South Korea’s health care tourism industry should take.

How the Leading Countries Built Distinctive Ecosystem Models

1. Thailand: A seamless relay from treatment to retreat

Thailand has set its sights on becoming a global luxury medical and wellness hub through a 10-year medical hub master plan spanning 2025 to 2034. At the heart of that strategy is a simple but powerful idea: the patient journey should never be broken. Treatment should flow organically into prevention, recovery and long-term care.

The clearest expression of that model is Bumrungrad International Hospital in Bangkok. The hospital receives patients the moment they enter the country, transporting them by limousine directly from a dedicated lounge at Suvarnabhumi Airport. It has even installed an immigration desk inside the hospital itself, eliminating the burden of separate bureaucratic visits. More notably, it operates a dedicated wellness facility, VitalLife, next to the main hospital building, where post-treatment programs — including anti-aging therapies and genetic analysis — are packaged into an integrated continuum of care. Rather than discharging patients after major surgery and sending them home, the system channels them onward to wellness resorts in Phuket or Hua Hin, where they may remain for weeks to recover. It is a model of near-perfect fusion: treatment in the city, recuperation in leisure destinations, all within one uninterrupted chain.

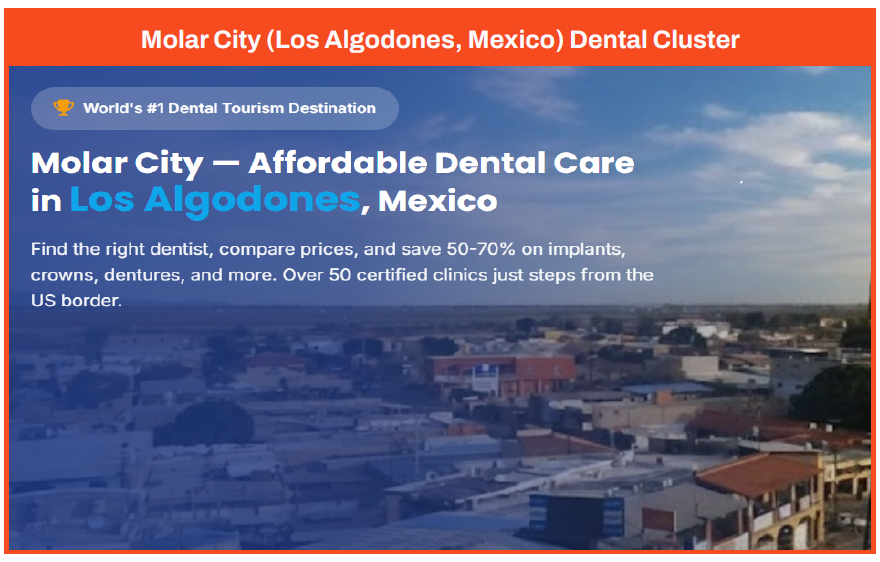

2. Mexico: A giant conveyor belt built on specialization and radical concentration

Mexico has taken full advantage of its geography along the U.S. border to create what amounts to a vertically structured medical factory. In Molar City, a small border town of just 5,000 residents, more than 350 dental clinics and over 600 dentists are concentrated in a single area.

The deeper value of this model lies in its anchor-and-cross-selling strategy. Ultra-low-cost dental care serves as the anchor, drawing patients in at scale. Once they arrive, their waiting time — or the hours spent recovering from anesthesia — is converted into commercial opportunity, circulating them through nearby optometry clinics, pharmacies and other businesses. One highly specialized treatment sector sustains an entire urban commercial web. In effect, a single medical specialty has become the economic engine for a broader ecosystem of consumption.

3. Türkiye: A vast state umbrella designed to reduce uncertainty to zero

Türkiye has pursued a different path, one defined by state-led coordination. By establishing the International Health Services Corporation, known as USHAŞ, under the Ministry of Health, it brought together functions that had previously been scattered across the private sector: marketing, accreditation and dispute resolution. Through a single national-brand portal — HealthTürkiye — the state itself stands behind the quality of services offered.

The strategy is built around eliminating uncertainty at its source. After identifying target treatments such as hair transplantation, the government works with Turkish Airlines to bundle discounted airfare, five-star hotel stays, surgery and interpretation services into one all-inclusive package. It also subsidizes global marketing on an unusually generous scale and has built digital remote aftercare platforms to ease concerns about complications and encourage return visits. The result is a system in which the state does not merely regulate the market; it actively wraps the patient in a sense of security.

4. Malaysia: An independent control tower and a rigorous regime of quality assurance

Malaysia addressed fragmentation by creating an independent institution under the Ministry of Health: the Malaysia Healthcare Travel Council, or MHTC. The council functions like the conductor of an orchestra, coordinating marketing, patient management and quality assurance while bringing 82 member hospitals together under a single national brand, Malaysia Healthcare.

One particularly notable feature of the Malaysian model is its flagship accreditation system. After applying rigorous international standards, including JCI evaluations, the country selected and concentrated support on four leading hospitals. The result was striking: revenue from health care tourism at those hospitals rose by 75 percent. Malaysia has since declared 2026 the “Year of Medical Tourism,” or MYMT 2026, and is now mobilizing national resources in an effort to sharply expand visitor numbers from their current level of roughly 1.6 million. At its core, this is a strategy of brand-building through uncompromising quality assurance.

5. Singapore and Switzerland: The high-end longevity economy, where biotechnology meets luxury

Singapore and Switzerland have chosen not to chase volume. Instead, they have focused on the extreme upper end of the market, seizing an early lead in anti-aging and longevity services.

Singapore has fused advanced biomedical science with elite hospitality. Chi Longevity, the country’s first longevity clinic, is located inside the Four Seasons Hotel and offers highly personalized programs costing millions of won, combining genetic profiling, metabolic analysis and microbiome testing. The country has also elevated wellness into a lifestyle category through R.E. Koop, Asia’s first social wellness club, which opened in the central business district and turned luxury biohacking — hyperbaric oxygen therapy, cryotherapy and similar interventions — into something closer to an everyday consumer good.

Switzerland has built a similarly rarefied ecosystem, but one grounded in the natural prestige of the Alps. There, luxury detox programs that combine stem cell banking, mRNA genetic testing and elite hospitality can cost tens of millions of won for a single week. It is a model designed not for the mass market, but for the world’s ultra-high-net-worth individuals — and it has proven remarkably effective in drawing them in.

What South Korea Can Learn: Five Core Recommendations for Building a Korean Model

The success of these leading countries offers concrete, evidence-based solutions to the very weaknesses that continue to define South Korea’s health care tourism sector: its triple concentration in specialty, geography and nationality, and the fragmentation of its value chain. Five lessons, in particular, stand out.

Lesson 1: Design long-stay integrated packages that extend beyond one-time procedures

South Korea must overcome the broken patient journey in which treatment ends and the traveler heads straight for the airport. The Thai model offers a clear alternative. As Bumrungrad has shown, medical treatment in urban centers can be linked to longer recovery stays in regional wellness destinations. South Korea should move aggressively to develop hybrid products — perhaps under a concept such as the “Medi-tel” — that connect medical procedures in Seoul or other cities with restorative stays in places such as Gyeonggi, Jeju or Gangwon.

Lesson 2: Use K-beauty as the anchor for high-value cross-selling

Rather than viewing the concentration in dermatology and plastic surgery as a weakness to suppress, South Korea should treat it as a powerful point of entry — much as Molar City has done with dental care. Patients who arrive for aesthetic procedures should be guided naturally into higher-margin wellness offerings, including premium health screenings, traditional Korean detox programs and other high-value K-wellness products. What is needed is not less beauty tourism, but a more sophisticated cross-selling ecosystem built around it.

Lesson 3: Create an independent control tower and a national quality certification system

South Korea must move beyond the current fragmented competition among individual hospitals and create the conditions for genuine national branding. Malaysia’s MHTC offers a strong model. A Korean equivalent could gather scattered institutions under a unified national brand while introducing a rigorous flagship certification system that guarantees quality at the national level. For foreign patients, trust is often the single most decisive variable. A credible state-backed quality framework could become one of South Korea’s most powerful assets.

Lesson 4: Build a state-led integrated platform that removes uncertainty from the patient journey

Türkiye’s model suggests the importance of a one-stop platform capable of handling flights, lodging, treatment and interpretation with a single click. South Korea should seriously consider a similar state-led platform, backed by close cooperation among ministries. Such a system would not only reduce uncertainty at every stage of the patient experience, but also allow post-return digital aftercare to be integrated into the process. In that model, South Korea would not simply provide treatment for a single episode of illness. It would position itself as a lifelong health care partner.

Lesson 5: Seize the ultra-high-value market through advanced regenerative medicine

Finally, South Korea should use its recently implemented Advanced Regenerative Bio Act as a lever to enter the global luxury longevity market. Singapore and Switzerland have shown what becomes possible when biotechnology, elite hospitality and distinctive natural assets are woven into one offering. South Korea could develop its own anti-aging programs by combining advanced regenerative medicine — including stem cell and gene-based therapies — with high-end accommodations and the country’s own natural and cultural resources. That would create a path toward attracting the world’s wealthiest patients, rather than competing solely for volume.

A Paradigm Shift in South Korea’s Medical and Wellness Tourism: Proposing “K-MediWell”

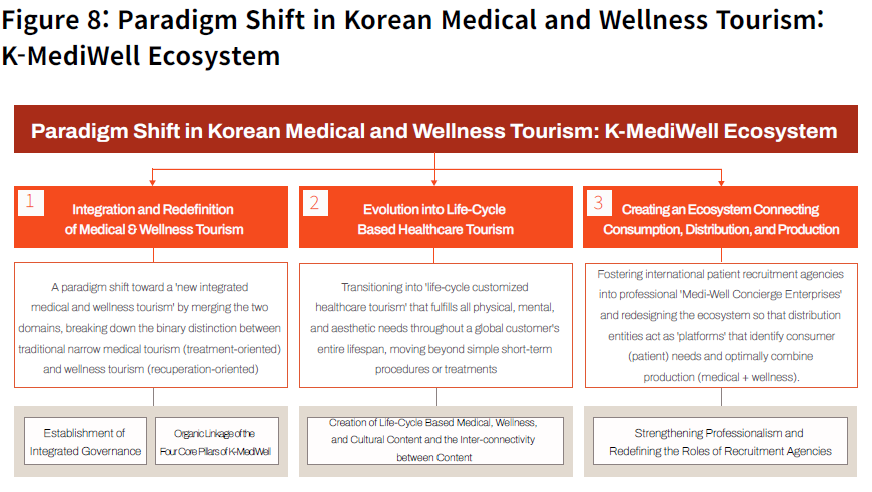

To overcome the structural limitations confronting South Korea’s health care tourism industry — namely, the concentration of patients in a narrow set of medical specialties and geographic areas, along with the fragmentation of the customer journey — and to secure a lasting global competitive advantage, a fundamental paradigm shift is required. The industry in its current form is marked by disconnected links between production (medical institutions), distribution (patient recruitment agencies), and consumption (foreign patients). Medical care and wellness services continue to operate in parallel rather than in concert, preventing the country from fully realizing the continuous value chain that now defines global best practice in health care tourism: prevention, treatment and management.

Against this backdrop, the authors propose abandoning the outdated binary of “medical tourism versus wellness tourism” and replacing it with a new hyper-converged ecosystem model: K-MediWell. This framework integrates prevention, treatment and post-treatment management into a single continuum. It is more than an expansion of existing products. It is a national strategic framework aimed at redesigning industrial structure, distribution systems, customer relationships and policy governance in their entirety.

1. Defining K-MediWell: A Smartphone-Style Revolution in Health Care Tourism

K-MediWell is a model that integrates what have traditionally been separate domains — medical tourism and wellness tourism — into a single, continuous value chain. It is designed to deliver a full-cycle health care experience in which prevention (wellness), treatment (medical care), and recovery and management (wellness) are connected within one seamless system. In that respect, it reflects the underlying structural direction in which global health care tourism is already moving, while also representing a strategic attempt to reorganize South Korea’s own strengths — advanced medical technology, K-culture and natural healing resources — into one integrated platform.

The concept may be likened to the smartphone revolution. Just as the fusion of the camera and the telephone transformed everyday life, K-MediWell seeks to combine K-culture as the channel of attraction, world-class medical technology as the engine of treatment, natural healing assets as the foundation of recovery, and digital platforms as the connective tissue into one seamless experience. It is, in essence, an innovation platform that transforms a fragmented customer journey into a continuous structure of value creation.

2. Interindustry Collaboration and Institutional Foundations: Redesigning the Infrastructure for a Hyper-Converged Ecosystem

For the K-MediWell model to function in practice, the industrial boundary between health care and tourism must be dismantled, and a policy environment capable of supporting such integration must be established. That, in turn, requires close coordination among government ministries and meaningful institutional innovation.

A more flexible regulatory framework should be introduced to reflect global market realities, including broad regulatory sandboxes covering areas such as medical advertising, telemedicine and systems for managing foreign patients. At the same time, integrated infrastructure — including hybrid facilities such as the “Medi-tel,” which combines medical care and recovery-oriented hospitality — should be expanded, and strategic alliances across industries should be actively encouraged.

3. Product Strategy: Expanding a Nationwide Ecosystem Through an Anchor-Cross-Selling Structure

The current structure, heavily concentrated in Seoul’s Gangnam district and in aesthetic medicine, offers strong short-term profitability but reveals clear limits in long-term sustainability. To overcome those limits, South Korea must use K-beauty, which accounts for roughly 70 percent of total demand, as a powerful anchor for market entry and then connect that demand to premium wellness offerings through a more systematic cross-selling ecosystem.

Packages could be designed so that patients who undergo cosmetic procedures in Seoul are then naturally linked to forest-and-lake healing programs in Chuncheon or marine wellness experiences in Jeju. Such packages would lengthen visitor stays, increase total spending and create a pathway for dispersing consumption away from the Seoul metropolitan area and toward the regions. In doing so, K-MediWell could also become a strategic bridge to more balanced national development.

4. Relationship Strategy: Managing the Customer Life Cycle Through Lifelong Health Care Partnerships

The ultimate ambition of K-MediWell is to move beyond one-time transactions and transform foreign patients into lifetime customers. In other words, the industry must evolve from a model centered on episodic visits to one based on enduring relationships.

That requires designing tailored journeys across the life cycle: aesthetic enhancement in youth through K-beauty; functional recovery and preventive screening in middle age; and longevity management through regenerative medicine in later life. By combining these stages with digitally enabled remote aftercare, South Korea can build durable partnerships that continue long after the patient has returned home.

5. Distribution Innovation: From Small-Scale Agencies to a K-MediWell Health Care Concierge

One of the weakest links in South Korea’s medical tourism industry today lies in distribution — the structure that connects producers and consumers. Most foreign-patient recruitment agencies remain small-scale operators whose functions are largely limited to interpretation, airport pickup and appointment booking. As a result, the patient experience effectively ends with hospital treatment, producing a fragmented system in which the broader value chain is never fully activated.

This is a decisive bottleneck. The strategic imperative, therefore, is to elevate distribution beyond simple brokerage and transform it into a form of experience orchestration. South Korea should cultivate globally competitive K-MediWell Health Care Concierge platforms capable of integrating flights, lodging, medical care and wellness into a unified service system. From airport arrival to post-treatment management, these platforms should provide end-to-end coordination, enabling medical tourism to evolve from a narrow service transaction into a total health care experience industry.

In conclusion, K-MediWell is not merely a new tourism product. It is a national strategic model aimed at fundamentally reorganizing the structure of South Korea’s tourism industry. By integrating medicine, tourism, culture and digital technology into a single platform, it offers one of the most powerful solutions available for achieving both a qualitative leap in inbound tourism and a meaningful improvement in the tourism balance.

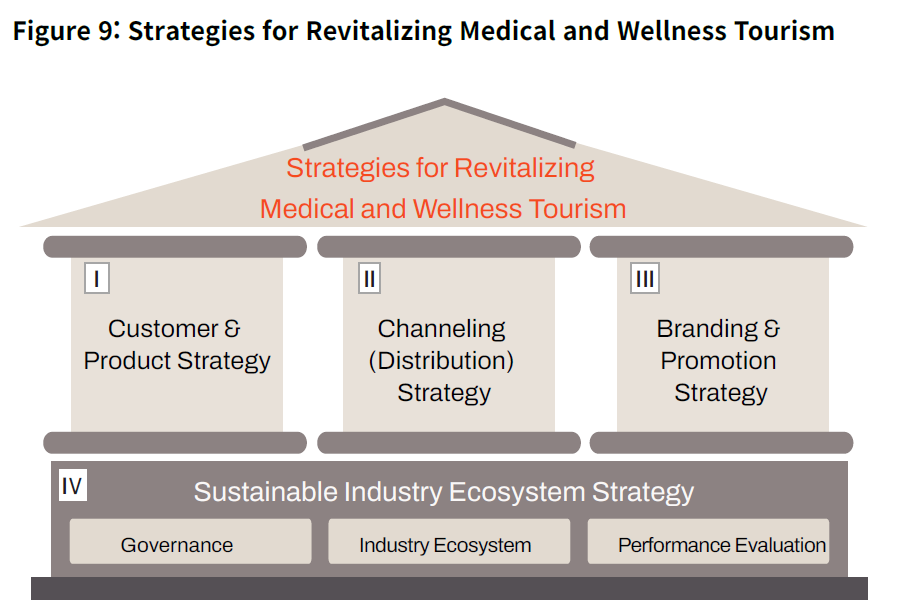

Strategies for Revitalizing South Korea’s Medical and Wellness Tourism Industry

As discussed earlier, the three industries of medical care, wellness and tourism are increasingly shedding their traditional boundaries and generating new forms of convergent value. The intersection of clinical treatment, preventive health management and the pursuit of new experiences is precisely where medical and wellness tourism now takes shape. The ideal development of such a convergent industry lies not merely in the quantitative expansion of its individual sectors, but in the explosive growth of the hyper-converged space where all three overlap. In essence, the task is to create demand by delivering the content of medicine and wellness through the carrier of tourism.

Despite its considerable potential, South Korea’s high-value medical and wellness tourism industry continues to face several structural constraints, as diagnosed earlier. Yet paradoxically, those very limitations contain the seeds of a qualitative leap. To convert potential into reality, the country must systematically design and implement four core activation strategies: customer and product strategy; channeling and distribution strategy; branding and promotion strategy; and the building of a sustainable ecosystem. What follows, then, is a more concrete proposal for the four strategic pillars that could drive a fundamental paradigm shift and a full-scale revitalization of South Korea’s medical and wellness tourism sector.

I. Customer and Product Strategy: Precision Targeting and the Selection, Concentration and Linkage of Products

A customer-and-product strategy begins by identifying the target customer for medical and wellness tourism, constructing an effective portfolio of tourism products, and expanding cross-selling by linking different product categories.

1. Defining the target customer: multilayered, data-driven targeting

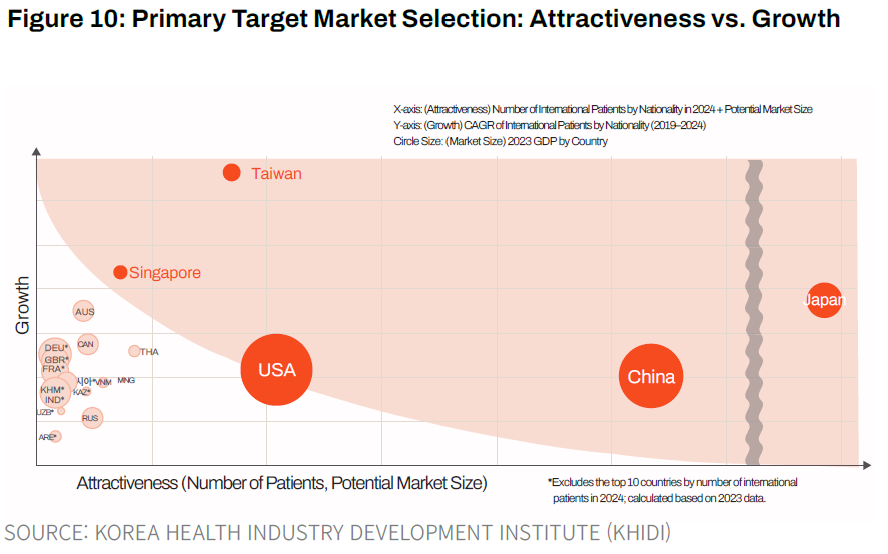

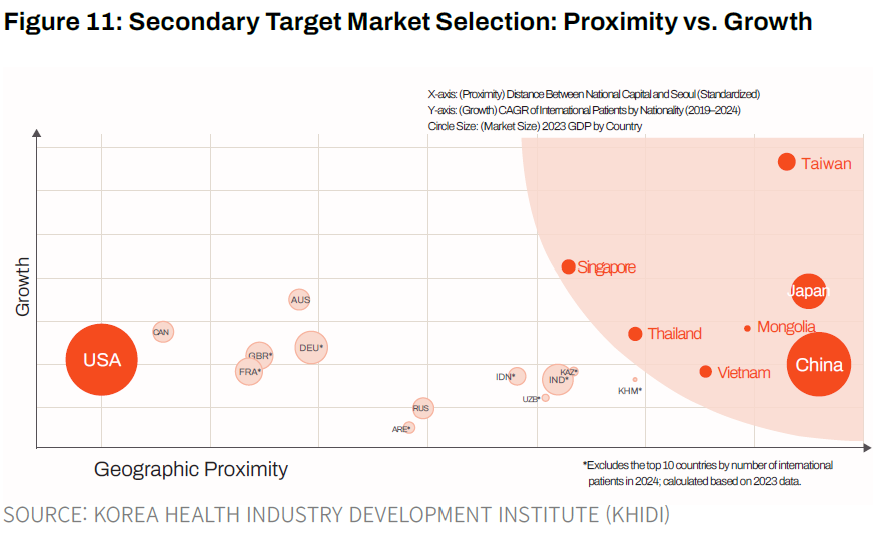

Any effective strategy begins with a precise answer to three questions: To whom should it be sold, what should be sold, and how should it be sold? On the basis of current patient volumes, market attractiveness, recent growth trends and geographic proximity to Korea, target markets can be divided into primary core targets and secondary emerging targets.

The primary target group consists of Japan, China, the United States, Taiwan and Singapore. Japan is the largest market, with about 440,000 patients in 2024, and has recorded explosive growth, with a compound annual growth rate of 45.2 percent. Yet its per-capita spending remains relatively low, and visits are often short and concentrated in dermatology. China shows clear demand for aesthetic medicine, while per-capita spending, at roughly 4.43 million won, is more than twice that of Japan. The United States has the highest per-capita spending, at about 5.85 million won, and a higher share of serious treatment and health screening, making it especially favorable for attracting high-value patients. Taiwan has posted the fastest growth, with a CAGR of 104.2 percent, while Singapore stands out for its high-spending profile.

The secondary target group includes Thailand, Vietnam, Mongolia and the CIS countries. Mongolia is particularly striking. Although patient numbers remain modest, the country sends a disproportionate number of patients seeking highly complex treatment, giving it the highest per-capita spending of all, at roughly 9.97 million won. Vietnam, too, stands out as a promising strategic partner for qualitative upgrading, with diverse treatment demand and strong consumer spending — in effect, a high-spending VIP market in the making.

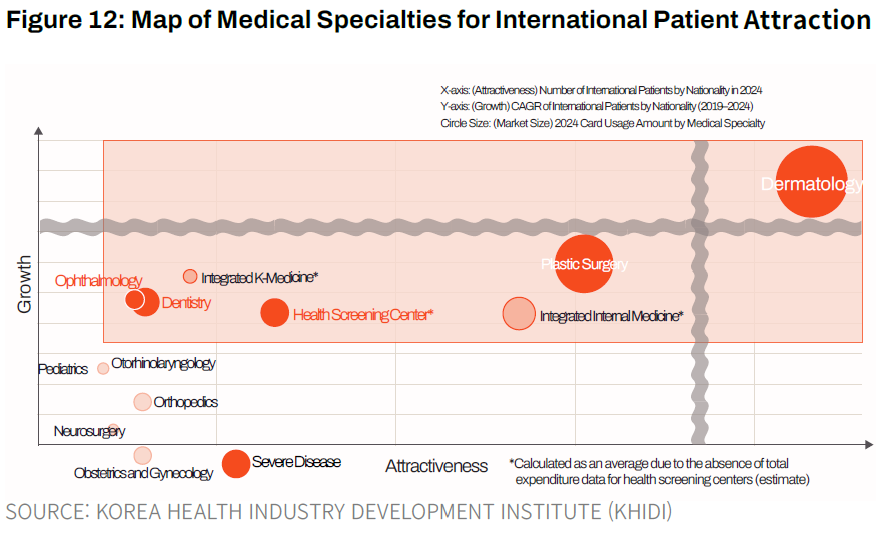

2. Selection and concentration in medical products: five priority fields and the cultivation of severe care

When one considers, by specialty, the growth rate, patient volume and market size associated with foreign patients visiting South Korea, the medical product categories that merit strategic concentration become increasingly clear.

Dermatology recorded 705,044 foreign patients in 2024 and a CAGR of 52.6 percent, making it the fastest-growing and largest specialty in the sector. Per-capita spending, at about 1.04 million won, is relatively low, but Korea’s cost competitiveness — particularly in Botox, supported by strong domestic manufacturers — remains formidable. Korea also enjoys a distinctive operational advantage that is difficult to replicate abroad: highly specialized division-of-labor systems extending from coordinator consultations to post-procedure care, and clinics capable of operating dozens of devices simultaneously.

Plastic surgery, with 141,845 patients in 2024 and a CAGR of 9.4 percent, forms the second major pillar of the aesthetic medical market. Its core strength lies in an unparalleled depth of clinical experience and a globally influential beauty standard reinforced by K-content. Particularly important is the concentration of clinics in Gangnam, Seocho and Myeong-dong, where one of the world’s most distinctive medical clusters has emerged, expanding patient choice while reinforcing a virtuous cycle of competition and innovation.

Health screening centers, ophthalmology and dentistry have seen more moderate growth — with CAGRs of 0.6 percent, 3.9 percent and 3.5 percent, respectively — but because their patient base is more diversified across nationalities, including the United States, Mongolia and Vietnam, they deserve strategic support as a hedge against concentration risk. Korea’s stock of CT and MRI units per million people — 45.3 and 38.7, respectively — far exceeds the OECD average. That advanced diagnostic infrastructure, combined with the ability to complete multiple pre-surgical tests within a single day, remains a core pillar of the country’s global competitiveness.

By contrast, the number of foreign patients in the field of severe disease fell to 29,039 in 2024, down 5.7 percent from 2019. But this should not be mistaken for a collapse in demand. Overseas demand for highly complex treatment continues to rise in both advanced and emerging economies, and South Korea, despite its world-class capabilities, has not yet absorbed that demand fully. One reason is structural: conventional medical tourism is largely B2C, while attracting severe-care patients often requires B2G or B2B arrangements involving governments and insurers.

This is particularly evident in Seoul, where leading tertiary hospitals face a structural limit on further foreign-patient intake due to strong domestic demand, foreign-bed caps and chronic workload pressures. At the same time, top-tier regional hospitals possess excellent medical capacity but remain underweighted in high-value treatment. To address that inefficiency, South Korea should strategically cultivate tertiary and large general hospitals outside the capital region — in places such as Busan, Daegu and North Gyeongsang Province — as hubs for severe care, while more aggressively expanding patient referral agreements through B2B and B2G channels.

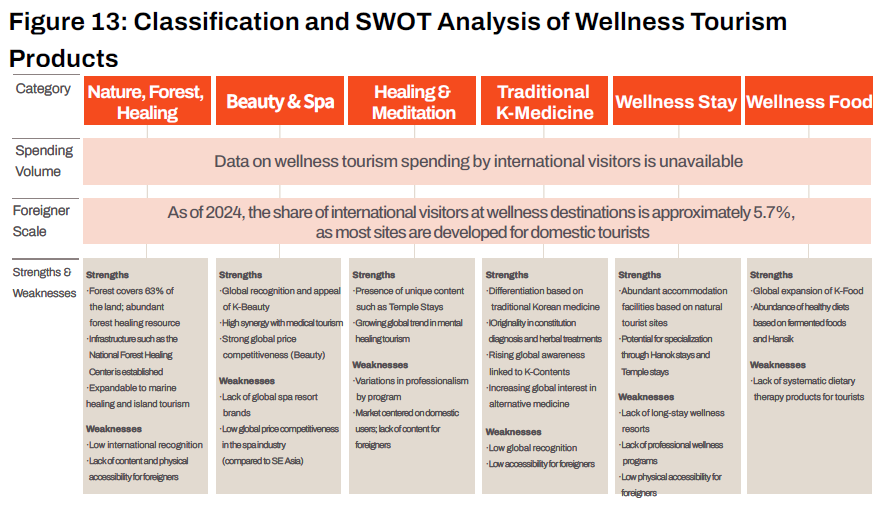

3. Selection and concentration in wellness products: convergence toward a premium strategy

South Korea’s wellness tourism offering spans six broad categories: nature and forest healing, beauty and spa, healing and meditation, traditional Korean medicine, wellness stays and wellness food. Yet foreigners account for only 5.7 percent of visitors to the country’s designated premier wellness destinations, or roughly 418,325 people. In other words, most Korean wellness content remains designed for domestic consumption. That gap suggests that wellness infrastructure built around local demand continues to present access barriers to foreigners and has yet to communicate its differentiated experiential value clearly enough.

Among the six categories, the area with the clearest global competitiveness at present is beauty and spa. Through K-pop and K-drama, Korean approaches to makeup, hair and skincare have spread internationally as a cultural standard. That has created not only demand for Korean beauty products, but demand for direct participation in Korean beauty experiences. Distinctive offerings such as personal color analysis, priced at about 100,000 to 150,000 won per hour, and K-makeup classes, at roughly 80,000 to 200,000 won per hour, represent successful examples of experiential commodification — products that users eagerly share on social media, generating organic promotion. Large-scale beauty wellness franchises such as Welkin Scalp Care Center, Cha Hong Room and Juno Hair were built primarily around domestic demand, yet already show high levels of linked consumption among foreign medical tourists.

Taken together — the industrial structure, consumer characteristics, supply profile and distribution conditions — the strategic direction of Korean wellness tourism points toward a premium and luxury focus. Basic spa or massage services are areas where Thailand and Bali already dominate both in price and in experience, leaving Korea with limited comparative advantage. By contrast, foreign demand is increasingly shifting toward high-end, uniquely Korean wellness experiences that can only be had in Korea. The current supply structure, centered on large and upscale wellness facilities with interpretation and reservation systems already in place, is also better suited to premium services than to the mass market.

4. Linking medical and wellness products: anchoring, cross-selling and customized integration

The data make it clear that foreign patients visiting Korea for medical services already spend substantial amounts on wellness-adjacent consumption. In 2024 alone, foreign dermatology patients spent a total of 1.1684 trillion won outside the medical sector. Their major spending categories included department stores, duty-free shops, restaurants, cosmetics and hair salons. Yet structurally, very few services currently bundle medical care and wellness into a unified package.

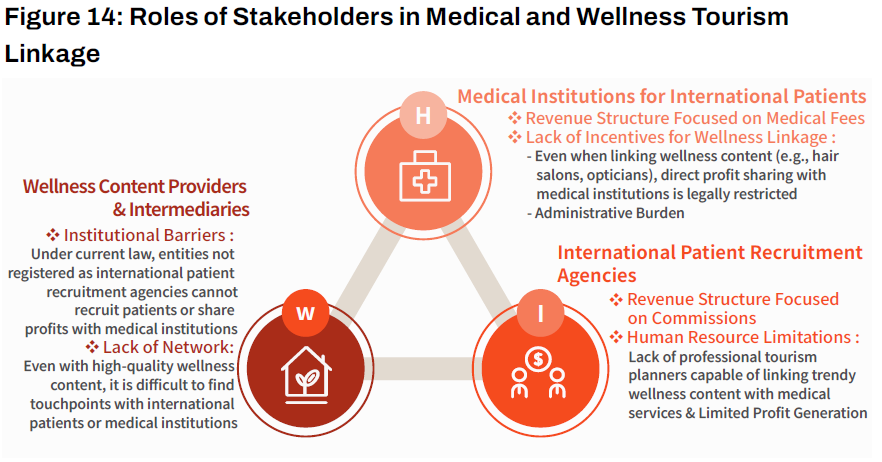

The reasons lie in the structural limitations of three different sets of actors. First, from the perspective of medical institutions, even when wellness content is linked to treatment, the direct revenue-sharing benefit to the hospital is limited, leaving little incentive to develop such packages. Second, wellness content providers and intermediaries face institutional barriers: unless they are legally registered as foreign-patient recruitment businesses, they cannot formally attract patients or share profits with medical institutions. Third, existing patient recruitment agencies tend to remain passive about wellness integration because wellness products are generally low-priced and therefore offer limited additional profit under the current model.

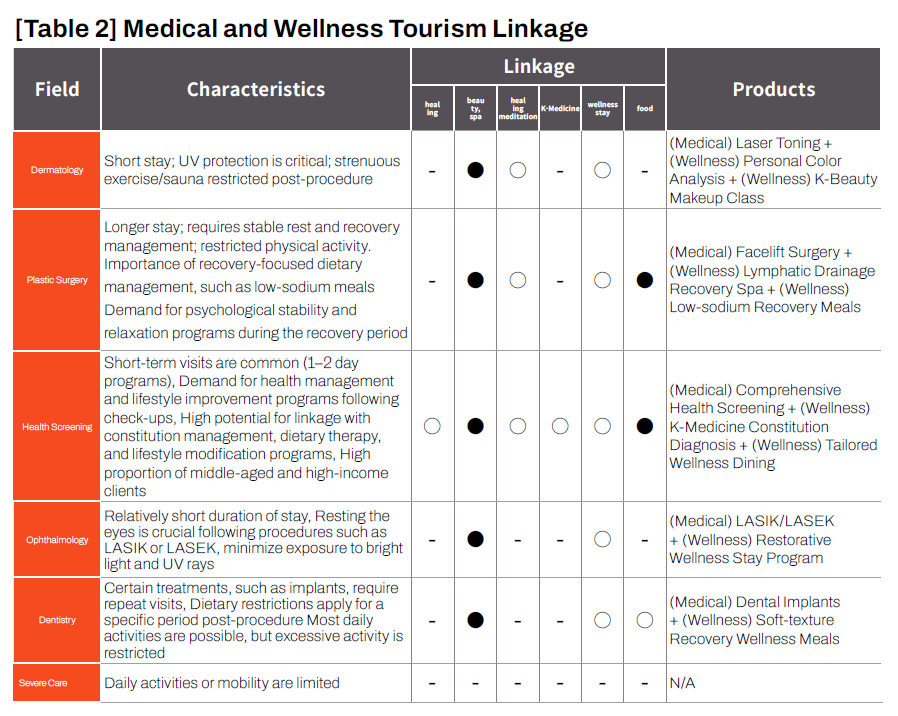

The key strategy for overcoming this structural disconnect lies in an anchor strategy and cross-selling. Patients visiting dermatology and plastic surgery clinics — who account for 68 percent of total demand — should be treated as the gateway through which consumption is redirected into other medical and wellness categories. Tailored linkage programs can then be designed according to the specific treatment characteristics of each specialty.

For dermatology, where post-procedure care often requires UV avoidance and minimal skin irritation, the most suitable linkages are in the beauty-and-spa category, such as personal color analysis and K-beauty makeup classes. In plastic surgery, where rest, recovery and emotional stability are essential after treatment, suitable pairings include lymphatic recovery spa programs, meditation or psychological stabilization programs, and low-sodium recovery meals. Visitors to health screening centers — especially affluent middle-aged and older clients — often show strong post-screening demand for body constitution management and lifestyle improvement, making them especially well suited to programs in traditional Korean medicine, customized wellness dining and restorative wellness stays.

South Korea has already seen early examples of this model. Life Center Chaum integrates clinics, spas and hair services within a single building, while platforms such as Creatrip have begun commercializing bundled packages linking dermatology, dentistry and beauty services. Abroad, Thailand’s recovery programs based on traditional Thai medicine, Sunway City’s hospital-resort-spa complex in Malaysia, and Türkiye’s thermal rehabilitation tourism based on natural hot springs all offer valuable benchmarks for K-MediWell-style linked products.

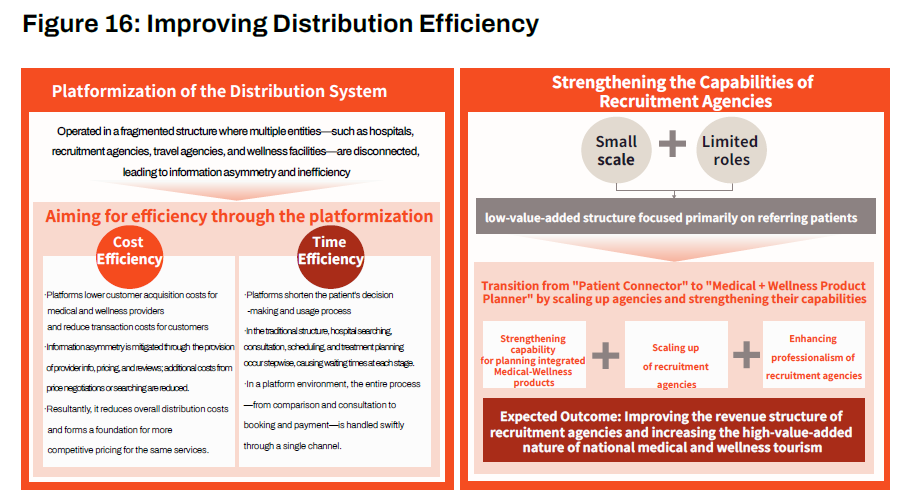

II. Channeling and Distribution Strategy: From a Fragmented Ecosystem to an Integrated Platform

For medical and wellness tourism to grow, the most important task is to connect suppliers with consumers. In other words, building an efficient distribution structure is essential. The platform economy and generative AI should therefore be treated as central tools in improving distribution efficiency.

1. The current distribution structure

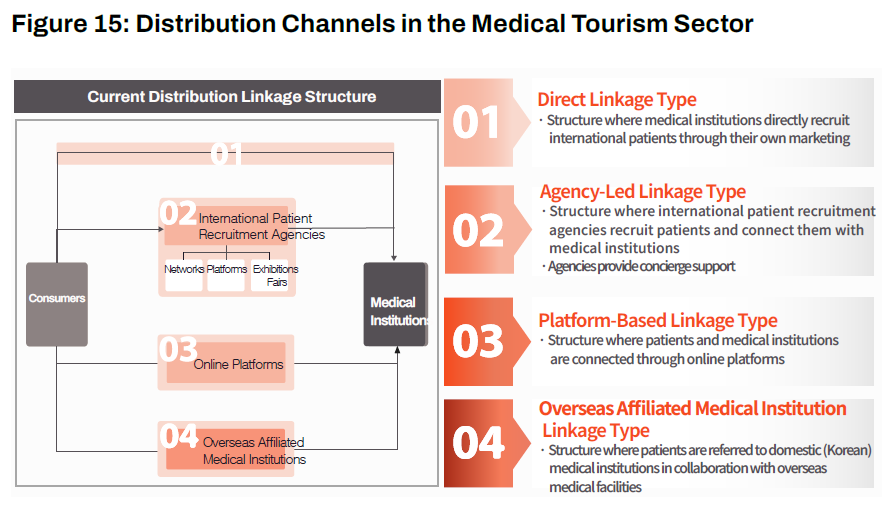

The distribution structure of medical and wellness tourism can be broadly divided into four forms, depending on how consumers are connected to medical institutions or wellness-content suppliers: direct connection, connection through registered foreign-patient recruitment agencies, connection through online platforms, and linkage through overseas partner medical institutions.

The first, the direct-connection model, involves hospitals attracting foreign patients on their own through social media platforms such as Instagram, YouTube and TikTok, global search-engine optimization and advertising, or overseas roadshows. The model has the advantage of eliminating intermediary commissions, which lowers variable costs and may reduce costs for patients. But because it requires substantial initial investment in global marketing, multilingual consultation and foreign-patient response infrastructure, it tends to favor large hospitals. More important, because the structure remains hospital-centered, it rarely leads to the design of integrated medical and wellness packages.

The second, the recruitment-agency model, relies on licensed agencies that gather overseas patients through local networks, proprietary platforms or expos and then connect them to medical institutions. In South Korea, only legally registered recruitment businesses may perform this role. Overseas, however, patient recruitment occurs through a much wider range of channels, including travel agencies, insurers and even sales networks in sectors such as cosmetics and automobiles. Korean medical institutions typically pay recruitment commissions to these agencies — capped by law at 15 percent for tertiary hospitals, 20 percent for general hospitals and 30 percent for clinics — and have often covered these costs through dual pricing for foreign patients. Recently, however, the growing transparency of online pricing has led to stronger resistance among foreign patients to dual pricing, prompting a shift toward models in which agencies charge concierge fees directly to the patient. Even so, most agencies remain small and continue to face limits in staffing and operating capacity.

The third is the platform-based model, which includes specialized medical tourism platforms such as Gangnam Unni, Medical Travel Korea and GroovyX; global online travel agencies; and public platforms. Specialized medical tourism platforms integrate multiple functions, including hospital promotion, price information, discount coupons, online consultation between hospitals and patients, reservations and reviews. Korea’s public platform, Medical Korea, remains largely limited to basic hospital promotion and information provision. In functional terms, it falls well short of Türkiye’s HealthTürkiye platform, which offers one-stop services including treatment plans, quote requests, price comparisons, online booking, airfare and accommodation integration, complaint filing and redress. In Türkiye, USHAŞ centrally manages the platform and supports the full process through 24-hour multilingual call centers, follow-up satisfaction surveys, complaint intake and formal remedy procedures.

The fourth model is linkage through overseas partner institutions. This includes government-to-government patient referral agreements with countries such as the United Arab Emirates, Saudi Arabia, Kuwait, Mongolia and parts of Central Asia; remote consultation agreements between hospitals; and referral structures based on the transfer of Korean clinical expertise abroad. This channel is particularly valuable because it tends to bring in highly complex patients, but it is also difficult to scale because building such networks is inherently demanding.

Taken together, the current distribution system suggests a clear trend: alongside the digital transformation of traditional offline intermediaries, platform-based connection is expanding rapidly. In particular, systems in which patients directly obtain information, verify services and make reservations through online platforms are likely to become far more prominent in the years ahead..

2. How to improve distribution efficiency

The essential weakness of the current distribution system lies in the information asymmetry and transaction inefficiency that arise from a fragmented structure in which hospitals, recruitment agencies, travel companies and wellness facilities are only loosely connected. Two broad directions are available to address that problem.

The first is platformization. An integrated platform that bundles flights, accommodation, medical treatment and wellness stays into a single planning and sales channel would dramatically improve efficiency on two dimensions: cost and time. On the cost side, the aggregation of supplier information, pricing and reviews on a single platform would reduce information asymmetry and lower search and negotiation costs. On the time side, the waiting periods embedded in every step of the conventional process — hospital search, consultation, schedule coordination and treatment planning — would be reduced or eliminated, allowing comparison, consultation, booking and payment to occur rapidly through a single channel. AI-driven hyper-personalization already seen in global travel tech points to a useful model. What is needed is a smart platform through which a patient can enter symptoms in their own language, receive AI-matched recommendations for the most appropriate hospital and regional wellness itinerary, and complete integrated bookings. Trust would become even stronger if such a platform were paired with a post-discharge telemedicine system that allows patients to remain connected to their Korean physician from abroad through wearable devices.

The second direction is the strengthening and scaling-up of foreign-patient recruitment agencies. Agencies that remain trapped in low-value referral-fee models must be transformed from mere patient connectors into planners of integrated medical and wellness products. That requires greater scale, stronger professionalism and institutional and financial support that would allow these firms to grow into K-MediWell concierge companies on the model of global online travel agencies.

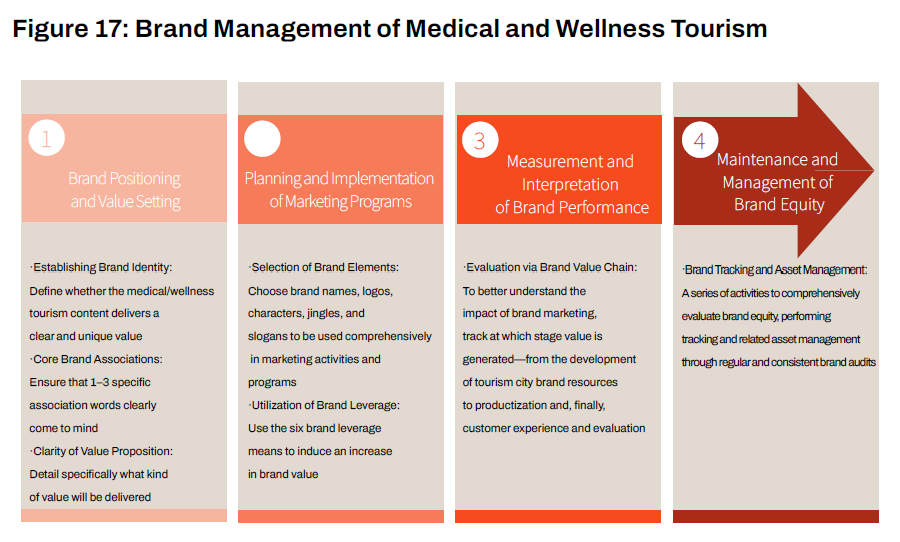

III. Branding and Promotion Strategy: Building K-MediWell as a National Brand

From the standpoint of modern management, every product and service in the world is branded. Nations and health care are no exception. Yet South Korea’s medical and wellness tourism industry still appears to be at the earliest stage of brand recognition. If the sector is to be branded in a way that reflects the country’s global standing, a deliberate and strategic approach from the outset is essential.

1. Why a national brand strategy is needed — and where it should go

One of the most serious structural flaws in Korea’s medical and wellness tourism sector is the absence of a coherent national brand. Because each actor has focused on selling individual medical or wellness products, the image most readily associated with Korea in this field remains narrowly confined to dermatology and plastic surgery. Despite the country’s abundance of content, there is no integrated message or visual identity that cuts across these assets, leading to the inefficient fragmentation of policy resources and budgets.

The most plausible solution is to establish K-MediWell as a national integrated service brand. This can be understood as an effort to extend the logic of K-content — exemplified by K-drama and K-pop — into the realm of medical and wellness tourism. Successful branding depends above all on coherence: a clear brand identity, strong core associations and a persuasive value proposition. Put differently, Korea must provide a compelling answer to the question, Why should one go to Korea? And it must communicate, in the language of the traveler rather than the provider, the particular experiences, emotions and benefits that cannot be replicated elsewhere.

From the standpoint of brand theory, the branding process in medical and wellness tourism should be managed as a continuous sequence: (1) positioning the brand and defining its value; (2) planning and executing marketing programs; (3) measuring and evaluating brand performance; and (4) maintaining and managing brand equity over time. All of this must be tied to sustainable key performance indicators. At present, however, little evidence can be found that Korean medical and wellness tourism is being managed through such a branding framework. A comprehensive national reassessment is urgently needed — one that asks where Korea is positioned in the global market and what clear value it intends to present to the world.

In building brand equity, it is not necessary to rely solely on assets internal to medical and wellness tourism itself. Secondary leverage points — third-party evaluations, events, media exposure and celebrities — can play a major role in expanding awareness and brand association. A treatment storyline involving the lead character of a K-drama, global social media content featuring Korean doctors, or the validation of Korean medical technology in international journals can all serve as powerful tools of brand leverage.

2. A multilayered architecture for advertising and public relations

Advertising and public relations in medical and wellness tourism serve as the initial market-making activity. By shaping images and providing information about the country and its services, they create awareness and interest among potential customers and move them into the stage of active consideration. Different forms of promotion serve different purposes.

Paid advertising is effective in targeting potential patients by country, age or interest group and in creating direct traffic channels. Official brand and campaign promotion strengthens recognition and trust in a medical tourism brand at the national or city level, helping to build a positive image of the country over the long term. Content- and information-based promotion reduces information asymmetry and supports trust-based decision-making by offering videos, blogs and detailed explanations of treatment processes, physicians and patient experiences. Press relations, public relations and publicity activities — including overseas roadshows, expos and press releases — are especially valuable for establishing credibility and building B2B and B2C networks.

International examples are instructive. Malaysia has built a national brand under the name Malaysia Healthcare, designated 2026 as the “Malaysia Year of Medical Tourism,” and promoted the country with the integrated message, Healing Meets Hospitality. Türkiye, for its part, has adopted an unusually aggressive approach by reimbursing up to 70 percent of social media advertising expenses aimed at overseas prospective patients, thereby encouraging clinics to market globally while using short-form platforms such as TikTok to lower the psychological barrier to entry. Singapore has pursued a different route, using academic and networking events targeted at overseas medical professionals to promote its medical technology and generate patient referrals — in effect, a strategy of doctors marketing to doctors.

3. Refining sales promotion strategy

Sales promotion is what turns recognized demand into actual behavior. By appealing to price, convenience and trust, it encourages real visits, reservations and purchases. It therefore includes all promotion activities other than advertising and public relations. In medical and wellness tourism, such strategies can be designed around four axes: mobility and stay convenience support, price incentives, integrated packages and trust-enhancement mechanisms.

One representative example of convenience support is Turkish Airlines’ discount program for medical tourists, which offers 10 percent off economy fares and 20 percent off business-class fares. The system operates through a formal process in which the patient obtains proof of medical visitation from the hospital and applies for a discount code. On the price-incentive side, the Tourism Authority of Thailand has run a three-way collaborative campaign with medical firms and Visa, offering special discounts on procedures, spas and wellness facilities to ASEAN Visa cardholders. Türkiye, meanwhile, has mandated complication insurance for medical tourists and has the government subsidize up to 70 percent of the premium, thereby institutionally reducing patient risk perception.

In the category of integrated packages, notable examples include the all-inclusive offering of Memorial Hair Transplant Center in Türkiye — priced at about 2,150 euros and including airport pickup, two nights of accommodation, interpretation and coordinator support — and Thailand’s three-to-five-night wellness retreat products. In the area of trust enhancement, Türkiye’s certification system led by USHAŞ and Malaysia’s Flagship Medical Tourism Hospital Program show how state endorsement can provide patients with a clear standard of choice while limiting the unchecked spread of services by uncertified institutions..

IV. A Sustainable Ecosystem Strategy for Medical and Wellness Tourism

No matter how impressive the content in medical and wellness tourism may be, growth will eventually reach its limits unless it is supported by a productive and sustainable ecosystem. In the end, the creation of such an ecosystem is what determines industrial competitiveness. That requires three things to move together: a collaborative governance structure, an efficient value chain that integrates production, distribution and consumption, and a performance-based evaluation system.

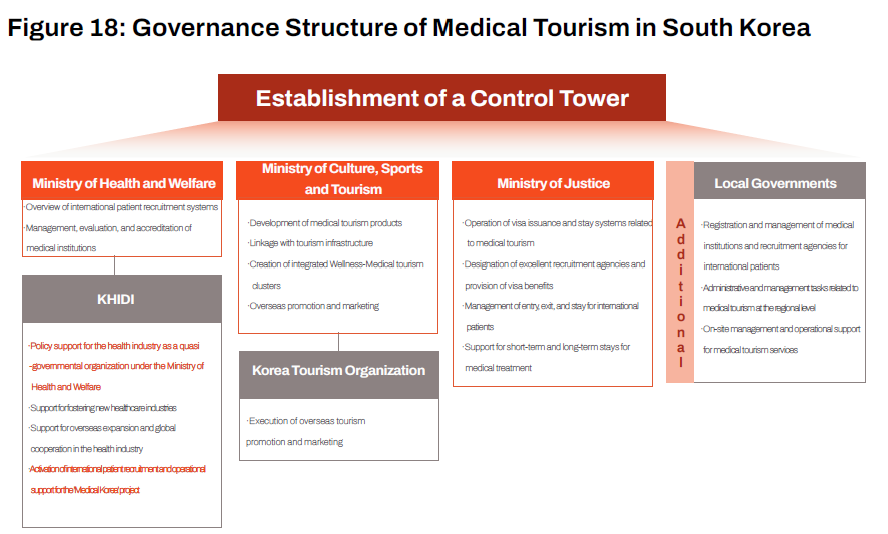

1. Building a collaborative governance system

One of the central tasks in ensuring the sustained growth of South Korea’s medical and wellness tourism industry is to build an organic system of cooperation among the ministries and institutions involved, thereby maximizing policy synergy. At present, Korea’s medical tourism ecosystem is shaped by a wide range of actors: the Ministry of Health and Welfare, which oversees medical institutions and the foreign-patient recruitment regime; the Ministry of Culture, Sports and Tourism, responsible for tourism products and marketing; the Ministry of Justice, which handles entry and visa matters; the Korea Health Industry Development Institute; the Korea Tourism Organization; and local governments, among others.

Because the industry is inherently convergent, the impact of each ministry’s strengths is multiplied when they are effectively connected — whether in the form of integrated package development or large-scale global promotion. The analogy is orchestral. Each instrument may produce beautiful sound on its own, but only through coordination and communication does it become a symphony. The need, therefore, is for a robust interministerial network that respects the independent expertise of each institution while linking those competencies more seamlessly.

The examples of leading countries illustrate the point. In Türkiye, USHAŞ, operating under the Ministry of Health, works closely with the tourism promotion authority under the Ministry of Culture and Tourism through formal agreements, allowing the two bodies to coordinate public and private activities, complement service standards and jointly support the HealthTürkiye platform. Türkiye also runs an advisory structure composed of medical institutions and intermediaries, ensuring that the voice of the field is reflected in policy. In Malaysia, MHTC serves as a coordinating body under the Ministry of Health, managing the national brand, hospital quality certification and even patient-dedicated airport lounges while also strategically expanding its global appeal through initiatives such as faith-friendly medical service models.

South Korea, too, has reached the point where it should elevate its own cross-government cooperation. The country already possesses world-class infrastructure and substantial policy know-how. What is needed now is a stronger collaborative network that preserves each ministry’s authority and administrative specialization while aligning shared performance indicators and a common policy vision. If ministries can work together more flexibly on convergent issues — relaxing medical advertising rules, institutionalizing Meditel certification, issuing long-term visas tailored to medical tourism, or jointly applying regulatory sandboxes — then the global competitiveness of Korea’s medical and wellness tourism industry could expand dramatically.

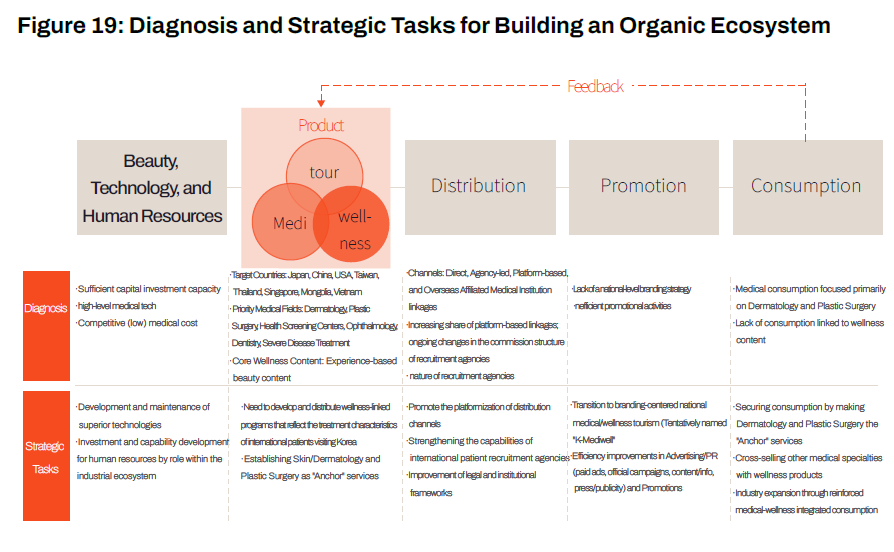

2. Building an organic industrial ecosystem

From capital, technology and labor inputs to product development, distribution, promotion and consumption, the entire industrial ecosystem of medical and wellness tourism must be organically connected. South Korea’s current position is mixed. On the one hand, it possesses excellent medical technology, ample capital capacity and a relatively affordable medical-cost structure. On the other, it continues to suffer from structural weaknesses: concentration in dermatology and plastic surgery, insufficient linkage with wellness content, the small scale of recruitment businesses, the absence of a national branding strategy and inefficient promotional systems.

Within this ecosystem, one challenge deserves particular attention: the specialization of human capital. In high-end services, the final point of contact that digital technology cannot replace is ultimately human. South Korea should therefore institutionalize a nationally certified professional category of Medical Wellness Concierge — experts capable of understanding clinical charts, accompanying patients from arrival to surgery, and overseeing even psychological recovery at wellness resorts in a deeply personalized, one-on-one way. Serving global VIP patients requires much more than interpretation. It calls for hybrid professionals with medical knowledge, cultural sensitivity and tourism-planning ability all at once.

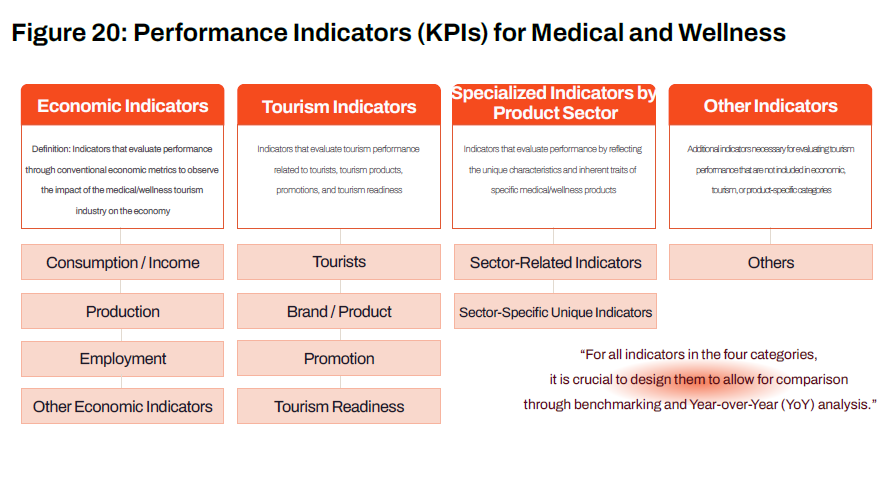

3. A performance-based evaluation system: SMART KPIs and multilayered indicators

To ensure the execution and sustainability of activation strategies in medical and wellness tourism, an integrated performance-indicator framework is essential. All core KPIs should be designed according to the SMART principle: they must be specific, measurable, attainable, relevant and time-bound. Evaluation should also combine relative indicators benchmarked against peer competitors with absolute year-on-year indicators, in order to strengthen objectivity.

These indicators may be grouped into four categories. The first is economic indicators, which quantify the direct and indirect ripple effects of the industry on the national economy, including tourism revenue, induced production, induced value added and employment creation. The second is tourism indicators, which measure both the scale and quality of demand through total visitor numbers, patient counts by nationality, average length of stay, satisfaction, revisit rates, brand awareness and brand associations. The third consists of sector-specific indicators, reflecting the distinctive structure of the industry, such as the linkage rate between medical and wellness products, sales rates of high-value products and measures of linkage with local economies and cultures. The fourth includes other sustainability indicators, such as ESG performance, crisis-response systems for medical tourism, and the number of lawsuits and civil complaints involving medical tourists — all of which shape long-term resilience beyond purely financial terms.

Concluding Remarks: K-MediWell as a National Strategic Asset for South Korea’s Next Fifty Years

For decades, South Korea’s inbound tourism industry was driven by a model of quantitative expansion centered on shopping. That model is now approaching a decisive structural turning point. The record-breaking performance of 2024 — 1.17 million foreign patients and 1.4 trillion won in medical revenue — is certainly encouraging. Yet beneath those impressive numbers lies a serious structural imbalance: nearly 70 percent of demand is concentrated in beauty procedures, while more than 85 percent of visitors are clustered in the Seoul metropolitan area. With such a fragile industrial structure, the sector will struggle to respond flexibly to external economic shocks or shifts in consumer trends. If long-term sustainability is to be secured, a fundamental restructuring is no longer optional; it is essential.

The global health care market is already undergoing a profound transformation. Medical care, once centered primarily on the clinical treatment of disease, is increasingly being integrated with wellness, which encompasses prevention, recovery and long-term management. Together, they are forming a single and expanding continuum of value. The global wellness economy, projected to reach approximately $9.75 trillion by 2029, is drawing in not only affluent consumers seeking sophisticated medical and longevity services, but also a far broader population — including patients from countries whose public health care systems are faltering under the weight of delay, shortage and dysfunction.

In the midst of this transformation, South Korea must move decisively beyond the fragmented approaches of the past if it hopes to outpace competitors such as Thailand, Türkiye and Singapore and emerge as a true global health care hub. The immediate priority is clear: to activate an interministerial network of cooperation and build, at the national level, an integrated brand and a sophisticated digital platform. Above all, South Korea must adopt a comprehensive cross-selling ecosystem that uses K-beauty as a powerful anchor of demand and links it strategically to the country’s regional wellness assets and high-value regenerative medicine. That model — K-MediWell — offers perhaps the most realistic and essential pathway for the qualitative transformation of South Korea’s tourism industry.

According to Yanolja Research, if this strategy is implemented successfully, the number of medical and wellness tourists could reach 6.87 million by 2030, with total spending rising to 17.5 trillion won. Input-output analysis further suggests that by 2030 the sector could generate 32 trillion won in production inducement effects, 14 trillion won in value-added effects, and 190,000 jobs. In that scenario, medical and wellness tourism would stand not merely as another tourism segment, but as one of the country’s most powerful high-value economic engines.