Suckwon Hong / Principal Researcher, Yanolja Research / [email protected]

Deachul (David) Seo / Senior Researcher, Yanolja Research / [email protected]

SooCheong Jang / Professor, Purdue University & Director, Yanolja Research / [email protected]

Kyuwan Choi / Professor, Kyung Hee University & Director, H&T Analytics Center / [email protected]

The global tourism industry in 2026 has moved beyond simple "recovery" into a phase of structural transformation. Macroeconomic factors—high interest rates, exchange rate volatility, frequent climate-related disasters, shifts in U.S. policy under the Trump administration, and geopolitical tensions—have become the key constants determining demand. We have entered an era of "hyper-uncertainty" where intuition alone is insufficient.

In this environment, sophisticated tourism demand forecasting transcends mere statistical estimation. At the national level, it serves as a compass for the allocation of public resources, including the expansion of airport and port infrastructure, immigration policies, tourism security, and guidance systems. In the private sector, it is a measure of survival that dictates flight route operations, hotel revenue management, and the marketing strategies of distribution and platform companies. In the South Korean tourism market, which is highly dependent on external factors and sensitive to surrounding circumstances, data-driven future forecasting has become a "mandatory requirement" rather than an option.

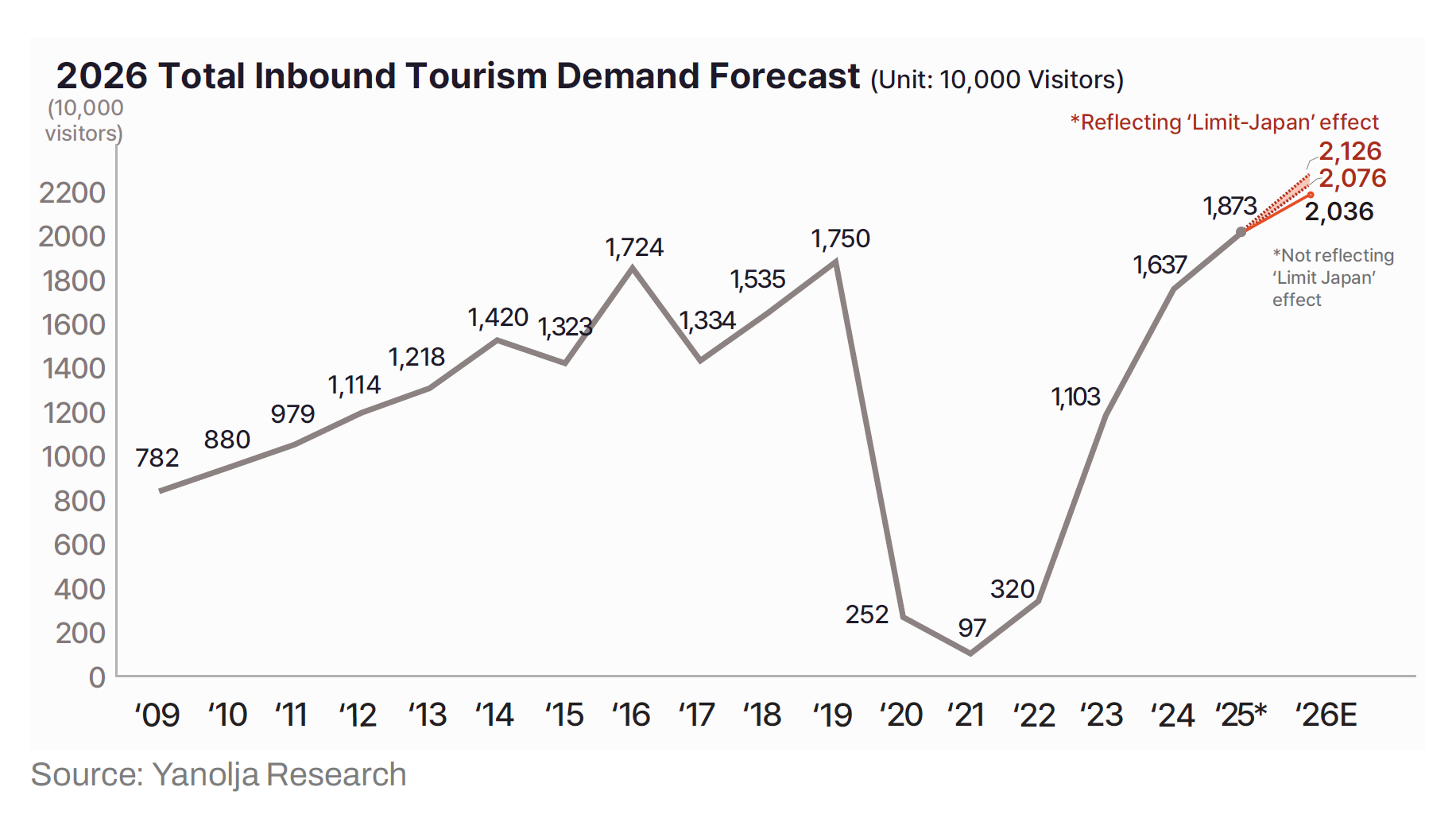

Yanolja Research has been taking a multi-dimensional view of the Korean tourism market by integrating macroeconomic indicators, aviation supply, and digital demand signals with the latest AI technology to meet these demands. Its accuracy has already been proven numerically. In the "South Korea's 2025 Inbound Tourism Demand Forecast (Yanolja Research Brief Vol. 3)" published last year, inbound demand for 2025 was projected at approximately 18.73 million. As of December 23, 2025, the cumulative number of foreign tourists reached 18.50 million, confirming that our prediction was very close to the actual performance. Factoring in year-end arrivals, the final result is expected to align very closely with our projection.

Behind this high level of accuracy is Yanolja Research’s proprietary deep-learning-based demand forecasting model. Rather than simply extending historical trend lines, the model is designed to learn from a broad set of signals: macro indicators such as GDP and exchange rates; aviation supply data; digital leading indicators such as search volume for Korea-travel keywords; and even sudden external shocks. In other words, it generates forecasts by integrating diverse signals into a single predictive framework.

Building on this verified model, this Insight provides detailed forecasts to outlook the massive movement of over 50 million people annually, created by the intersection of "over 20 million inbound" and "30 million outbound" tourists in 2026. We aim to identify industry opportunities and threats embedded in these dynamics, and to provide clear reference points so that government and businesses can design strategies based not on “gut feel” or “simple experience,” but on data—especially in an era dominated by uncertainty.

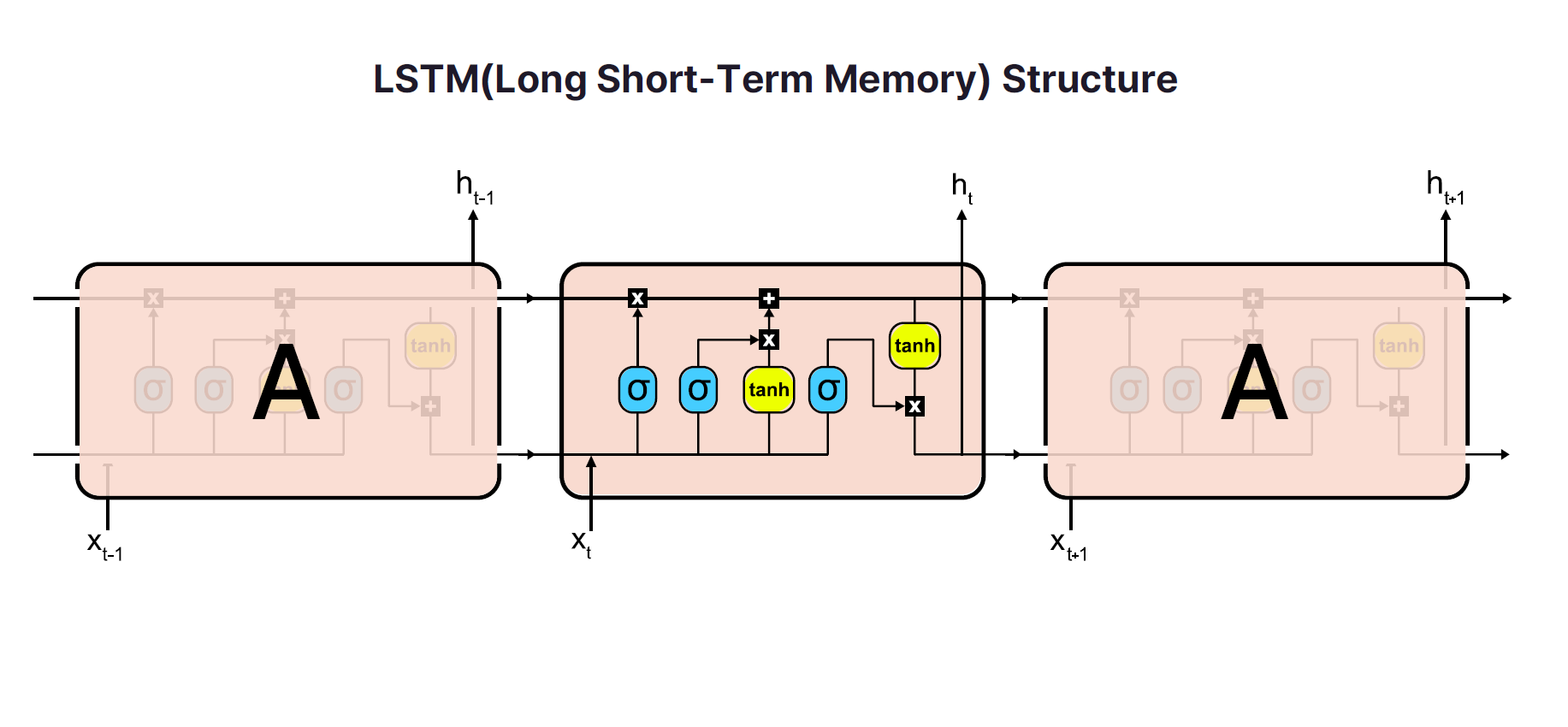

Traditional tourism demand forecasting has primarily relied on regression analysis or time-series statistical models such as ARIMA (Autoregressive Integrated Moving Average). While these models are useful for identifying linear trends in data, they reveal limitations in today’s environment characterized by frequent multi-variable and non-linear shocks. To overcome these limitations and secure both accuracy and explanatory power, Yanolja Research adopted the latest deep learning models.

The backbone of this forecast is the LSTM (Long Short-Term Memory) model. LSTM is a type of Recurrent Neural Network (RNN) specialized in learning long-term patterns in time-series data by solving the "long-term dependency" problem of standard RNNs. Whereas a typical RNN tends to lose information as sequences become longer, LSTM improves accuracy by retaining important information over long horizons and discarding irrelevant signals.

Tourism data exhibits strong seasonality while also reacting sharply to sudden external events. For instance, short-term patterns such as recurring holiday peaks coexist with long-term shifts such as changing destination preferences over multiple years. The LSTM model learns these complex time-series structures to capture non-linear dynamics hidden in patterns rather than simply repeating the past.

Forecast performance depends heavily on the quality and diversity of the input data. Yanolja Research’s model does not rely solely on historical arrival counts. It integrates a comprehensive set of macro and micro variables that influence tourism demand, including:

Before discussing the future, it is essential to validate how accurate past forecasts were. As mentioned, Yanolja Research projected that approximately 18.73 million foreign visitors would enter Korea in 2025. According to provisional counts from the Ministry of Culture, Sports and Tourism and the Korea Tourism Organization, cumulative inbound arrivals reached about 18.50 million as of December 23, 2025. With the final week of December—traditionally peak period due to Christmas and New Year—still to be tallied, the result is expected to be nearly identical to the 18.73 million projection. Having delivered accurate predictions amidst global economic slowdown concerns and exchange rate instability in 2025, our model serves as a reliable compass for 2026.

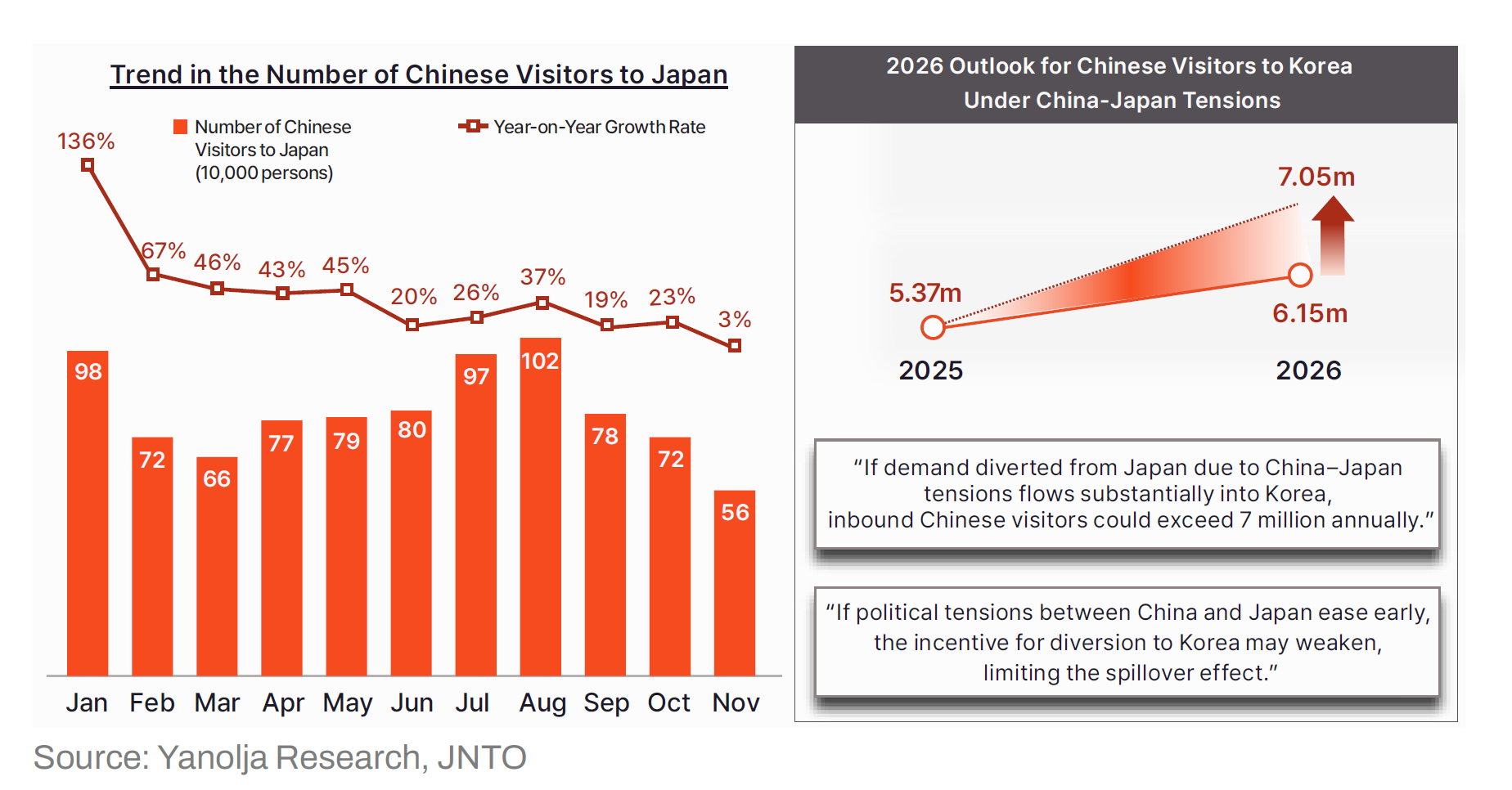

Based on analysis using this validated model, inbound arrivals to Korea in 2026 are projected to reach 20.76 million to as high as 21.26 million. This is not merely a trend projection; it also incorporates, in advance, a key variable in Northeast Asian geopolitics: intensified China–Japan tensions and the resulting de facto “Limit-Japan” (限日令; Han-il-ryeong) effect.

Under the base model, the forecast was approximately 20.36 million. However, scenario analysis that reflects external geopolitical shifts indicates stronger upside potential. If worsening bilateral tensions—deepening since last November—lead Chinese tourists who had planned to visit Japan to switch their destination to Korea, a “spillover benefit” could materialize and push the overall market beyond the baseline. In that case, 2026 would not only mark the opening of the “20-million inbound era,” but could become a landmark year in which Korea records the largest inbound volume in its history.

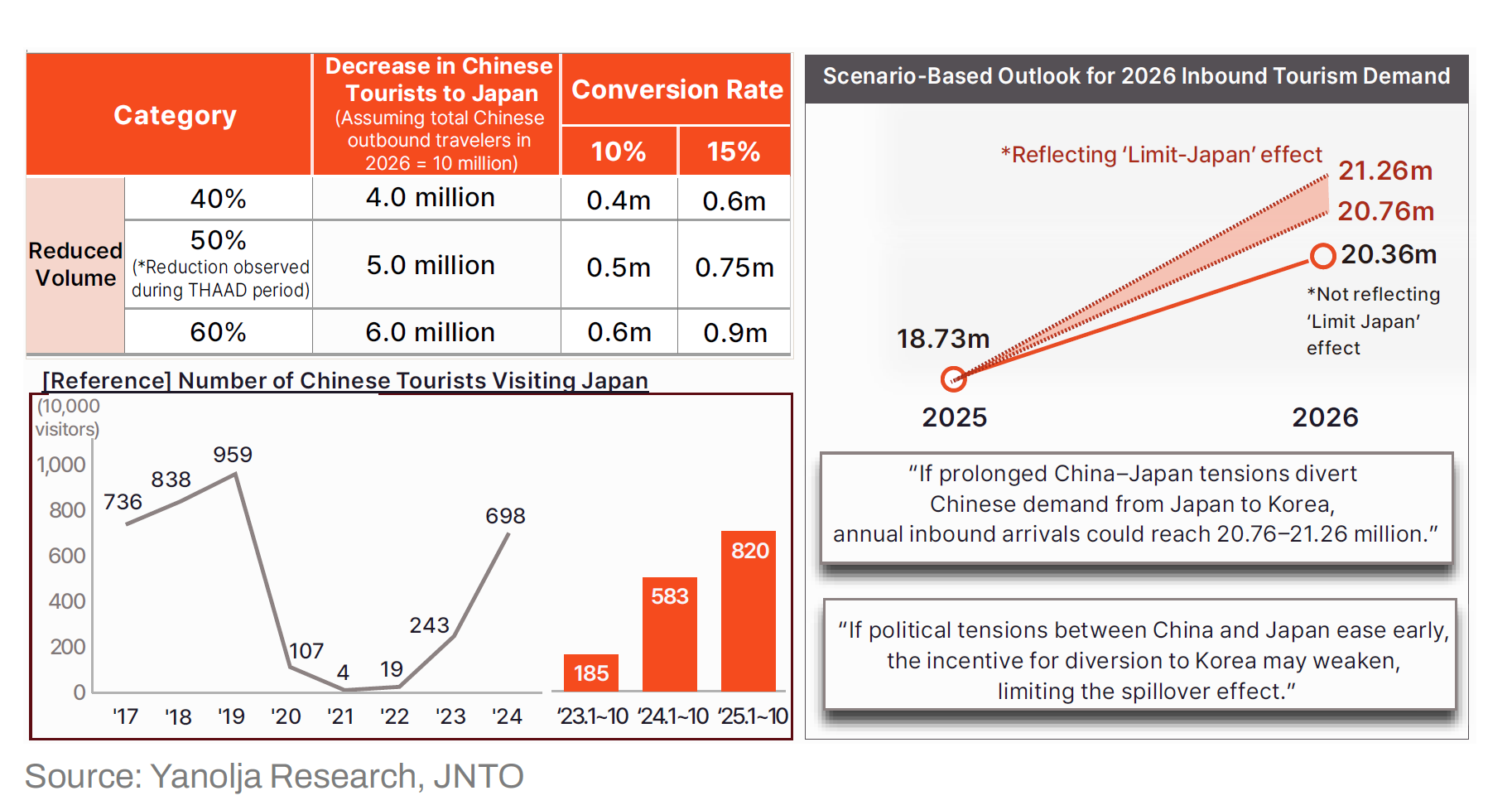

To estimate the scale of additional demand the China-Japan conflict might bring to the 2026 Korean inbound market, we used data from the 2017 "Limit Korea" (triggered by the THAAD deployment) as a benchmark. This is a clear empirical case of how travel demand shifts to neighboring countries when political/diplomatic conflicts suppress demand for a specific nation.

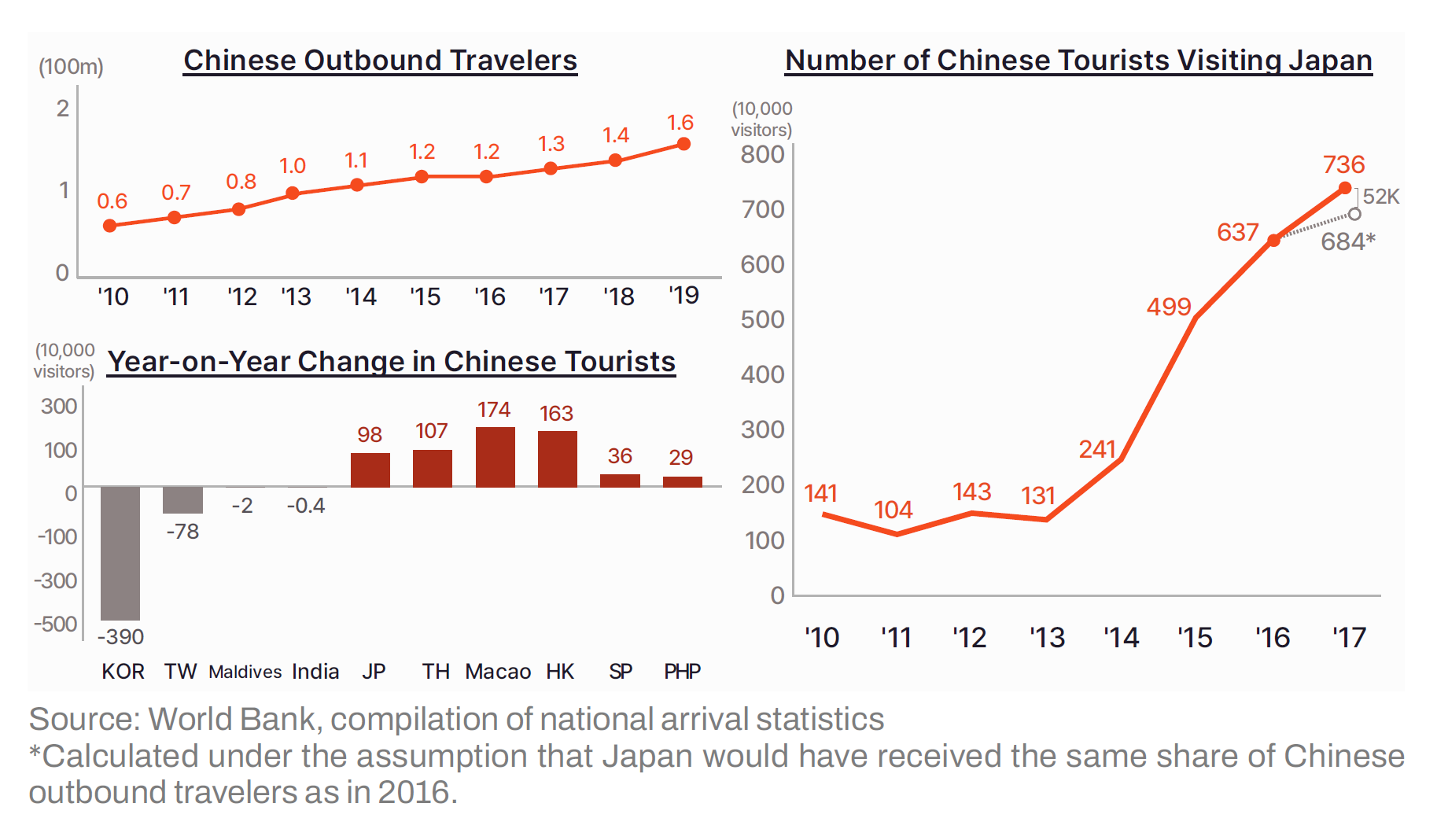

Past Experience: Demand shifts, it doesn't vanish. In 2017, the number of Chinese visitors to Korea fell by approximately 3.9 million (-48%) year-on-year due to China’s restrictions on travel to Korea. Importantly, overall outbound travel demand from China did not collapse during the same period. When the path to Korea was blocked, demand reallocated toward geographically close “substitute destinations” that could provide similar cultural satisfaction. Japan, for example, received an additional about 0.98 million Chinese visitors, and Thailand received about 1.07 million, reflecting a clear “balloon effect.”

Calculating the Conversion Rate. We introduced a "conversion rate" to measure this balloon effect—the percentage of displaced demand for Korea absorbed by Japan. We separated the “excess inflow” above Japan’s expected trend (about 0.52 million) from total Chinese arrivals to Japan in 2017 (7.36 million), and compared it with Korea’s decline (3.9 million). This yielded an estimated conversion rate of approximately 10.9% to 13.1%—i.e., roughly that share of diverted Korea-bound demand shifted to Japan.

Using these empirical parameters, we conducted scenario analysis for current China–Japan tensions as follows:

Under this framework, an estimated 0.4 to 0.9 million Chinese tourists could shift from Japan to Korea. As a result, if spillover benefits materialize, Korea’s total inbound demand in 2026 would be revised upward from the baseline 20.36 million to a range of 20.76 million to as high as 21.26 million.

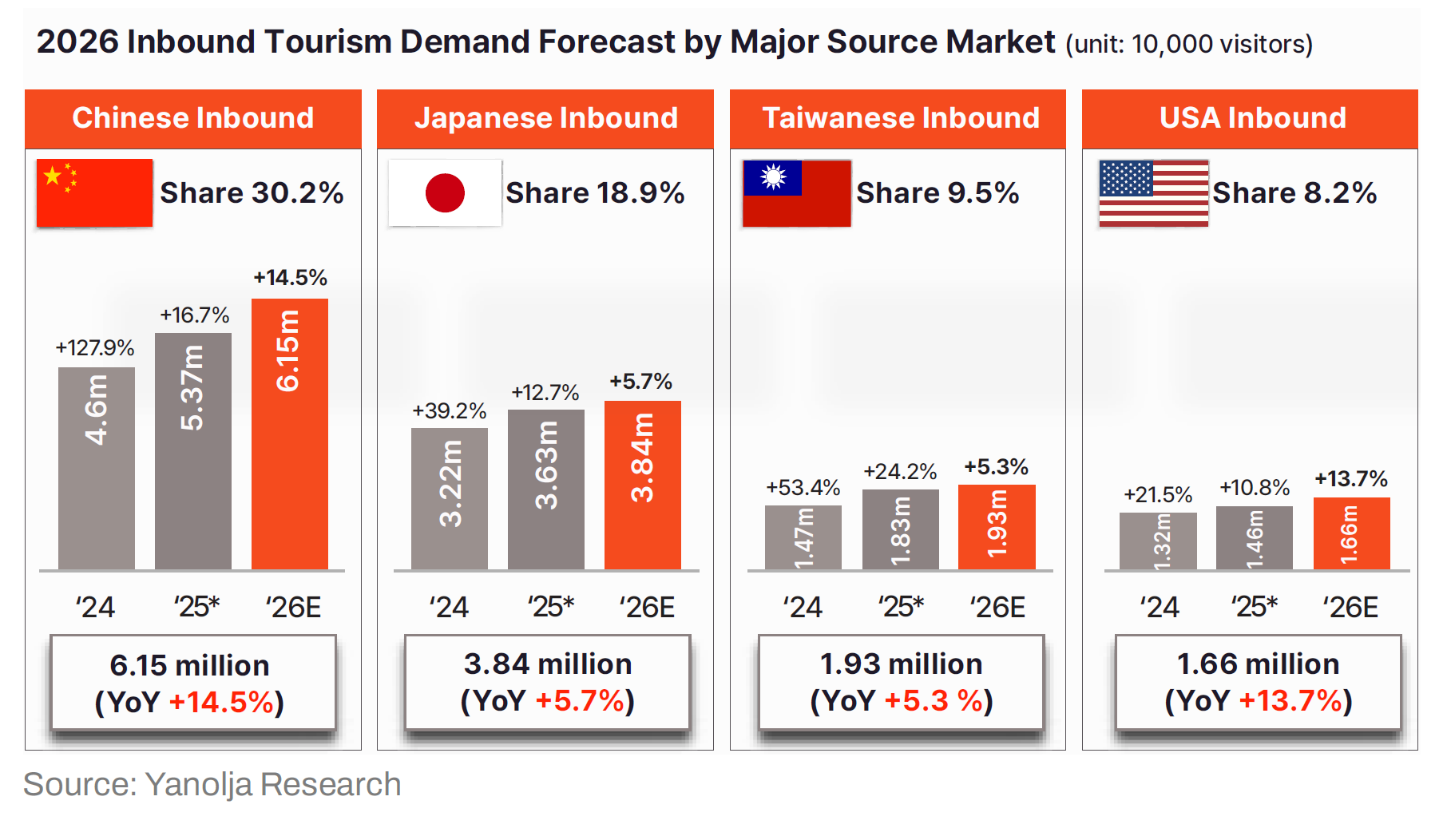

Korea’s inbound market in 2026 is projected to be strongly driven by four core markets—China, Japan, Taiwan, and the United States—which together are expected to account for 66.8% of total arrivals. This suggests that even amid global tourism uncertainty, Korea’s demand base remains resilient around these “Big 4” markets.

By market, China is expected to solidify its position as the largest source market at 6.15 million (with upside to higher levels under the scenario), followed by Japan (3.84 million), Taiwan (1.93 million), and the United States (1.66 million). While these four markets differ in economic context and travel motivations, collectively they are expected to serve as the primary pillars supporting Korea’s quantitative inbound growth in 2026.

Among the Big 4, China is the key battleground where the most dynamic and dramatic growth is anticipated. The base forecast from our model is approximately 6.15 million, implying a full recovery to the pre-pandemic level. What is especially notable, however, is the upside potential: if spillover benefits from China–Japan tensions materialize, arrivals could expand sharply—up to 7.05 million. This outlook is driven by three dimensions:

Firstly, removal of policy barriers. The visa-free entry policy for Chinese group tours, implemented from the second half of 2025, acted as a decisive catalyst by unlocking suppressed package-tour demand at scale. This is a powerful structural driver that restores liquidity to the group segment, not only to FITs (independent travelers). At the same time, normalization of Korea–China air routes and the recovery of cruise calls—key channels for mass travel—have strengthened the physical foundation for demand expansion.

Secondly, geopolitical spillover effect. Rising anti-Japan sentiment within China is likely to reposition Korea as a “psychologically safer and more comfortable” destination. As Korea’s attractiveness as a nearby country free of political burden rises, substitution away from Japan toward Korea may become more pronounced.

Thirdly, value-for-money demand. While China’s domestic slowdown and weakening consumer sentiment could appear negative for outbound travel overall, they can become an opportunity for Korea. Instead of long-haul trips to the Americas or Europe, travelers may prefer nearby destinations that offer high satisfaction at a reasonable cost—making Korea an appealing alternative.

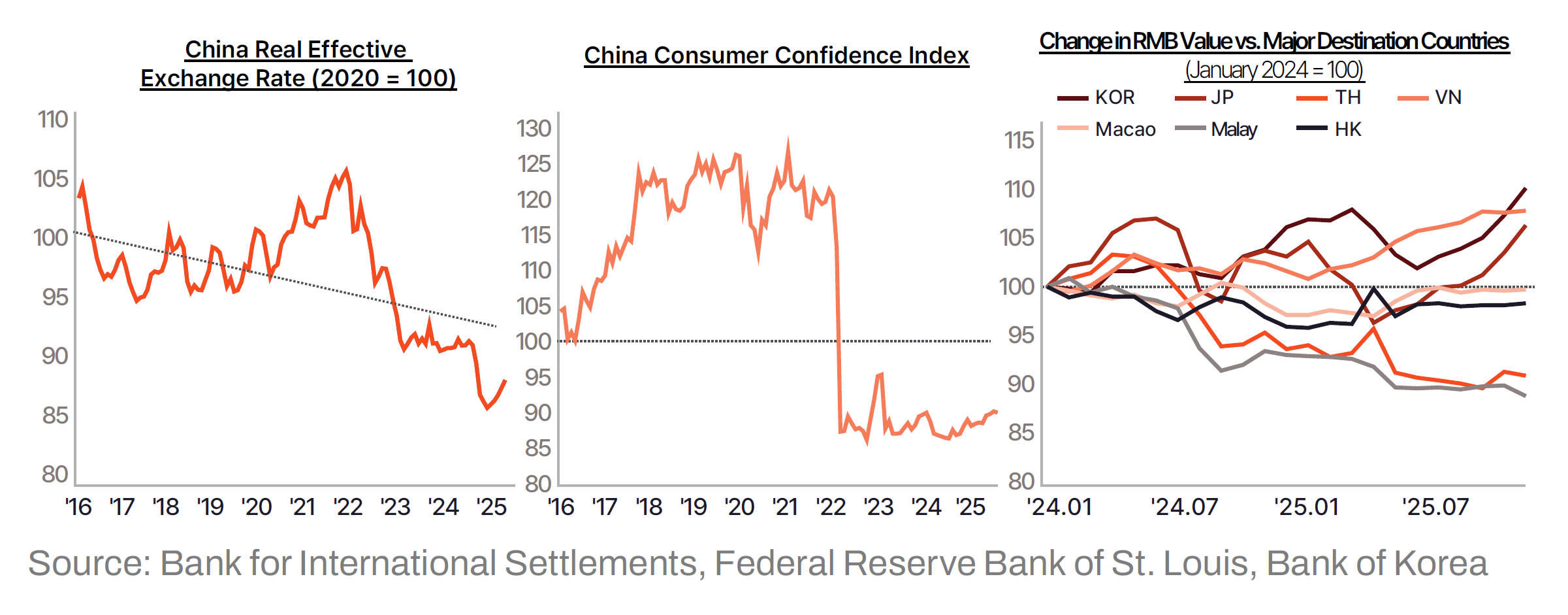

That said, China’s domestic slowdown and RMB weakness remain meaningful downside risks: weaker income prospects can reduce willingness to travel abroad. However, when viewed through the lens of relative exchange-rate purchasing power, the picture is not uniformly pessimistic. While the RMB has weakened, the KRW has also been trending weak, keeping the RMB’s purchasing power relative to the KRW (real effective purchasing terms) comparatively stable. If this environment continues into 2026, Korea’s “price competitiveness” could partially offset economic headwinds and serve as a buffer that helps defend demand.

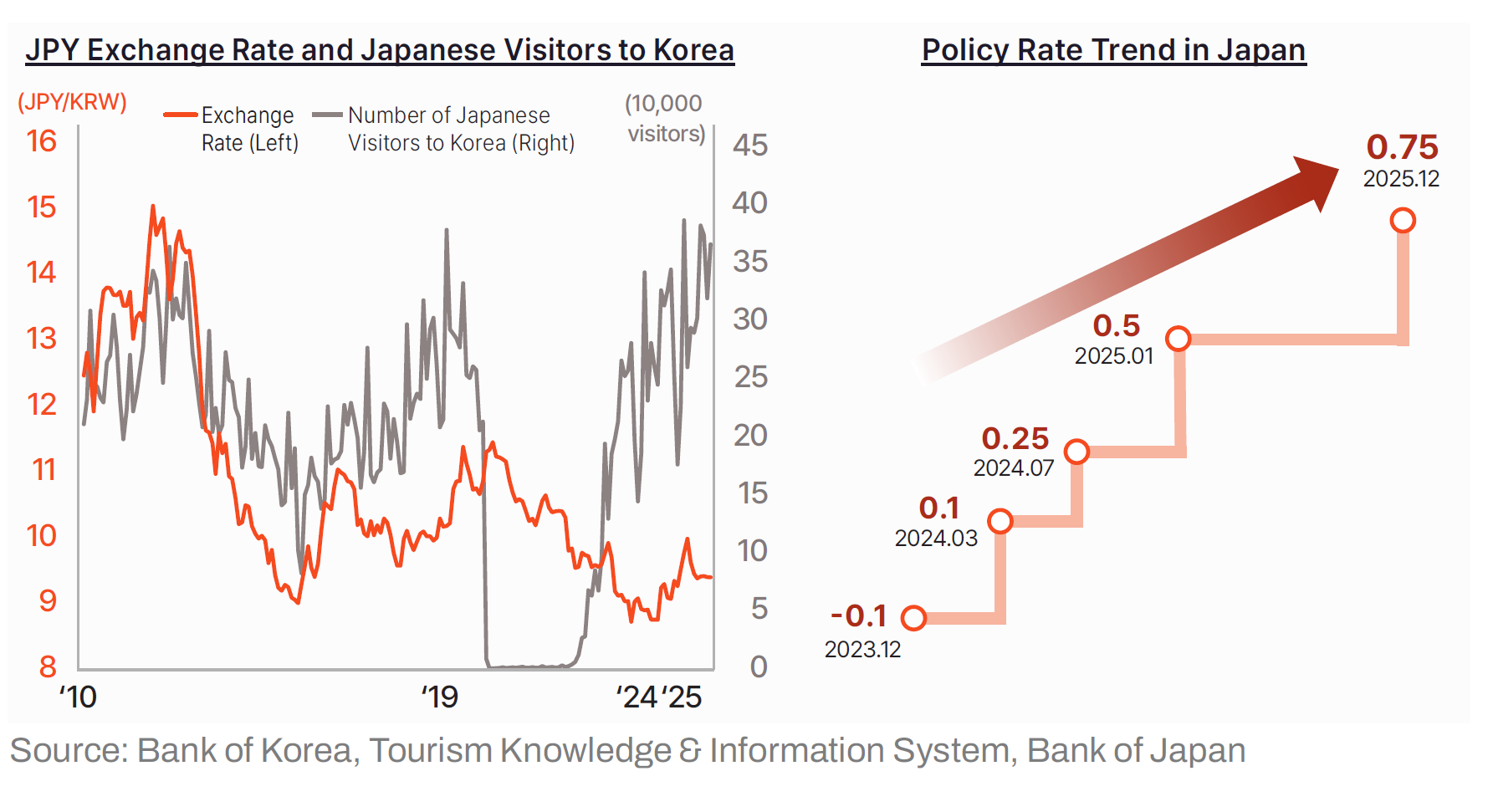

Japanese inbound arrivals to Korea in 2026 are projected to reach approximately 3.84 million, up 5.7% year-on-year. This is not only 17.4% higher than the 2019 level (3.27 million), but also exceeds Japan inbound’s previous peak in 2012 (3.52 million), setting a new all-time record after 14 years. This record growth is expected to come from the interaction of two forces: robust supply networks and improving macroeconomic conditions.

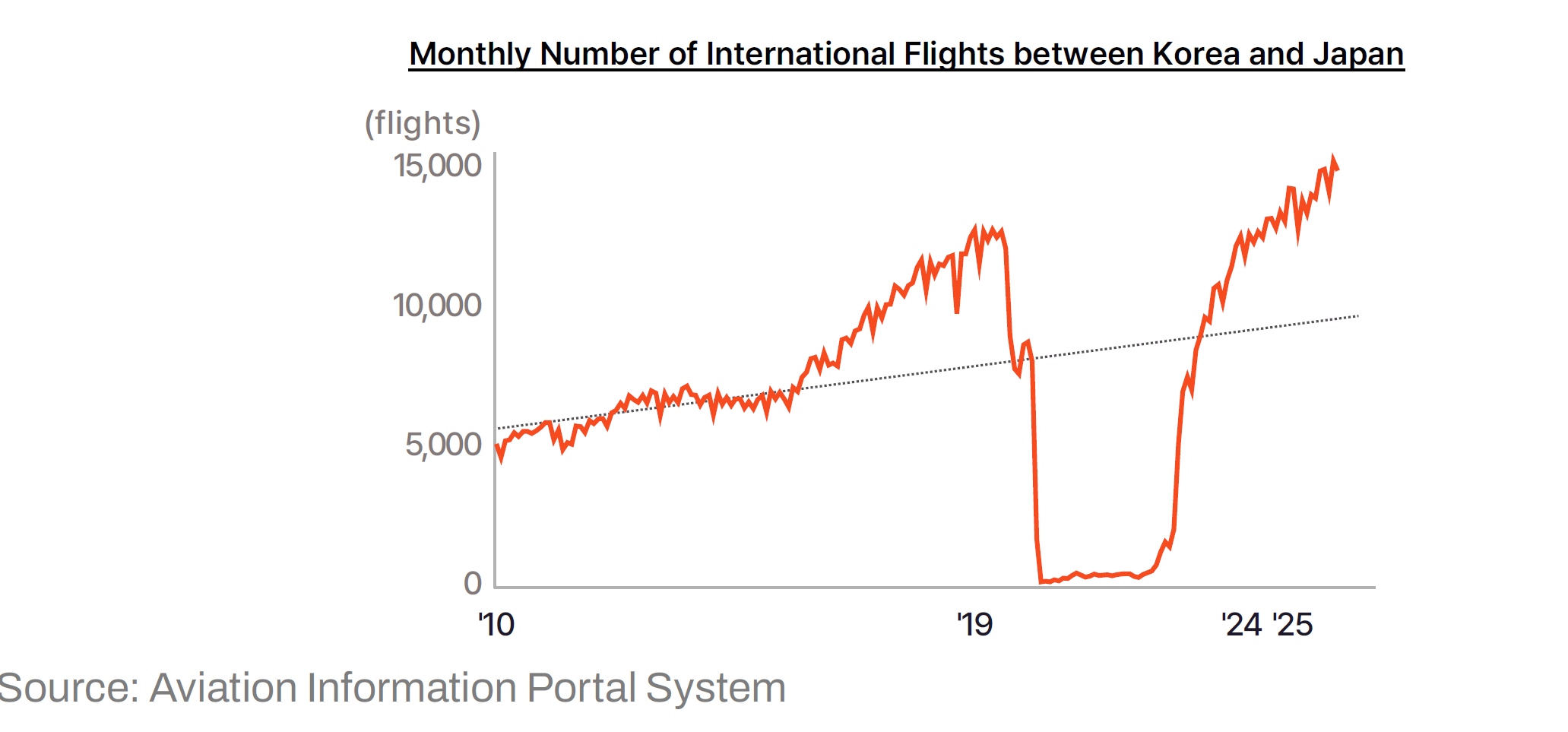

Firstly, dense aviation supply physically enables demand expansion. Since the pandemic, the Korea–Japan network has recovered on a steady upward trajectory, reaching an overwhelming supply capacity of roughly 12,000 flights per month in 2025. Beyond the traditional focus on major cities such as Tokyo and Osaka, the restoration and launch of direct routes connecting regional Japanese cities to Korea has improved accessibility and allowed the market to capture latent demand originating outside Japan’s largest urban centers.

Secondly, macro shifts—especially Japan’s monetary policy turn—should revive purchasing power. Japan’s historically weak yen has weighed on outbound travel sentiment, but Korea’s market defended demand thanks to the KRW’s parallel weakness maintaining relative price competitiveness.

In 2026, however, a more tangible purchasing-power boost is expected. After lifting its policy rate from -0.1% to positive territory (0.1%) in March 2024, the Bank of Japan continued gradual hikes, reaching 0.75% by December 2025. Over time, this tightening bias can support yen appreciation, translating into stronger external purchasing power for Japanese travelers. In effect, “easy to go” conditions (air connectivity) combine with “more valuable spending power” (exchange rates), creating strong momentum supporting rising inbound demand to Korea.

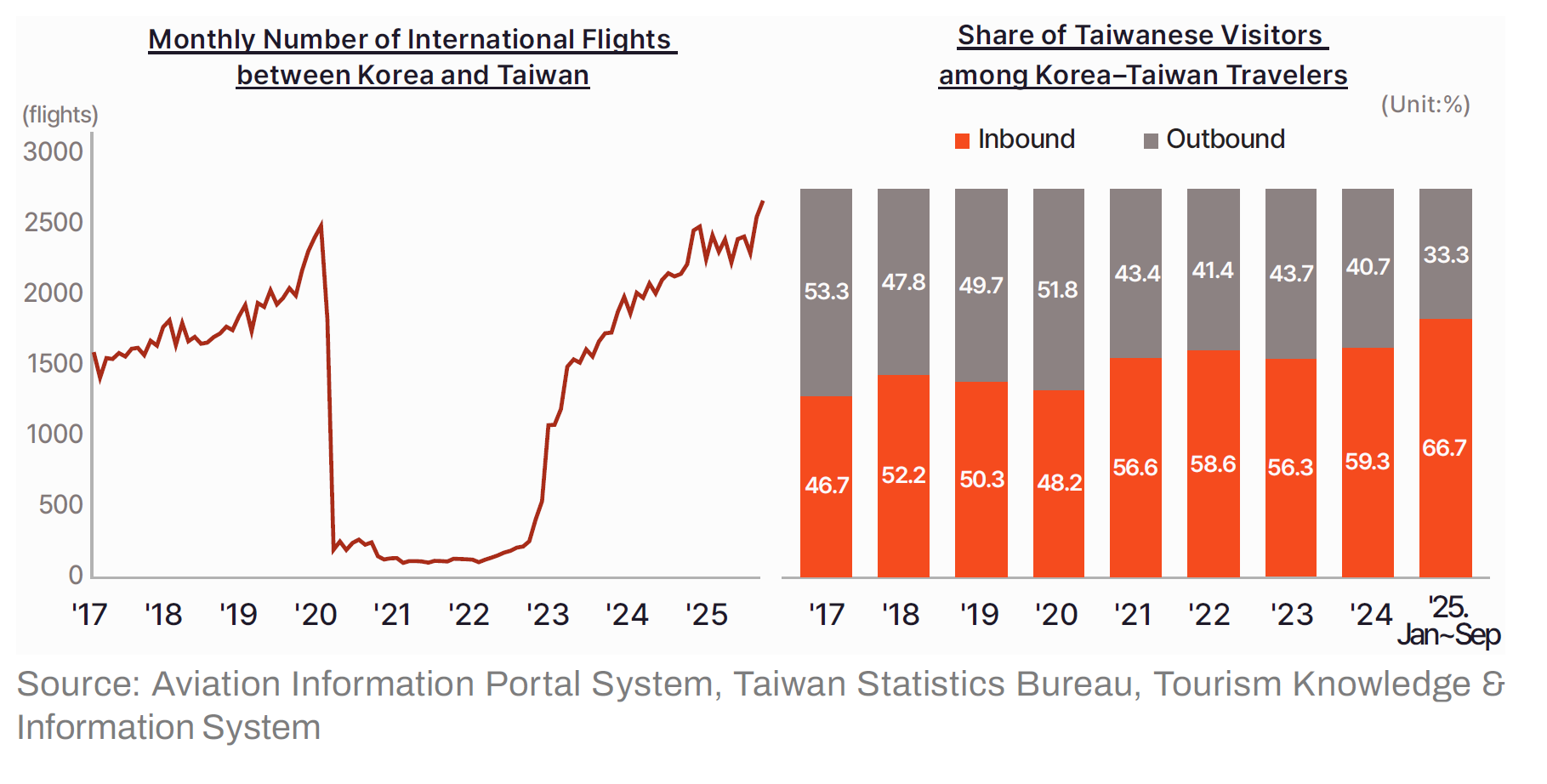

Taiwanese inbound arrivals to Korea in 2026 are expected to reach approximately 1.93 million, up 5.3% year-on-year. This continues the steep rebound since 2023 (0.96 million) immediately after the pandemic, and represents more than 1.5x the 2019 level (1.26 million). Taiwan is therefore expected to move beyond being merely a major market, becoming a core axis of Korea’s inbound growth. This expansion reflects structural and economic drivers:

Firstly, the structural rebalancing in Korea–Taiwan travel exchange. Before the pandemic (2017–2019), Taiwanese inbound to Korea accounted for about 46–50% of total bilateral exchange, balancing Korean outbound to Taiwan. Post-endemic, this balance flipped decisively toward inbound dominance. The share of Taiwanese visitors within total exchange rose from 56.3% in 2023 to 66.7% in 2025 (Jan–Sep).

A key driver is the normalization of K-culture’s influence in Taiwan. Favorability toward Korean culture—expanding beyond K-pop and dramas to food, beauty, and fashion—strongly stimulates latent travel desire, positioning Korea not just as a destination but as the “source of culture to be experienced firsthand.” This culturally driven structural shift improves aviation supply efficiency: strong underlying demand means additional flights translate directly into arrivals without persistent empty seats, reinforcing a virtuous cycle. As a result, in 2026 as well, expanding aviation supply is likely to remain the most reliable guarantee of continued market growth.

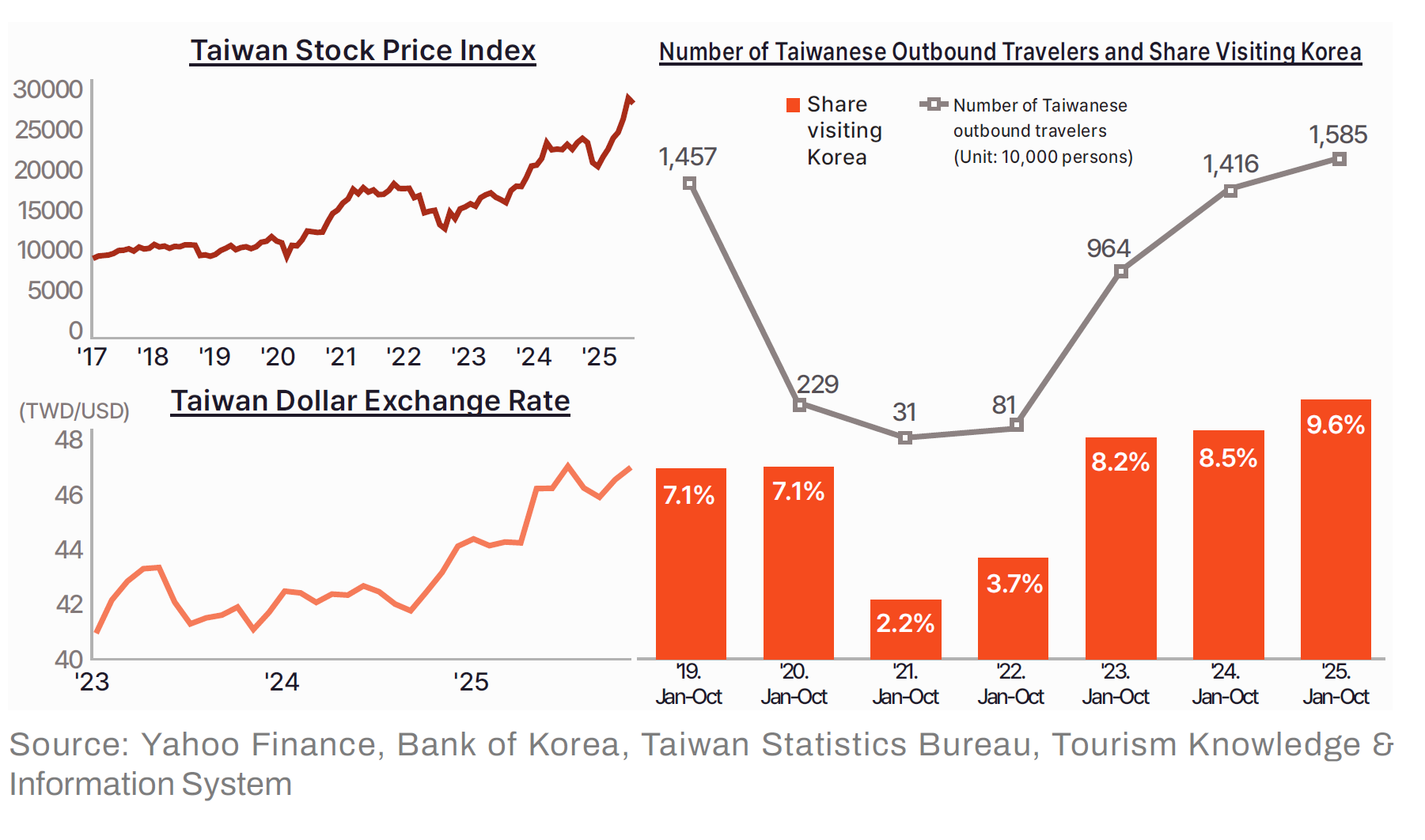

Secondly, purchasing-power expansion via a wealth effect. The global boom in semiconductors—Taiwan’s core industry—has supported a steady rise in the Taiwan Weighted Index. Rising asset values stimulate household spending sentiment and meaningfully expand capacity for overseas travel spending. Combined with a stable TWD–KRW exchange-rate trend, Korea remains attractive to high-purchasing-power Taiwanese travelers.

There are downside risks: external policy uncertainty, including US-led supply-chain realignment and pressure for localized semiconductor production, could raise Taiwan’s economic volatility. However, Korea’s share among Taiwan’s outbound travelers increased from 7.1% in 2019 to 9.6% in 2025, reaching an all-time high preference level. This suggests the likelihood of an abrupt contraction is low. Overall, despite external variables, Taiwan is expected to remain a solid pillar supporting both the quantity and quality of Korea’s inbound growth in 2026.

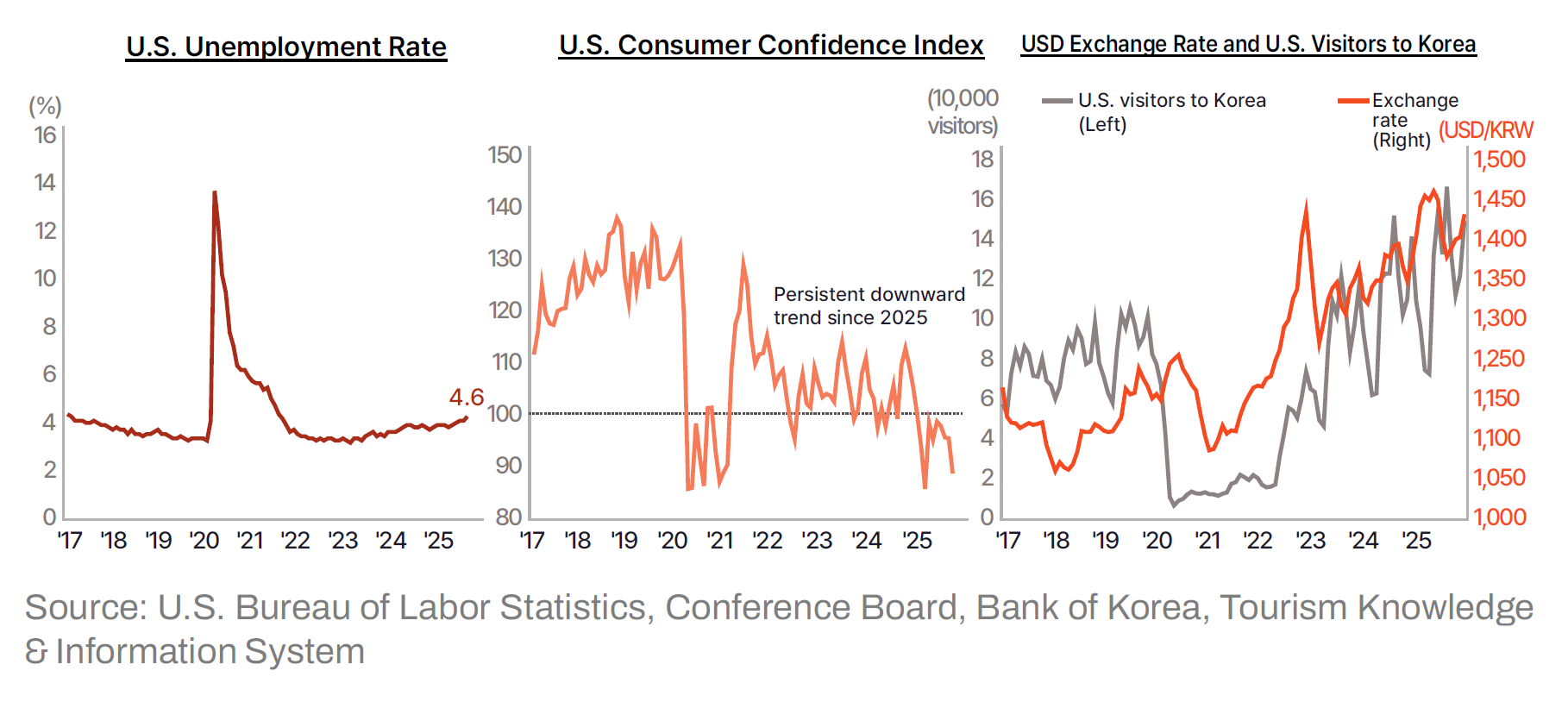

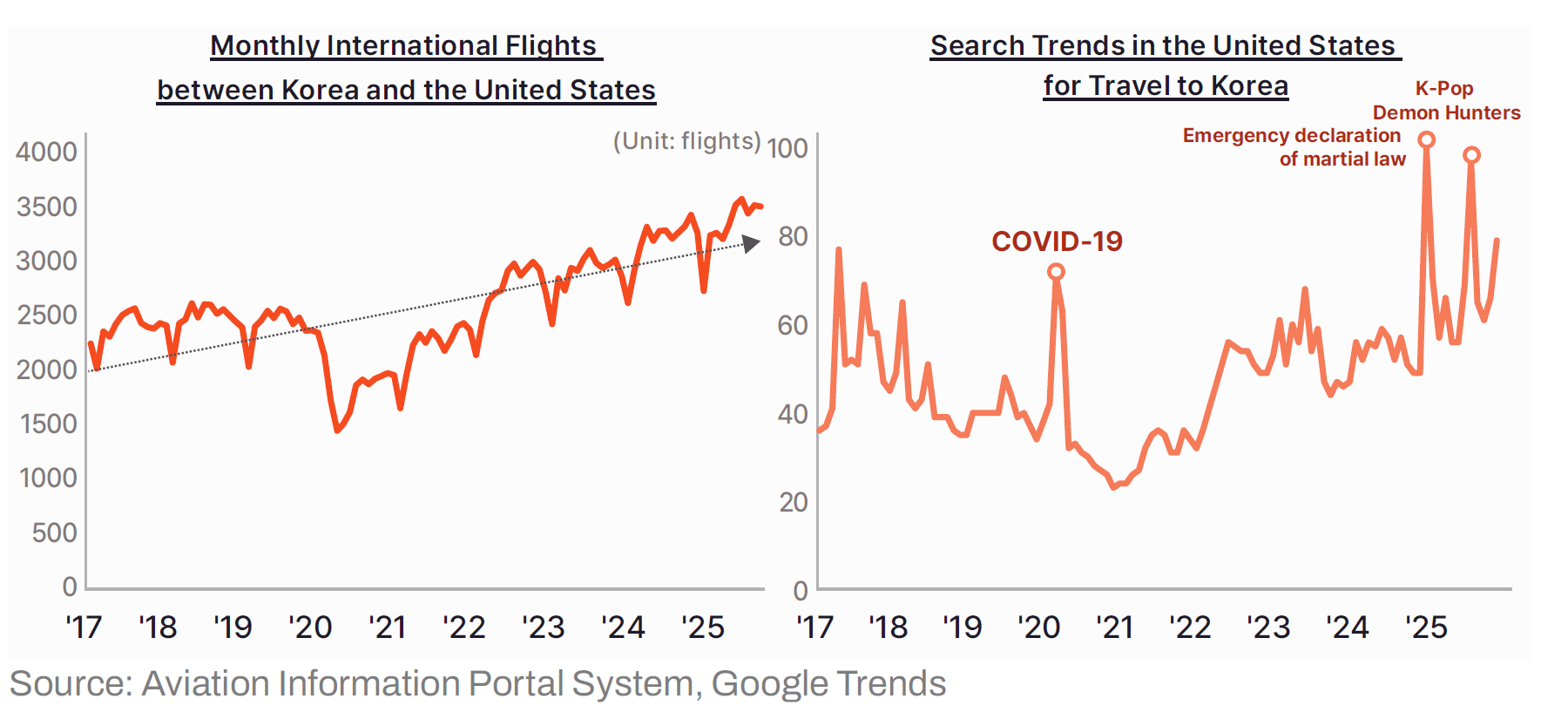

US inbound arrivals to Korea in 2026 are forecast at approximately 1.66 million, up 13.7% year-on-year. This represents nearly 60% growth versus the pre-pandemic 2019 level (1.04 million), making the US one of the strongest rebound performers among major source markets and likely setting a new all-time high. This surge appears to reflect structural growth driven by the combination of economic incentives and cultural expansion.

Firstly, the “strong dollar” effect overwhelms recessionary headwinds. Recent US macro indicators have shown instability: unemployment, which had held in the 3% range, rose from the second half of 2024 to 4.6% in November 2025, while consumer confidence declined—both signaling recession risk. Normally, income uncertainty suppresses outbound travel demand. In Korea’s case, however, KRW weakness against the USD provides US travelers with a tangible purchasing-power boost, offsetting consumption retrenchment and strengthening travel motivation.

Secondly, K-content-driven interest is converting into real demand. Google Trends indicates that US searches for “travel to Korea” have maintained an upward trajectory since the pandemic. The pattern of search spikes coinciding with K-content moments suggests curiosity is translating into concrete information-seeking behavior—an early step toward actual travel.

Thirdly, such growing interest is reflected in a structurally rising market share. As total US outbound travel gradually increases, the share choosing Korea rose steadily from 0.98% in 2017 to 1.3% in 2025, suggesting Korea is moving beyond an Asian niche market toward a mainstream destination. Meanwhile, aviation supply already exceeds 2019 levels, providing a solid physical foundation to absorb and sustain this growth.

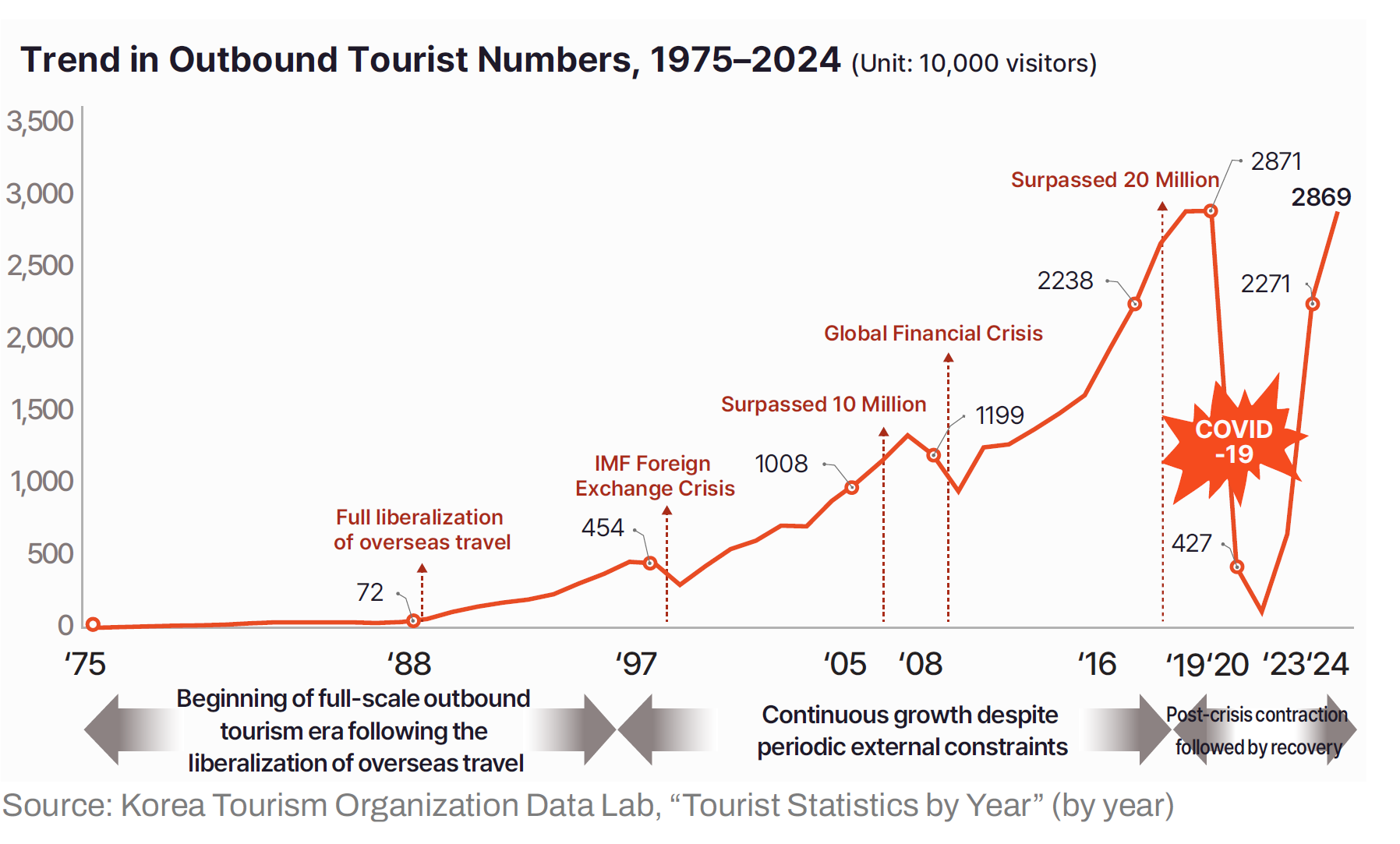

Korea’s outbound tourism market has followed a long-term growth curve since the 1989 full liberalization of overseas travel. After opening the 20-million annual departures era in 2016, the market demonstrated strong resilience even through the unprecedented shock of the COVID-19 pandemic.

The year 2025 is assessed as the peak of the recovery phase. Combining January–November performance (26.80 million) with seasonal year-end demand, total outbound departures in 2025 are estimated at approximately 29.47 million[1]. This exceeds the 2025 inbound forecast (18.73 million, Yanolja Research estimate) by more than 10 million, highlighting the outbound market’s overwhelming weight within Korea’s tourism industry structure.

Yanolja Research expanded the deep-learning-based analytical system validated in inbound forecasting to the outbound market outlook. Outbound demand is sensitive to a complex set of factors including exchange rates, income levels, aviation route supply, and destination safety/security. Accordingly, the model was designed to integrate multidimensional exogenous variables—not only historical demand flows but also domestic and global macro indicators, online search trends, and policy/diplomatic events.

As with inbound forecasting, we adopted LSTM (Long Short-Term Memory) as the core technique, given its strength in simultaneously learning long-term trends and short-term shocks in time-series data. This helps address the structural limitations of simple trend extrapolation and allows precise modeling of the non-linear recovery patterns observed after the pandemic. In addition, we used Random Forest as a supplementary method to quantitatively test the influence of major variables, enhancing not only predictive performance but also interpretability.

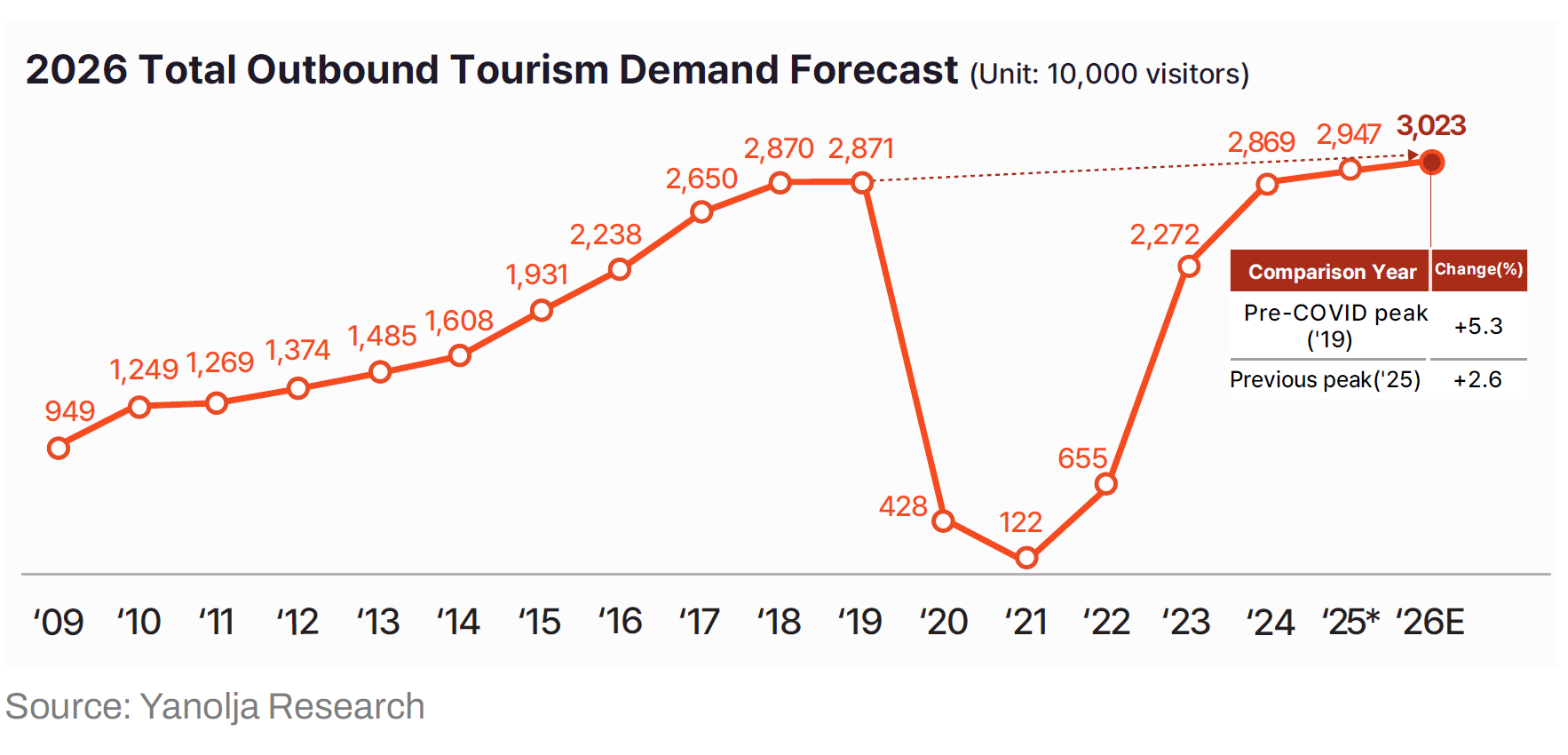

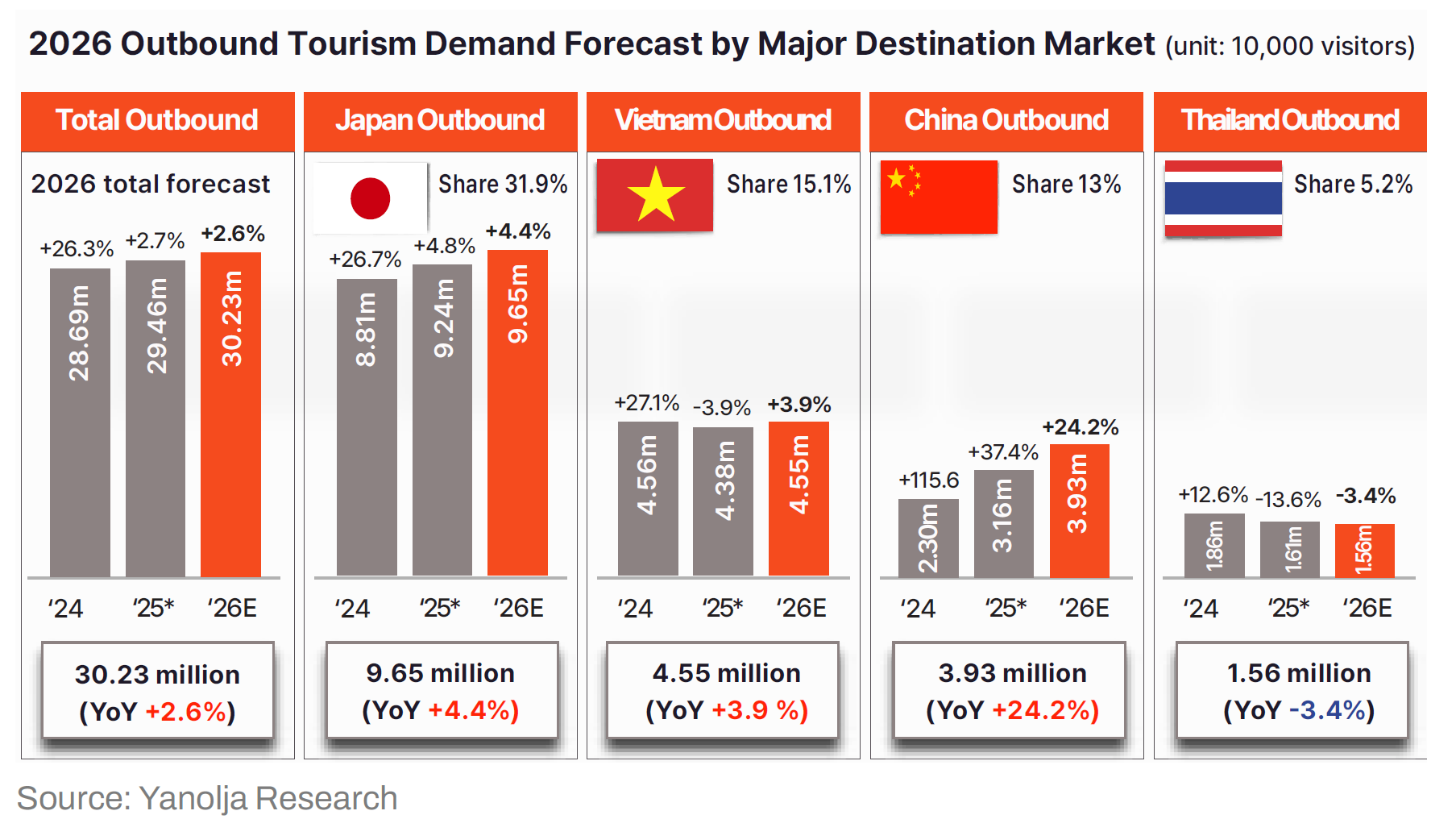

Based on this forecasting framework, the number of Korean outbound travelers in 2026 is projected at approximately 30.23 million, an increase of about 2.6% versus 2025. While the explosive rebound immediately after the pandemic is expected to moderate, the annual total is still likely to set a new all-time high.

A key point is the market’s internal qualitative shift. Separate from total outbound growth, demand by destination is expected to show decoupling—diverging patterns—because external variables evolve differently across countries (exchange rates, visa policy, inflation, safety/security conditions). As a result, even if the overall market grows, destination-level dispersion and volatility may increase.

A defining feature of the 2026 outbound market is continued concentration in nearby Asian destinations. Japan, Vietnam, China, and Thailand—the top four—are projected to account for about 65.2% of total outbound demand, maintaining strong market dominance.

Forecasts differ markedly by country in both growth and volatility:

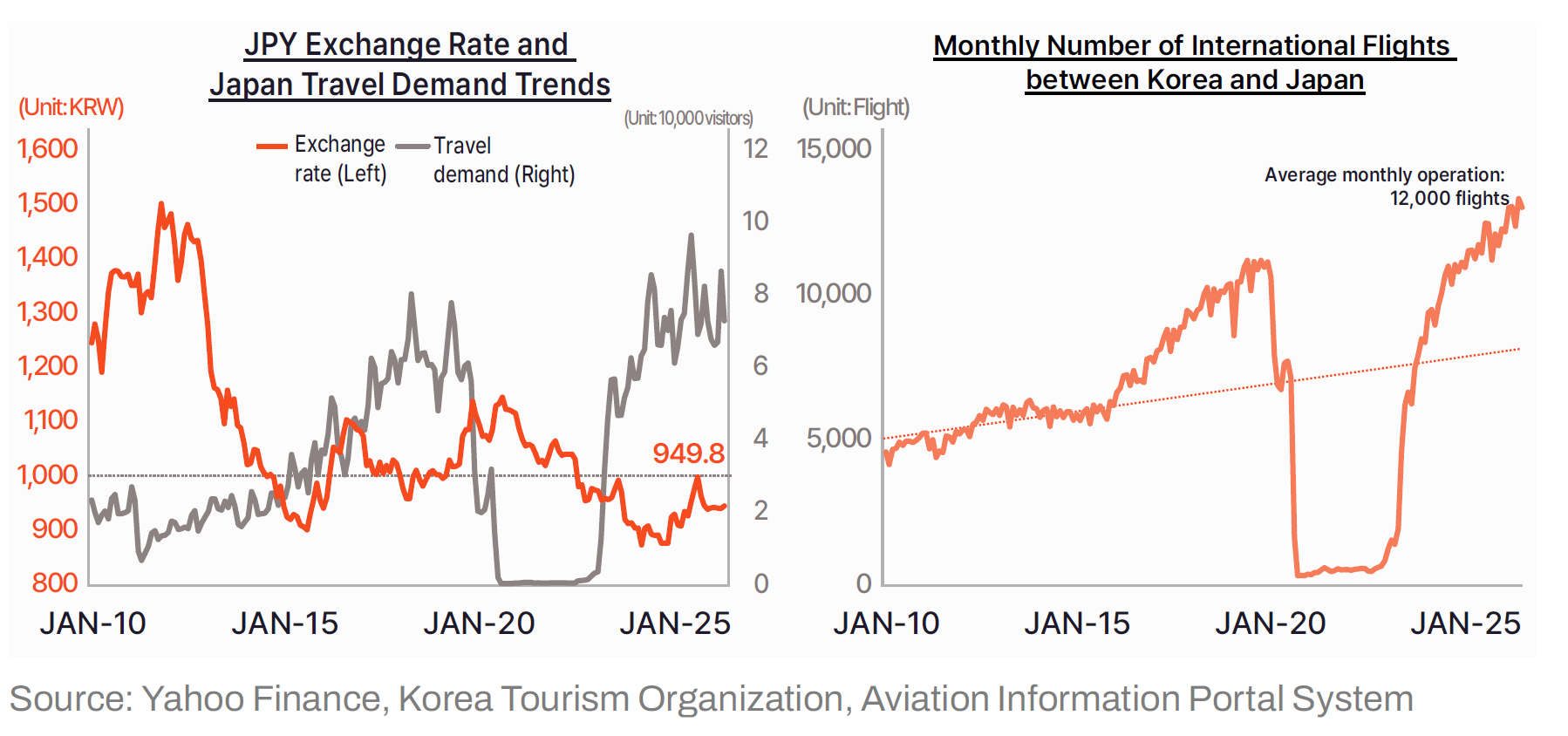

Demand outlook: a new peak with moderate growth. Korean outbound travel to Japan in 2026 is projected at approximately 9.66 million, up 4.4% year-on-year, setting another all-time high. In terms of growth speed, however, the market appears to be moving from explosive growth into a stabilization phase. The growth rate is similar to 2025 (+4.8%), suggesting a gradual upward curve that lifts the peak from an already elevated base.

Macro environment: policy direction of the Takaichi administration and the persistence of yen weakness. A supportive exchange-rate environment remains a key driver. Over the past year, KRW weakness and BOJ rate-hike discussions increased volatility. However, the newly launched Takaichi administration has signaled expanded fiscal spending and continued quantitative easing, easing some uncertainty. As of January 2026, the KRW/JPY rate fluctuates around KRW 920–940 per JPY 100, and a “relative weak-yen” environment is expected to persist through 2026, supporting travel sentiment.

Supply and risks: overwhelming connectivity and price competitiveness. Improved accessibility from expanded air supply is another growth driver. As Korean carriers aggressively launch and increase services to regional (secondary) Japanese city airports, Korea–Japan connectivity now spans 31 airports and 56 routes. Some cite further BOJ tightening and potential hikes in tourism taxes (accommodation taxes, departure taxes, etc.) as downside risks. However, overwhelming supply—about 12,000 flights per month—and intense fare competition among low-cost carriers (LCCs) are likely to offset upward pressure on travel costs. Given structurally secured price competitiveness and convenience, demand leakage driven by external variables is expected to remain limited.

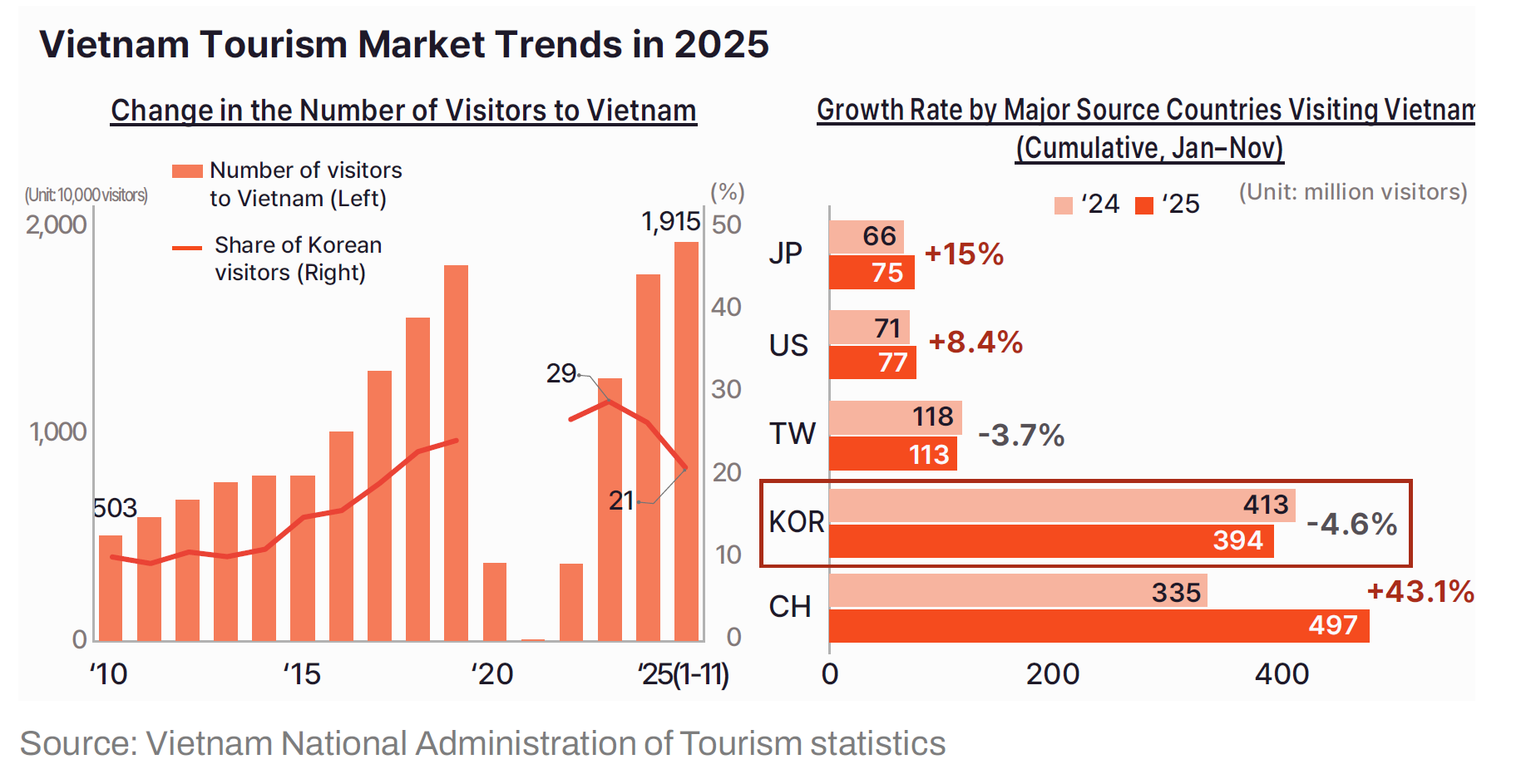

Demand outlook: a technical rebound based on base effects. Korean travel to Vietnam in 2026 is projected at approximately 4.56 million, up 3.9%. This reflects less of a structural growth and more a recovery that offsets the atypical demand decline in 2025. In other words, after a contraction caused by short-term headwinds, the market is expected to show a mild rebound supported by base effects.

2025 diagnosis: Vietnam’s global boom vs. Korea’s “solo contraction.” Vietnam enjoyed a record boom in 2025. According to the Vietnam National Administration of Tourism, cumulative inbound arrivals reached 19.15 million by November, setting an all-time high; China, the largest market, surged by 43.1% year-on-year. Korea—the second-largest market—diverged from this trend, recording a decline of about 4.6% (Taiwan also declined by -3.7%). This shows Korea’s market was uniquely sidelined amid broader growth.

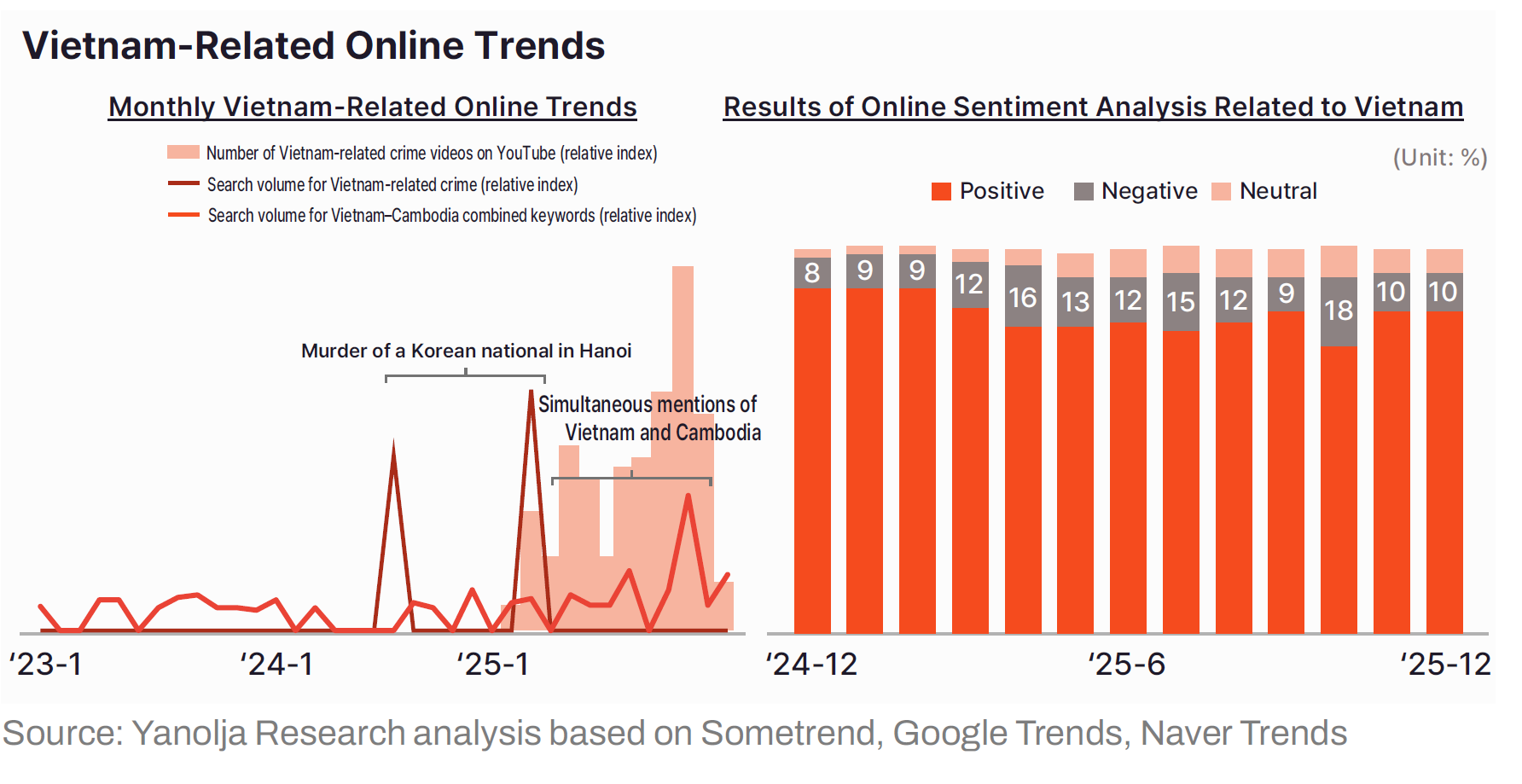

Drivers of decline: safety concerns and the spread of negative sentiment. One major factor behind weakened Korean demand was psychological contraction linked to perceived safety risks. Social data analysis indicates that media coverage on Vietnam-related safety/crime issues increased from the first half of 2025. In the second half, coverage of “Cambodia crime-compound” stories frequently exposed “Vietnam” as an associated keyword, amplifying negative perceptions. Online sentiment analysis showed negative sentiment peaking at 18% in some months, which translated directly into travel avoidance. Airlines reacted sensitively: among eight Incheon–Vietnam routes, all except Phu Quoc saw capacity adjustments ranging from a minimum of -6.9% to as much as -100% (service suspension).

Recovery factors: exchange-rate stability and promotion effects. This psychological contraction is expected to gradually ease from 2026. The biggest recovery engine is price competitiveness. Even amid recent KRW weakness, the KRW/VND exchange rate has remained highly stable, with volatility around 0.7%, limiting travelers’ perceived cost burden. In addition, airlines are starting to execute aggressive fare promotions to recapture demand, adding private-sector corrective efforts. Together, these factors suggest Vietnam will move from stagnation toward gradual normalization in 2026.

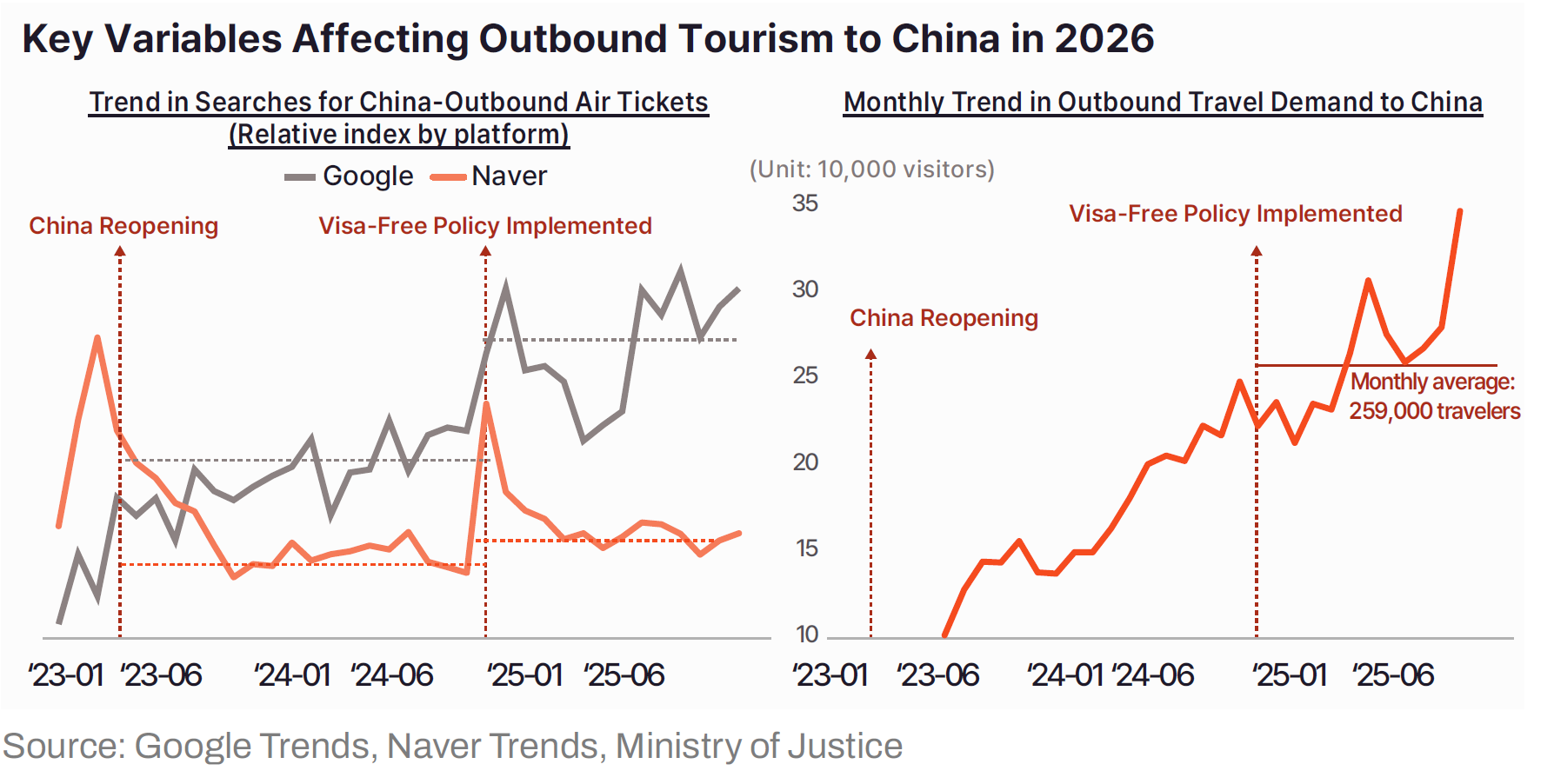

Demand outlook: the steepest upward curve among major destinations. Korean travel to China in 2026 is projected to reach approximately 3.94 million, up 24.2% year-on-year—the highest growth rate among the top destinations—indicating a shift from prolonged weakness into an expansion phase.

Recovery background: easing constraints plus base effects. Post-pandemic, China’s recovery lagged due to delayed aviation supply restoration, cumbersome visa procedures, and diplomatic tensions. From 2024 through 2025, these constraints gradually eased, and base effects from low prior performance strengthened the platform for a rebound.

Key driver: structural change triggered by visa-free policy. The pivotal trigger is visa-free entry. The visa waiver for Koreans introduced in November 2024 functioned as a decisive turning point. Data shows that immediately after implementation, baseline flight-ticket search volume for China shifted up by one level—evidence of structural improvement in travel sentiment, not merely a one-off spike.

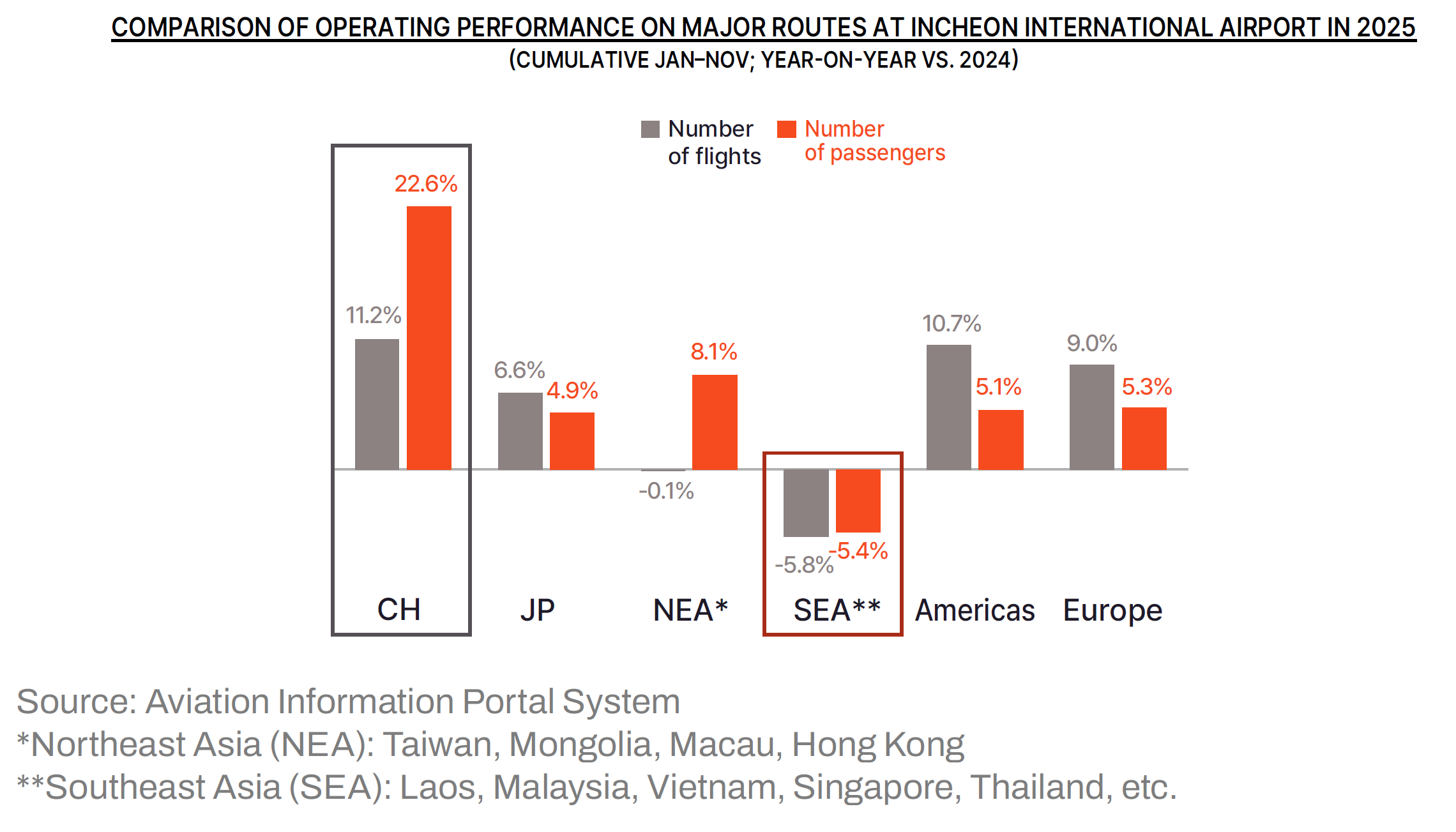

Supply situation: a virtuous cycle of route expansion and passenger growth. Policy effects are also visible in the joint rise of demand and supply. In 2025, average monthly outbound travelers recovered to around 260,000. On the supply side, Incheon–China flight frequency increased 11.2% year-on-year, while passenger volume rose 22.6%, far outperforming other routes. With improved accessibility and convenience, China is expected to absorb substitution demand away from competing destinations such as Southeast Asia and lead overall outbound market growth in 2026.

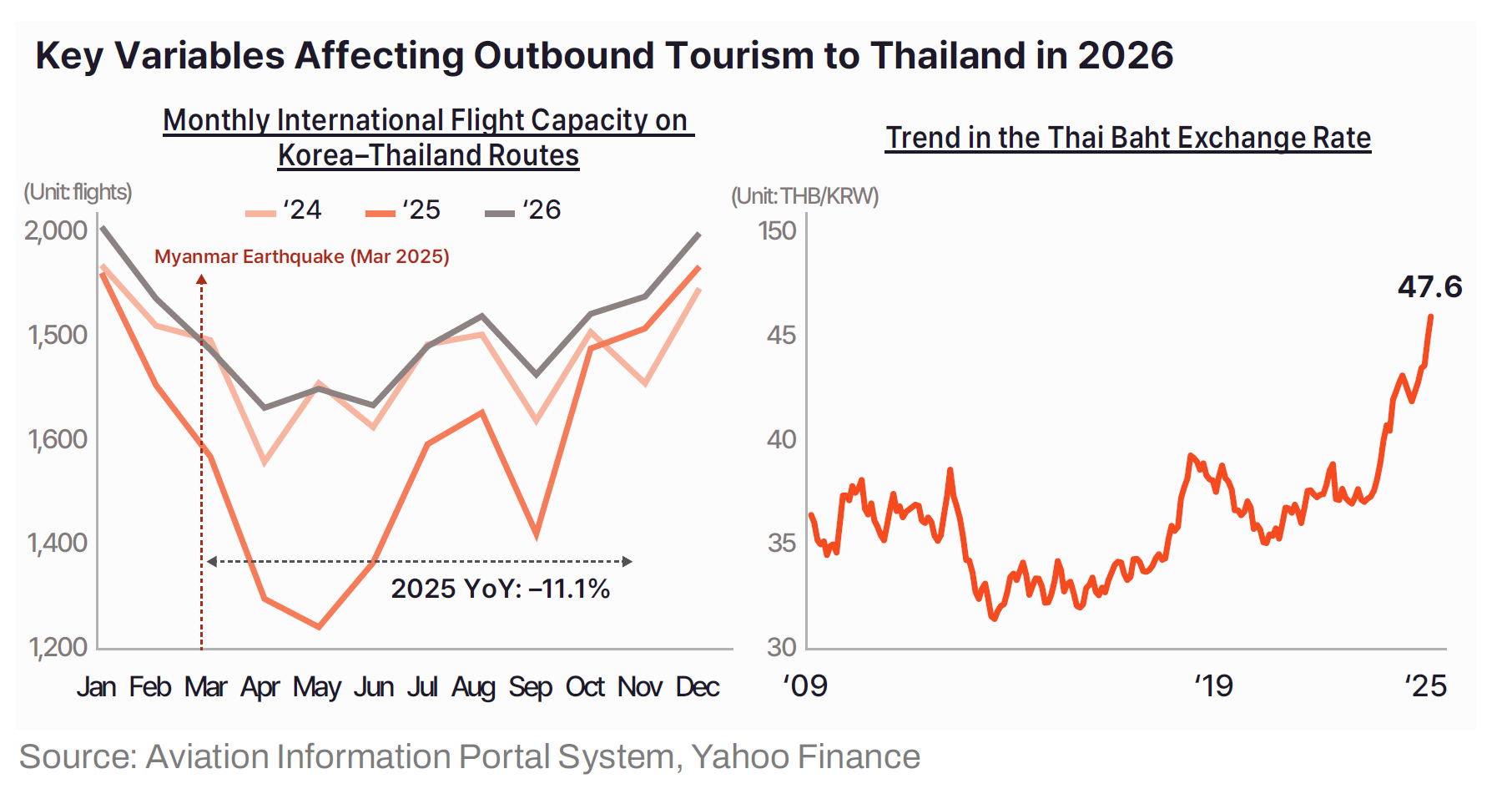

Demand outlook: the only contraction among major destinations. Korean travel to Thailand in 2026 is projected at approximately 1.56 million, a 3.4% decline year-on-year. It is the only destination among the top four where contraction is expected. The market remains about 17.5% below the 2019 level and 16.5% below the recent peak in 2024, suggesting a sustained phase of stagnation and adjustment.

Decline factor 1: aftereffects of natural disasters and supply cuts. A powerful exogenous shock underlies the downturn: the Myanmar major earthquake in March 2025. The resulting safety-related psychological contraction appears to persist in 2026. On the supply side, airlines reduced routes for risk management, and Thailand-bound flight counts fell 11.1% year-on-year. In other words, weakened sentiment translated into reduced physical supply, reinforcing a negative feedback loop.

Decline factor 2: weakened price competitiveness due to currency appreciation. On the economic side, exchange rates are a structural headwind. The Thai baht (THB) has maintained a long-term strengthening trend over the past decade and rose by about 11% versus the KRW over the past year, raising perceived travel costs. As a result, Thailand’s core competitive positioning as a “high-value, affordable resort destination” appears to be gradually weakening.

Decline factor 3: spillover of regional risks and the rise of substitutes. Geopolitical and safety risks also matter. Cambodia-related crime issues and border tensions have amplified broader safety concerns across Southeast Asia, placing Thailand under a similar “unsafe region” frame. With alternatives such as Japan and China offering strong air access and stable safety perceptions, Thailand’s choice priority is likely to decline.

Overall outlook: gradual adjustment rather than a sharp rebound. There is some possibility that aviation supply partially recovers toward pre-earthquake levels during 2026 and that the recent baht surge moderates. However, Thailand’s structurally strong baht trend and psychological safety barriers are unlikely to fully disappear in the short term. Consequently, rather than expecting a rapid V-shaped rebound, Thailand’s outbound market in 2026 is expected to remain in a conservative phase of stagnation or gradual adjustment.

As forecasted in this Insight, South Korea’s tourism market in 2026 is highly likely to enter an era of 20 million inbound visitors and 30 million outbound travelers. This outlook is not based on vague optimism; rather, it represents a "realistic trajectory" shaped by market resilience, the expansion of aviation supply, and structural changes in travel sentiment. However, as these numbers grow, a shadow becomes increasingly distinct: the "structural asymmetry" of the tourism industry.

The most urgent task is the surge in outbound demand that overwhelms even record-breaking inbound achievements, and the resulting entrenched tourism balance deficit. The gap of 10 million people between inbound and outbound travelers demonstrates a structural reality that can no longer be bridged by a volume-centered approach of "simply bringing in more people." Now, the benchmark for policy must shift from "numerical expansion" to a "transformation of value." Central and local governments must move beyond report cards focused on the number of visitors and shift their weight toward "qualitative productivity of tourism"—measuring how deeply an individual visitor experiences Korea and how much they spend. High-value-added content, such as luxury travel, medical and wellness tourism, and immersive K-culture experiences that go beyond simple sightseeing to encourage extended stays and consumption, is the most direct solution to alleviating the chronic deficit. This is a phase where transitioning from "tourism that brings many" to "tourism that leaves much behind" becomes the key to national competitiveness.

Secondly, Korea must establish a solid "tourism identity" that remains unshaken by geopolitical waves. Historically, Korean tourism has grown by relying on reflective benefits from external variables, such as changes in relations with China and Japan or fluctuations in the yen and exchange rates. However, the appeal of being a "substitute destination" has a short expiration date. Regardless of conflicts between neighboring countries or exchange rate conditions, Korea must establish itself as an "unrivaled tourism destination" that provides reasons for global travelers to visit in its own right. To achieve this, Korea's unique experiences must be accumulated as a "brand" rather than just "products." Furthermore, resilience against external shocks must be strengthened by easing the demand structure concentrated on specific countries and diversifying the market portfolio to Southeast Asia, the Middle East, and Europe. As dependency decreases, policy becomes steadier, and the industry gains the stamina to handle the long game.

Thirdly, the market in 2026 demands "data-driven agility" more than ever before. Variables such as security issues, natural disasters, the re-emergence of infectious diseases, and flight disruptions can become "Black Swans" that abruptly change specific markets at any time. Policy-making that relies on past experience or intuition is no longer effective. Governments and corporations must establish an operating system that uses forecasting models and real-time indicators as a compass to detect signs of change early and nimbly reallocate resources, marketing, routes, and products. Tourism policy must now evolve from the "art of simple planning" into the "science of adjustment."

The 2026 inbound and outbound demand forecast heralds a new renaissance for Korean tourism. What we need now is not simply more forceful rowing, but refined seamanship: reading the map that data provides and riding the flow of the waves. Whether Korea remains within one-dimensional growth defined by sheer volume, or steps into a mature future defined by qualitative advancement, ultimately depends on what we choose as the core policy standard. When Korea goes beyond simply increasing visitor counts and instead elevates “depth of stay,” “density of spending,” and “completeness of experience” to the center of national strategy, it will be able to firmly establish its standing as a true tourism powerhouse.

*To reference this article, please use the following citation: "Suckwon Hong, Deachul (David) Seo, SooCheong Jang, and Kyuwan Choi. (2026), Forecasting South Korea’s Inbound and Outbound Tourism Demand in 2026, Yanolja Research Insights, Vol. 35."

--

[1] Actual outbound departures from January to November 2025 totaled 26.80 million (source: Tourism Knowledge & Information System). Considering long-term trends and seasonality, cumulative departures are projected to exceed 29.0 million by December.