SooCheong Jang / Professor, Purdue University & Director, Yanolja Research / [email protected]

Kyuwan Choi / Professor, Kyung Hee University & Director, H&T Analytics Center / [email protected]

South Korea’s tourism industry today resembles a “leaking barrel.” Despite continuous efforts to pour water in by attracting inbound tourists, far more water is leaking out through outbound travel, preventing the level from ever rising in a meaningful way.

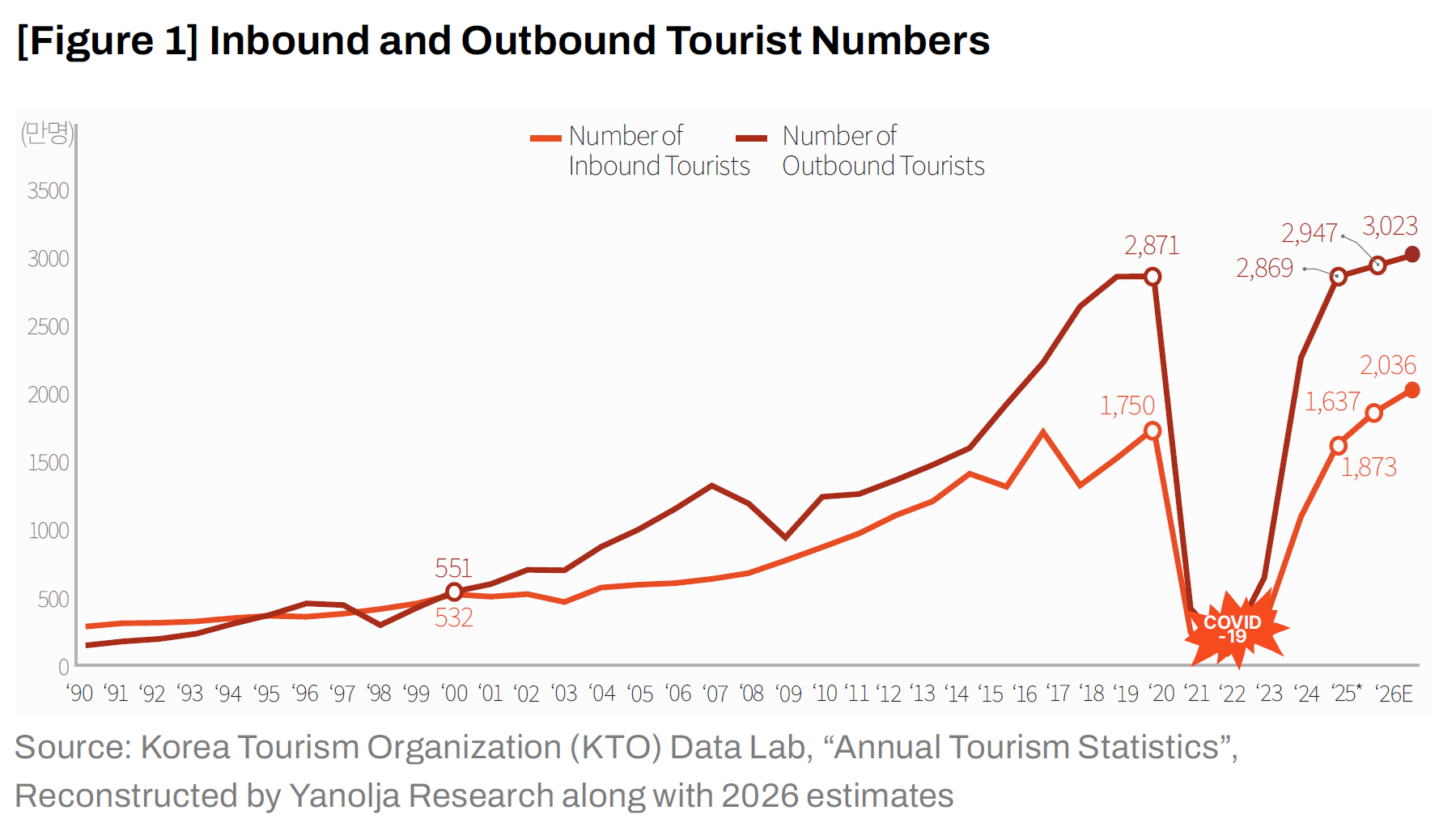

As previously reported by Yanolja Research Insights, inbound arrivals to South Korea are projected to exceed 20 million in 2026, while outbound travel by Koreans is expected to reach 30 million. As a result, more than 50 million cross-border movements may occur in a single year—marking what could be described as a “year of mass mobility.” Beneath this quantitative expansion, however, lies the risk of a deeply entrenched structural imbalance, with a gap of nearly 10 million travelers between inbound and outbound flows. This is not merely a numerical discrepancy; it is a warning signal revealing a structural deficiency in the tourism ecosystem’s “attractiveness capital.”

This problem was already evident in past performance. In 2019, when 17.5 million foreign tourists visited Korea, as many as 28.71 million Koreans traveled abroad—meaning that more than half of the population crossed national borders for travel. After the long tunnel of COVID-19, suppressed travel demand burst forth with the onset of the endemic phase, producing a harsh outcome: in 2024, South Korea recorded a record-high tourism balance deficit of approximately USD 10 billion (about KRW 14.5 trillion).

Crucially, this deficit is not a temporary phenomenon. Yanolja Research forecasts that inbound arrivals in 2026 will grow to an all-time high of approximately 20.76 million (up to 21.26 million under optimistic scenarios), while outbound travel will simultaneously rise to 30.23 million, also setting a new record. In other words, outbound travel continues to expand at the same pace as inbound growth, and the “10-million-person gap” shows little sign of narrowing. This implies that national wealth painstakingly earned through exports such as semiconductors and automobiles is structurally leaking overseas through travel-related experiential consumption.

This imbalance between inbound and outbound tourism goes beyond statistical deficits; it gradually drains the lifeblood of regional economies. The more citizens open their wallets abroad, the more domestic restaurants, accommodations, traditional markets, and neighborhood commercial districts lose vitality and face the risk of decline. Viewed from the opposite perspective, revitalizing intra-bound tourism—domestic travel in which citizens voluntarily spend because they perceive genuine enjoyment and value—is the most reliable and sustainable form of domestic economic stimulus, as well as a realistic solution for balanced regional development.

This brings the central question into sharp focus: why do people choose to travel abroad rather than domestically? The answer is surprisingly simple—consumers are rational. As the Korean saying goes, “given the same price, one chooses the better option.” When costs are similar, choosing Japan or Southeast Asia, which offer better service and more distinctive experiences, is a perfectly rational consumer decision. Appeals such as “travel domestically out of patriotism” no longer carry persuasive power.

Japan’s experience offers important lessons in this regard. Japan has endowed each of its regional cities with a distinct identity and built a domestic tourism market rich in detailed content—so compelling that not only foreign visitors but even its own citizens wish to return repeatedly. It has become a country where one can fully enjoy travel without leaving. This clearly demonstrates that the path forward lies not in price competition, but in creating irreplaceable attractiveness that cannot be substituted by alternative destinations.

This Insight begins from that critical awareness. Using 2026 demand forecasts, we aim to provide a sober diagnosis of the tilted playing field facing Korea’s tourism industry. In particular, despite the positive milestone of entering the era of 20 million inbound visitors, we closely examine the structural asymmetry driven by the still-overwhelming scale of outbound travel. Furthermore, by benchmarking Japan’s successful formula, we seek practical strategies for revitalizing domestic tourism.

What is needed is not forced or superficial campaigns, but a redesign of attractiveness that leads consumers to voluntarily choose domestic travel. This is the only viable solution to filling an annual tourism deficit exceeding KRW 14 trillion and restoring warm circulation to regional economies. We hope this report provides policymakers, tourism industry practitioners, and academic researchers with practical insights and inspiration to turn crisis into opportunity.

An examination of Korea’s tourism performance over the past several years reveals a striking divergence between inbound tourism (foreign visitors to Korea) and outbound tourism (Korean residents traveling abroad), as if the two were governed by entirely different gravitational forces. In particular, the asymmetric recovery observed in the post-pandemic period has laid bare the structural fragility of Korea’s tourism industry.

The year 2019 serves as a critical benchmark for understanding this imbalance. Even at that time, the number of outbound Korean travelers already exceeded inbound foreign visitors by a factor of 1.6. However, developments in the endemic era have demonstrated that this gap was not a temporary anomaly. According to 2024 statistics, outbound travel rebounded fully to 28.72 million trips, achieving a 100% recovery relative to 2019. Suppressed demand for overseas travel surged back like a compressed spring. In contrast, inbound tourism reached 16.96 million visitors, recovering only 93.5% of its pre-pandemic level.

This imbalance is expected to persist through 2026. According to Yanolja Research’s LSTM-based forecasting model, inbound arrivals could reach up to 21.26 million under an optimistic scenario that incorporates positive spillover effects—such as the rebound driven by the weak Japanese yen—marking the first time Korea surpasses the 20-million inbound visitor threshold. Nevertheless, outbound demand is projected to rise simultaneously, reaching approximately 30.23 million trips, exceeding its pre-pandemic peak.

As a result, the gap between inbound and outbound tourism—nearly 10 million travelers—is likely to remain intact. This underscores that the imbalance cannot be resolved through simple policies aimed solely at increasing visitor numbers. As the global tourism market transitions from recovery to a phase of sustained growth, Korea’s tourism industry stands at a critical crossroads. It must confront a structural contradiction in which the exit door remains significantly wider than the entrance.

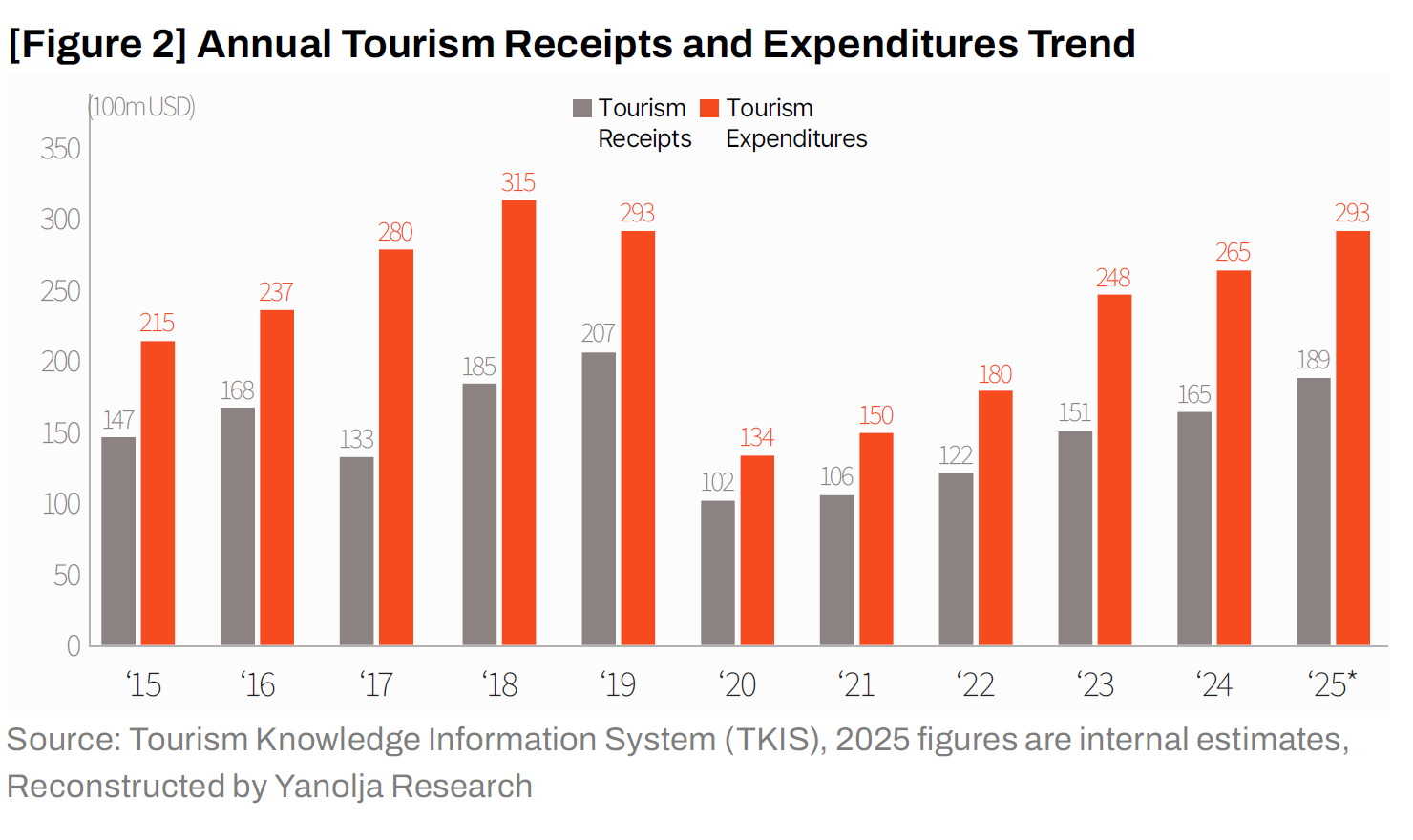

This asymmetric pattern of recovery has translated into an astronomical tourism balance deficit. During the pandemic, when cross-border travel was largely suspended, the deficit temporarily narrowed. However, once international air routes reopened, the gap widened rapidly and uncontrollably. The tourism deficit, which stood at approximately USD 9.7 billion in 2023, surpassed an all-time high of over USD 10 billion in 2024.

The stark contrast between foreign visitor spending in Korea (USD 16.45 billion) and Korean residents’ spending overseas (USD 26.49 billion) highlights a fundamental structural weakness. Korea’s tourism industry is trapped in a leakage-driven system in which foreign exchange earnings generated domestically are not effectively retained or circulated within the national economy, but instead flow outward at an accelerating pace.

Behind the USD 10 billion tourism deficit lies a deep-rooted structural factor: a persistent mismatch between demand (consumers) and supply (tourism infrastructure, products, and services). This is why the imbalance cannot be explained solely by post-pandemic “revenge consumption.”

On the demand side, Korean consumers’ expectations for travel experiences have risen sharply. Improvements in income levels, coupled with decades of travel liberalization and accumulated overseas travel experiences, have significantly raised the bar. For the trend-leading Millennial and Generation Z cohorts, travel is no longer merely a form of rest or leisure; it has become a process of acquiring “experience capital”—something to be recorded, shared, and validated through social media. These consumers pursue rational choices: “If the cost is similar, they prefer destinations that offer a more distinct sense of foreignness and demonstrably higher-quality service.” Japan, with its enhanced price competitiveness driven by a weak yen, and Southeast Asia, known for its exotic landscapes and unique atmospheres, have emerged as highly attractive substitutes. When domestic destinations fail to deliver an experience density that matches these elevated expectations, consumers do not hesitate to head for Incheon International Airport.

On the supply side, the challenges are equally severe. Korea’s tourism sector continues to suffer from a chronic concentration around Seoul and a shortage of compelling content. The fact that 70–80% of foreign visitors are concentrated in Seoul and the surrounding metropolitan area creates a double-edged problem: overtourism for the capital region and a growing risk of decline for provincial areas. Even more concerning is the response from regional destinations. Rather than uncovering and cultivating distinctive local content to create “irreplaceable appeal,” many regions have focused on replicating hardware-based facilities such as suspension bridges and cable cars. This approach has fostered the perception—among both foreign visitors and domestic travelers—that destinations across the country all look and feel the same. The absence of compelling local narratives and experiences ultimately accelerates outbound travel among Koreans while reinforcing the perception among foreigners that “once you have visited Seoul, there is little else to see in Korea.” This vicious cycle continues to deepen.

Ultimately, the current imbalance is not a temporary trend but a structural outcome of a stagnant supply system that has failed to keep pace with increasingly sophisticated demand. In the following section, we examine how these structural weaknesses manifest in actual consumer perceptions, offering an in-depth analysis of the psychological barriers and preference gaps between domestic and international travel choices.

The process by which consumers choose a travel destination is not a simple arithmetic calculation based on distance or cost. Rather, it is a rigorous exercise in value judgment—an assessment of what kind of psychological satisfaction one can obtain in return for investing time and money. Behind the current outbound-oriented travel bias facing Korea’s tourism industry lies a deeply embedded combination of psychological dualism and a collapse of trust capital within consumers’ cognitive frameworks when comparing domestic and international travel.

1. Asymmetry Between “Dopamine (Excitement)” and “Serotonin (Comfort)”

For consumers, international and domestic travel activate fundamentally different neurological response mechanisms. International travel is primarily driven by the pursuit of novelty and new stimulation. The tension and exhilaration generated by unfamiliar, foreign environments trigger what can be described as a dopamine-driven response. Domestic travel, by contrast, is perceived as the pursuit of rest and stability within familiar language, culture, and surroundings—a serotonin-driven experience.

The problem is that when consumers open their wallets, they tend to assign far greater value to extraordinary adventures than to simple relaxation. For the Millennial and Generation Z cohorts, who shape contemporary consumption trends, international travel represents a life highlight and a tangible investment—an experience that can be documented and leveraged for personal branding on social media. Domestic travel, on the other hand, is often relegated to an extension of the weekend or a casual outing that can be taken at any time. As long as the cognitive frame of “international travel as a true journey, and domestic travel as a brief getaway” persists, domestic travel will face structural limitations in surpassing the perceived attractiveness of overseas trips.

2. The Value Gap: “Domestic Travel Is Expensive Even at Half the Price”

These psychological distinctions translate directly into hard economic value assessments. The fundamental reason consumers turn away from domestic travel is not a lack of financial capacity, but rather the perception that domestic tourism products fail to deliver commensurate value for the price paid.

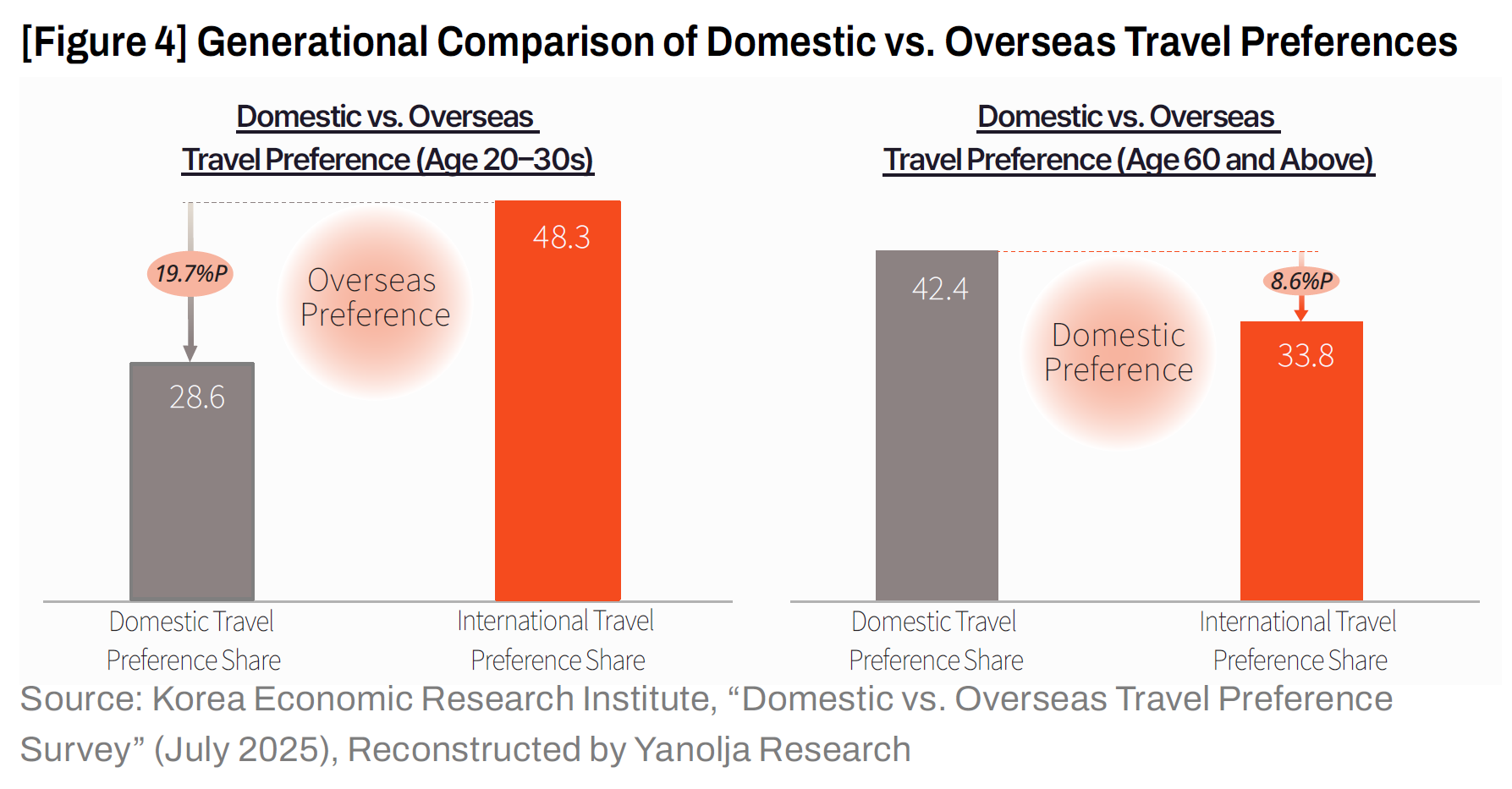

Survey results from Yanolja Research vividly illustrate this psychological discount rate. Fifty-four percent of respondents indicated that while they would consider domestic travel instead of an overseas trip, they would be willing to pay only 30–50% of the budget they would allocate to international travel. Only 18% expressed a willingness to spend an equivalent amount. This suggests that on consumers’ internal balance sheets, domestic travel is valued at less than half the worth of international travel. In psychological terms, current domestic travel is positioned as a low-cost substitute—chosen primarily when overseas travel is not an option.

At this point, a powerful comparative heuristic comes into play: “For this amount of money, I might as well…” For example, when a one-night stay at a private pool villa in Gangwon Province approaches KRW 500,000, consumers immediately begin to compare it with a five-star resort in Da Nang, Vietnam, or a traditional ryokan in Japan. Even if the absolute cost of traveling abroad is higher, consumers perceive the utility gained per unit of expenditure—in other words, satisfaction relative to price—as significantly greater overseas. This is the outcome of a rational economic judgment rather than an emotional impulse.

3. The Depletion of Trust Capital Driven by “Overcharging” and “Replication”

What ultimately delivers a decisive blow to already low value perceptions is the collapse of trust. Recurrent controversies during peak vacation seasons—such as excessive accommodation price hikes and outrageously priced food at local festivals (e.g., the “fat-only pork belly” incident)—have moved consumers beyond mere price resistance to a sense of betrayal. Behavioral economics suggests that consumers are more likely to close their wallets not simply when prices are high, but when they perceive pricing to be unfair. The self-deprecating belief that “traveling domestically means being taken advantage of” risks becoming an irreversible broken-window effect.

By contrast, the essence of Japan’s travel boom lies not merely in the weak yen, but in predictability. Whether at a convenience store in Tokyo or a rural ryokan, Japan consistently delivers standardized service quality aligned with transparent, fixed pricing. Consumers choose Japan with the confidence that “at the very least, I won’t be overcharged, and I won’t fail.” In this sense, domestic travel in Korea has come to represent an uncertain, high-cost risk, while travel to Japan has evolved into a reliable form of consumption with assured returns.

4. Generational Perception Gaps and the Risk to the Future

Perhaps most troubling is the long-term outlook. Today’s domestic tourism market is being sustained largely by the inertial demand of older generations, including those in their 50s and 60s, for whom overseas travel may be constrained by language barriers or health considerations. Meanwhile, the 20–30 age cohort, which will dominate future consumption, engages with the world in real time through social media and faces few psychological barriers to international travel. For them, domestic travel appears to have been relegated to a secondary option—chosen only when overseas travel is not feasible. There is little reason to expect that these consumers will naturally “return” to domestic travel as they age. This signals a structural warning: over time, the support base for domestic tourism may erode irreversibly.

Reinterpreted this way, on consumers’ internal balance sheets, domestic travel is categorized as an inferior good—offering lower appeal at a disproportionately high cost compared to international travel. Without dismantling this deeply entrenched psychological barrier, appeals to patriotism or simple measures such as discount coupons will be insufficient to reverse the prevailing trend.

The question, then, is how this impasse can be overcome. Fortunately, there exists a compelling case of a country that confronted a remarkably similar challenge and achieved a dramatic turnaround: Japan. Once struggling with stagnant domestic demand and declining tourism appeal, Japan reinvented itself as a global tourism powerhouse through bold policy shifts and meticulous content innovation—while simultaneously revitalizing domestic travel to its regional areas.

How Japan transformed declining provincial regions into destinations people genuinely want to visit offers powerful lessons. Its concrete strategies provide valuable insights for Korea as it seeks a sustainable path forward.

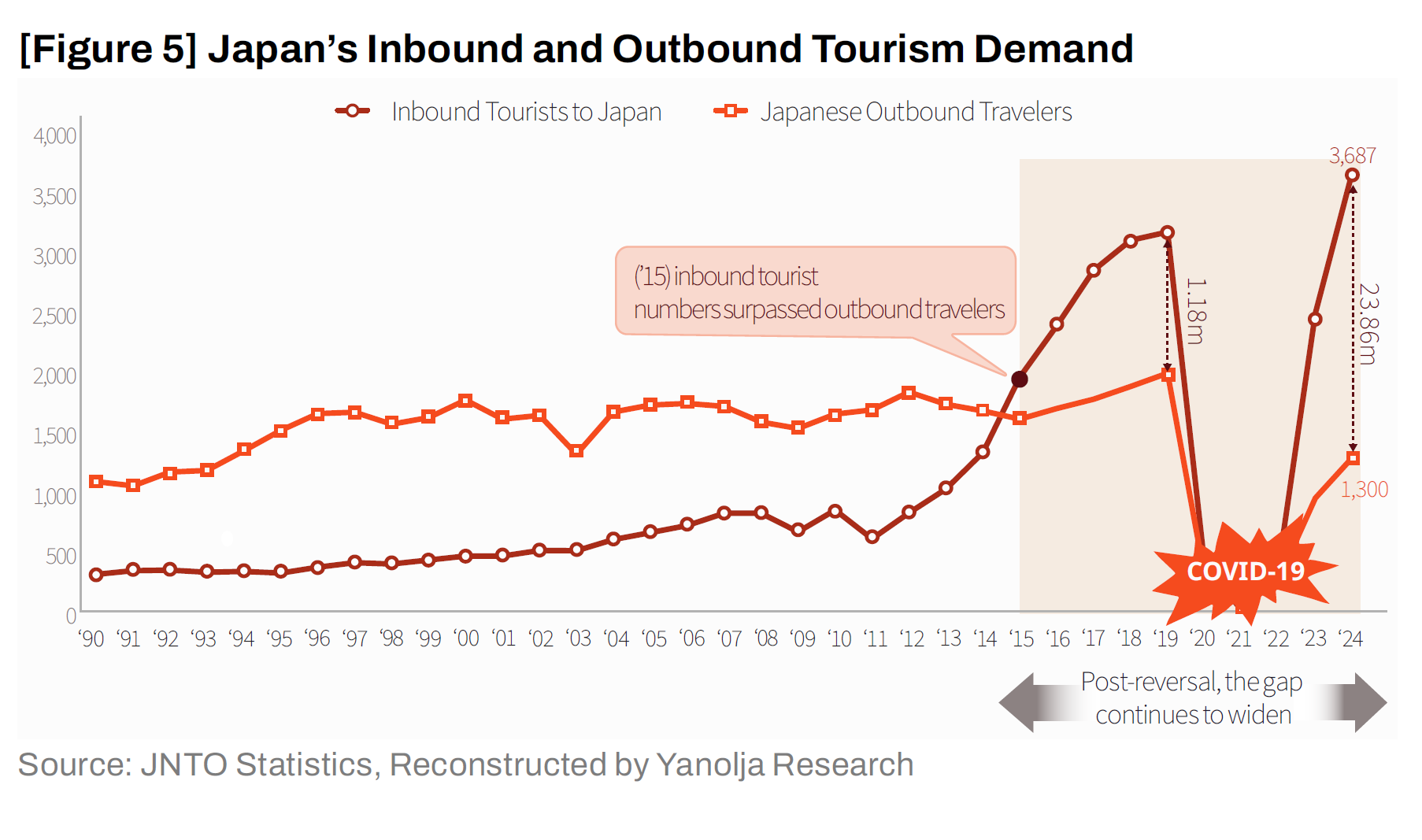

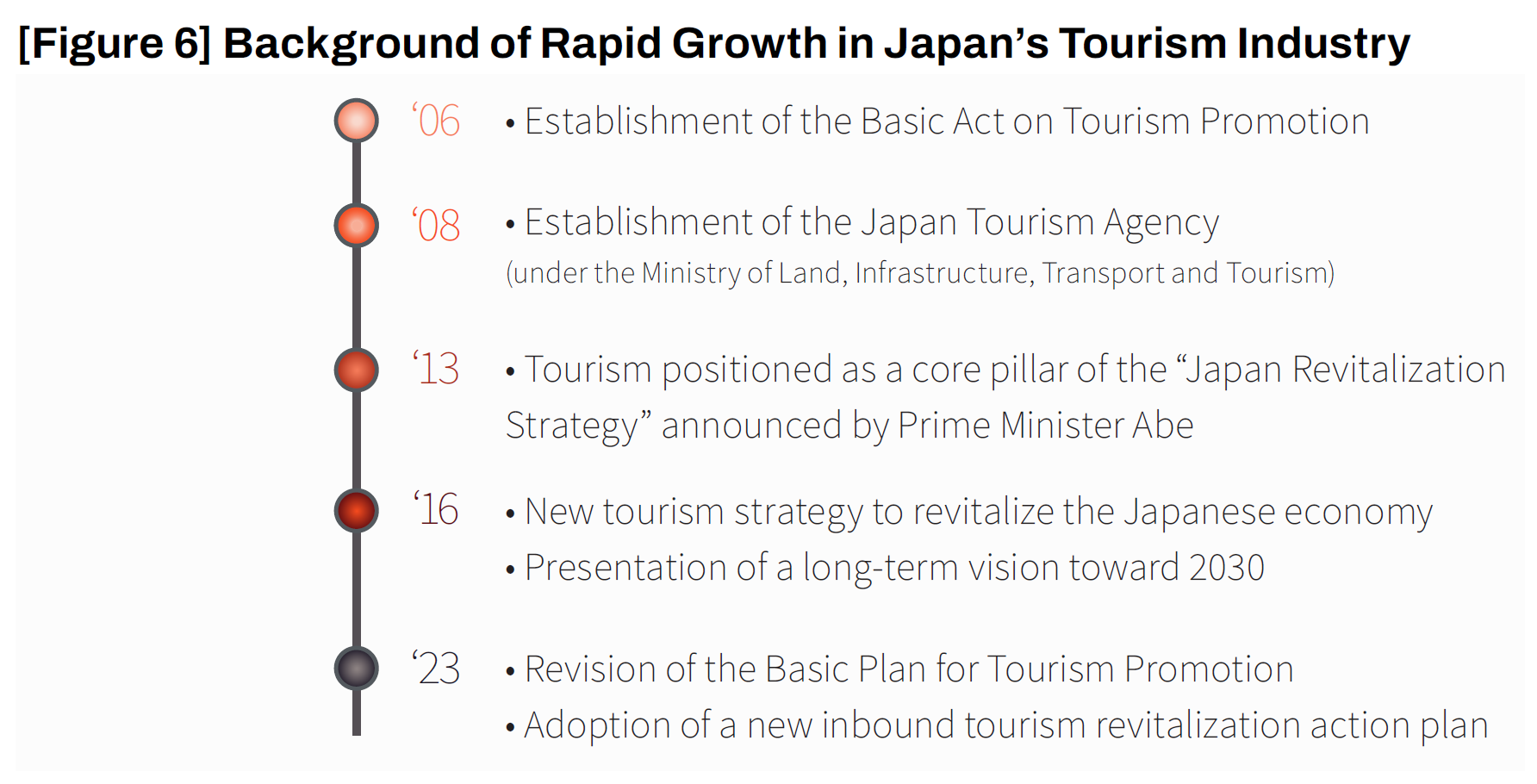

The imbalance and regional decline currently confronting Korea’s tourism industry are, in fact, challenges that Japan experienced more than a decade earlier. However, Japan transformed this crisis into an opportunity for a dramatic turnaround by wielding tourism as a strategic instrument. Amid the prolonged stagnation symbolized by the so-called “Lost Two Decades,” Japan redefined tourism not merely as a leisure industry, but as a core pillar of national growth strategy and a breakwater against regional extinction.

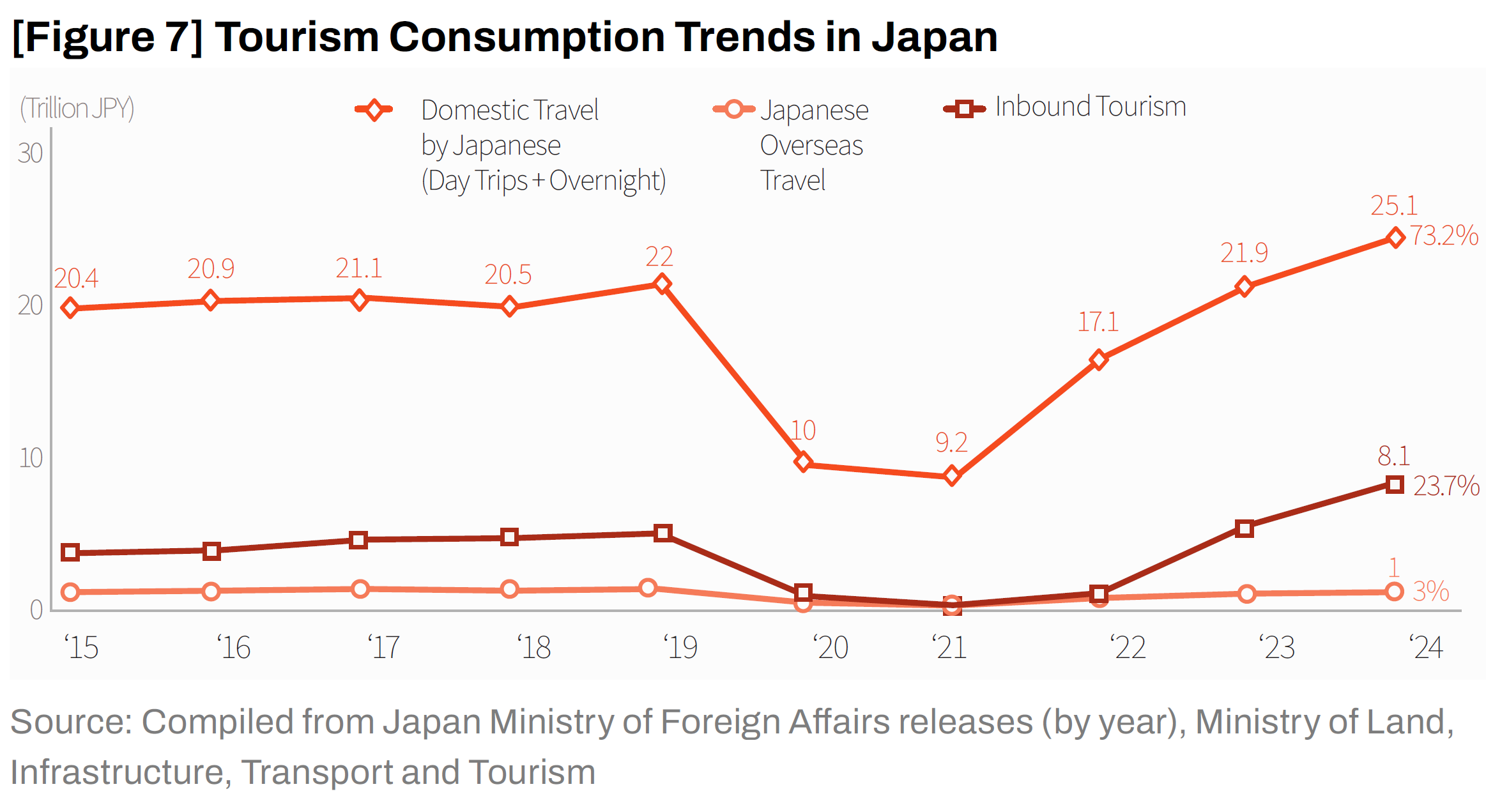

In particular, following the launch of the Abe administration in 2012, Japan adopted “tourism-oriented nation-building” as a national agenda and set an ambitious target of attracting 60 million inbound tourists by 2030. As a result, the number of foreign visitors to Japan surged vertically—from around 10 million in 2013 to 31.88 million in 2019—while total travel expenditures reached JPY 4.8 trillion (approximately KRW 45 trillion).

How did Japan shed its reputation as a tourism laggard and rise so rapidly to become a global tourism powerhouse? At the heart of this success lie two key drivers explored below: “innovation through detail” and “the rediscovery of regional Japan.”

First, [Infrastructure Innovation] Clearing Blocked Arteries: Connecting LCCs and Regional Airports

Japan’s first decisive move was to remove the physical barriers that prevented foreign visitors from traveling directly to regional areas. Rather than relying solely on the major arteries of Tokyo and Osaka, Japan transformed 22 regional airports across the country into international gateways. In particular, it actively attracted foreign low-cost carriers (LCCs) and developed dense secondary transportation networks—such as shuttle buses and rail passes—linking regional airports to major tourist destinations.

This effectively opened direct air routes that allow visitors to fly straight to Hokkaido’s snowy landscapes or Kyushu’s hot springs without passing through Tokyo. As a result, the regional distribution of foreign visitors in 2019 achieved a relatively balanced spread: Tokyo (47%), Osaka (38%), Kyoto (35%), and Kanagawa (28%). This stands in stark contrast to Korea’s reality, where 70–80% of inbound tourists remain concentrated in Seoul. Through transportation infrastructure innovation, Japan dramatically improved accessibility to regional destinations and successfully expanded tourist flows nationwide.

Second, [Governance Innovation] Establishing DMOs as the “Control Towers” of Regional Tourism

A hidden driver behind Japan’s tourism success is the DMO (Destination Management Organization) system. Japan moved away from a passive model in which the central government allocates budgets and local governments merely execute them. Instead, it introduced DMOs nationwide as public–community partnership organizations, where local governments, private businesses, and residents jointly manage regional tourism.

These organizations go beyond simple promotion. They identify local attractions, conduct data-driven target marketing, generate revenue, and reinvest profits back into the community—effectively practicing tourism management rather than tourism administration.

Third, [Content Innovation] Competing with “Only One” Themes

Rather than adopting a department-store-style approach of “showing everything,” Japan chose a strategy of creating a single, decisive killer content for each region. Hokkaido positioned itself around “powder snow,” becoming a global mecca for skiers; Okinawa branded itself as the “Hawaii of Asia”; Kyoto emphasized “the most authentic Japanese tradition”; and Kyushu highlighted “hot springs and gastronomy.” Each region clearly defined its unique identity.

Equally notable is the regeneration of content driven by private-sector creativity. Tourist trains built on abandoned railway lines, luxury hotels converted from vacant traditional houses, and artist residency programs utilizing empty rural homes transformed aging assets into symbols of “hipness.” This diversity of content instilled not only foreign visitors but also domestic travelers with the perception that “there are still many places worth visiting within Japan,” thereby energizing intrabound tourism (domestic travel by residents).

The message Japan’s dramatic revival delivers to Korea is unmistakably clear. Success in tourism does not come from cosmetic touch-ups—such as slick promotional videos or one-off festivals. Without painful infrastructure reform and a fundamental redesign of the system’s “software,” a country may create short-lived trends, but it cannot build a sustainable tourism industry. Drawing on Japan’s success formula, the core lessons Korea must benchmark can be distilled into three key priorities.

First, a revolution in regional accessibility that breaks Seoul-centricity

Korea’s tourism system remains structurally centralized, with virtually all roads leading to Seoul. For foreign visitors, traveling to regional destinations almost inevitably requires passing through Incheon International Airport and Seoul, creating an inefficient and discouraging travel flow. This model—over-supplying tourism “blood” to the single heart of Seoul—must be abandoned.

Like Japan, Korea needs to activate regional airports as direct international gateways, opening “expr

ess pipelines” that allow foreign visitors to enter regional areas directly. At the same time, dense secondary transportation networks must connect airports to tourist destinations so that tourism flows reach even the smallest capillaries. Without accessibility, regional tourism remains little more than an illusion.

Second, institutionalizing privately led DMOs that move beyond government rigidity

Administratively driven, desk-bound policymaking cannot keep pace with rapidly evolving travel trends. What is needed is a functional control tower—a privately led DMO driven by market experts and local residents who understand demand dynamics firsthand.

Working in coordination with domestic and global OTAs, these organizations must set targets based on data, execute creative marketing strategies, generate revenue, and reinvest profits locally. Under a clear principle of government support without interference, the role of the public sector is to create an environment in which private-sector dynamism and creativity can fully flourish.

Third, abandoning replication and restoring originality

The era of copy-and-paste development—in which local governments compete to build suspension bridges and cable cars—must come to an end. Similar landscapes and souvenirs everywhere cannot meet the heightened expectations of today’s consumers. Instead, destinations must uncover stories and experiences rooted in their own history, culture, and lifestyle.

In tourism, the adage “the most local is the most global” holds true. Only when destinations compete through irreplaceable originality rather than imitation do consumers truly open their wallets.

Ultimately, the essence of Japan’s success lies in building a virtuous ecosystem: attracting people to regional areas through tourism and ensuring that their spending circulates within local economies as a source of renewed vitality. This is the genuine lesson Korea must learn from Japan.

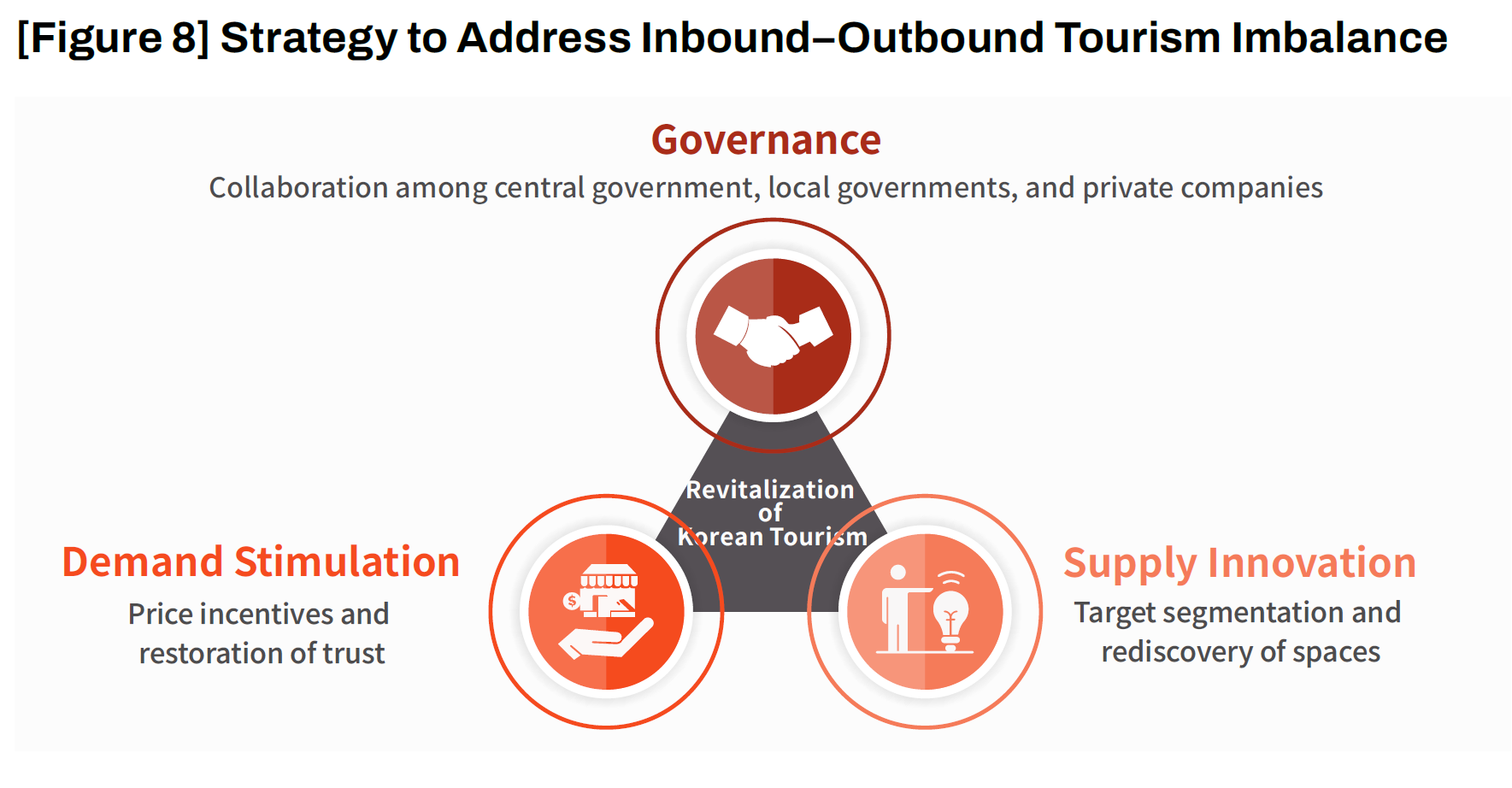

As discussed above, consumers’ reluctance to choose domestic travel stems from two fundamental problems: a deficit in attractiveness capital and a collapse of trust. The solution, therefore, is clear. Rather than adopting protectionist measures to artificially restrict outbound travel, Korea must redesign the playing field so that intrabound travel (domestic travel by residents) becomes the more attractive and rational choice. Achieving this requires a three-pronged approach: content innovation on the supply side, psychological incentives on the demand side, and a governance framework to support both.

First, [Supply Innovation] There Is No Tourism for “Everyone”: Target Segmentation and the Rediscovery of Space

To shed the stigma that “there is nowhere to go in Korea,” a precision targeting strategy must be combined with the upcycling of space. Bland tourism products designed for the entire population are no longer effective.

① MZ Generation Seeking Dopamine and “Hipness”: Regenerated Spaces and Activities

For younger travelers, travel is a form of self-validation. What they seek is space upcycling—reinterpreting the old through a contemporary lens. Examples include F1963 in Busan, which transformed a former industrial plant into a cultural complex, and the rise of Mullae-dong’s metal workshop alley as a hip destination. Idle spaces—such as closed schools, abandoned factories, and old downtown districts—must be infused with art and storytelling. These spaces should be paired with dopamine-inducing activities such as surfing, paragliding, and e-sports festivals, prompting reactions like, “I didn’t know Korea had places this cool.”

② Middle-Aged and Senior Travelers Seeking Quality and Rest: Premium Wellness and Storytelling

For economically stable travelers in their 40s to 60s, low-cost package tours can be counterproductive. This group values high-end experiences that deliver genuine hospitality, even at a higher price. Deep-content offerings—such as Southern coastal gastronomy tours, premium wellness retreats at mountain temples, and private heritage tours with local artisans—are essential. For seniors aged 60 and above, combining comfortable transportation with nostalgia-driven retro travel (modern history tours, film-location visits) can establish a new standard for senior tourism that is more comfortable than overseas travel yet emotionally fulfilling.

③ Spatial Scaling: Connecting “Points” into “Lines” and “Areas”

Individual local governments cannot compete alone. Just as Japan’s Setouchi became a global destination by linking islands across seven prefectures, Korea must develop cross-jurisdictional regional tourism routes. Initiatives such as a Southern Coast Marine Belt or a Baekdudaegan Ecological Route—designed as two- to three-night stay itineraries—are essential for regional tourism beyond Seoul to become competitive.

Second, [Demand Incentives] Breaking Price Resistance and Rebuilding Trust

Once attractive products are in place, triggers are needed to persuade consumers to open their wallets. This must proceed on two tracks: economic incentives and the restoration of psychological trust.

① Restoring Trust by Eliminating the “Overcharging” Stigma.

The most urgent task is rebuilding trust. The greatest enemy of domestic travel is uncertainty. Central and local governments should institutionalize price monitoring in tourist destinations and introduce quality certification systems that guarantee service levels relative to price. When consumers recognize that “places with this mark can be trusted,” suspicion can turn into confidence.

② Priming the Pump: Price Incentives and Vacation Culture Reform

To stimulate early demand, bold pricing policies are essential. Making the Lodging Sale Festival permanent and expanding tax deductions for domestic travel expenses would provide tangible incentives. At the same time, institutionalizing workations and staggered vacation systems can normalize travel as part of everyday life, redistributing demand from weekends and peak seasons to weekdays and off-peak periods.

Third, [Governance] A Tourism Symphony That Moves “Separately, Yet Together”

Even the finest score becomes noise if the musicians are out of sync. Structural reform in tourism can succeed only when central government policy, local execution, and private-sector creativity are orchestrated with precision. This requires a redefinition of roles for each stakeholder.

① Central Government: The “Conductor” Who Sets the Stage and Coordinates

The central government’s role is not micromanagement, but creating the overarching framework. A whole-of-government control tower must align fragmented tourism policies across ministries. Most importantly, the government must remove regulatory sandbags and open transportation arteries so that local governments and the private sector can move freely. Activating regional airports, expanding KTX networks, and implementing bold deregulation (e.g., expanding tourism special zones) are the conductor’s core responsibilities.

② Local Governments & DMOs: “Field Commanders” on the Front Lines

Local governments operate at the front line, but real authority should rest with DMOs that organically integrate private experts, residents, and municipalities. When these organizations lead place-based branding and exercise autonomy over budget execution, vibrant local marketing can replace standardized, formulaic festivals.

③ Private Companies & Startups: “Innovators” Who Bring the Music to Life

Ultimately, it is the private sector that plays the melodies that captivate consumers. Travel-tech companies—including NOL Universe—must leverage big data to deliver personalized services and reduce information asymmetry. Regional startups should develop killer content with fresh ideas, while large firms drive qualitative growth through bold investments in landmarks. When government builds the roads, the private sector must construct compelling destinations and narratives along them.

Only when these three elements move in harmony can Korea’s tourism industry evolve from a government-mobilized model into a self-sustaining ecosystem of public–private collaboration.

This insight has diagnosed the structural crisis of inbound–outbound tourism imbalance facing Korea’s tourism industry and explored comprehensive solutions to overcome it. Our analysis confirms that Korean tourism remains trapped in a chronic deficit structure and a value perception gap. Through Japan’s case, we examined how attention to infrastructure and content detail can fundamentally redirect tourism flows. We further proposed concrete solutions, including generationally tailored strategies, the rediscovery of space, and public–private collaborative governance.

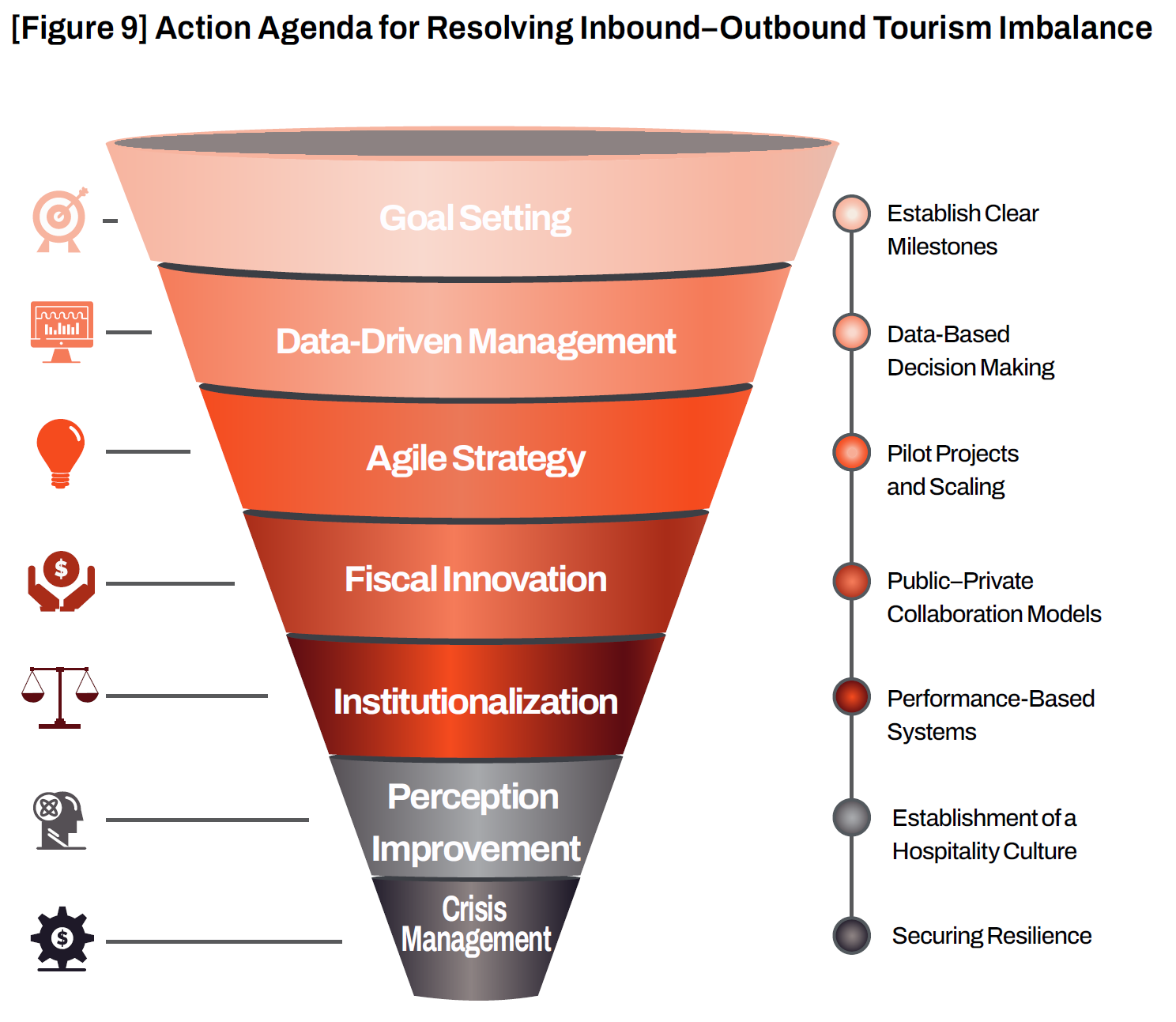

What remains now is execution. Even the most sophisticated strategy is futile if it remains a report on a desk. To transform the USD 10 billion tourism deficit into domestic economic vitality—and to turn crisis into opportunity—we propose seven core action tasks that government and the private sector must pursue together as one team.

1. [Goal Setting] Establishing a Mid- to Long-Term Roadmap

Vague aspirations are insufficient; goals must be numerically explicit and verifiable. Clear milestones—such as “30 million inbound visitors and a balanced tourism account by 2030”—are essential. However, policy should not focus solely on visitor volume. Qualitative indicators, including spending per visitor and repeat visitation rates, must be incorporated. In addition, internal strength indicators—such as the frequency of domestic travel by residents and the growth rate of regional tourism spending—should be defined as key performance indicators (KPIs) and managed as a national agenda.

2. [Data-Driven Management] Building Feedback Loops Based on Data, Not Intuition

Modern tourism is a data industry. Reliance on annual, retrospective statistics alone is inadequate in an era of rapidly shifting trends. Mobility data, card transaction data, and accommodation booking data must be integrated to track inbound and outbound flows in near real time. Policy decisions should be guided by a data feedback loop that diagnoses how policies function on the ground, where customer dissatisfaction emerges, and how immediate adjustments can be made. Policy must not be a fossil created once and forgotten—it must be a living organism that continuously evolves by feeding on data.

3. [Agile Strategy] Piloting Small, Scaling Fast

Not everything can be changed at once. To reduce risk and increase success probability, an agile approach is required. Selected regions should be designated as tourism innovation testbeds, where DMO models or themed travel discount weeks can be piloted first. Once small successes are validated, they should be standardized and rapidly scaled nationwide through a phased strategy. Proven success models naturally invite benchmarking by other local governments.

4. [Fiscal Innovation] Combining Seed Funding with Public–Private Partnerships (PPP)

Vision must be matched by financial resources. Government tourism budgets should play a catalytic role by funding initial infrastructure and system development. However, public finance alone is insufficient. Public–Private Partnership (PPP) models must be institutionalized, ensuring profitability and regulatory flexibility so that private capital can actively invest in regional resorts, theme parks, and regenerated spaces.

5. [Institutionalization] Establishing a Legal Foundation for Sustainability

For systems to take root, legal backing is essential. Enacting a tentative “Special Act on Regional Tourism Promotion” would codify the legal status and authority of privately led DMOs. At the same time, legal grounds must be established to allow local governments to impose meaningful sanctions on price gouging and unfair practices that undermine the tourism market. Such measures ensure consistency and enforceability in policy implementation.

6. [Perception Shift] Long-Term Investment in Kindness as Infrastructure

Ultimately, tourism is a people-centered industry. Cultivating service-mindedness among tourism workers is not a cost but the most reliable investment. Rather than one-off campaigns or slogans, systematic training and incentive systems are needed to embed a culture of hospitality. When travelers come to believe that “in Korea—especially in its regions—you are genuinely treated well,” those who once left will return.

7. [Crisis Management] Building Immunity Against External Shocks

External shocks—pandemics, diplomatic tensions, sharp exchange-rate fluctuations—will inevitably recur. Wisdom lies in preparing for downturns during boom times. Scenario-based response manuals should be developed in advance, and domestic demand should be strengthened as a stable anchor. Only then can the tourism ecosystem avoid collapse and maintain resilience during crises.

As we conclude this report, we seek to redefine the meaning of the USD 10 billion tourism balance deficit. This figure is not merely an accounting loss that needs to be filled. Rather, it represents a vast reservoir of demand—clear evidence that Korean consumers are ready and willing to spend on better travel experiences—and a territory of opportunity that Korea’s tourism industry must reclaim. What Korea needs now is not a heightened sense of crisis, but confidence and a strategic transformation capable of redirecting this powerful flow.

First, tourism is both an export industry and a breakwater against regional decline. Redirecting even 10% of outbound travel demand back into domestic travel would keep trillions of won circulating within the national economy. This capital would not concentrate in large corporations or duty-free shops; instead, it would flow into the parched capillaries of local economies. Where tourists gather, jobs are created, young people return, and communities regain vitality. In this sense, tourism promotion is one of the most immediate and effective policies for balanced regional development—and a crucial domestic buffer that strengthens the Korean economy against external shocks.

Second, Korea must compete not on patriotism, but on overwhelming attractiveness. The painful consumer critique—“people leave because there is nothing to see”—can no longer be ignored. Consumers are rational and discerning; the era of retaining demand through appeals to national sentiment is over. What is required is a fundamental overhaul of the tourism industry’s constitution—from supply to governance. As Japan demonstrated, Korea must arm itself with meticulous content and trustworthy services, capable of making even domestic travelers exclaim, “I didn’t know places like this existed in Korea.” Destinations that domestic travelers do not love will never appeal to foreign visitors. The success of intra-bound tourism is, ultimately, the foundation of inbound competitiveness.

Third, what is needed is the harmony of “One Team”—government, businesses, and local communities playing together. Resolving the inbound–outbound imbalance cannot be achieved by any single ministry or corporation. Government must dismantle regulatory barriers and set the stage; local governments and DMOs must infuse destinations with distinctive local identity; and companies must respond with innovative technologies and compelling content. Only when this triangular alliance operates in concert can Korea shed the stigma of price gouging and content scarcity.

In conclusion, the USD 10 billion deficit is a critical golden-time signal. If Korea breaks the “leaking bucket” now and replaces it with a wellspring of attractiveness and trust, then five or ten years from today, the nation can stand tall as a genuine tourism destination defined by culture and restorative experiences.

Recreating Korea as a country that is a must-visit bucket-list destination for foreigners—and a place of rediscovery and pride for its own citizens—is not merely a tourism agenda. It is the installation of a new growth engine for the economy and the most reliable path toward enriching the cultural quality of everyday life. Now is the time to act together to restore a healthy and sustainable tourism ecosystem.