Korea Medical Tourism: Current Status and Strategies for Qualitative Growth

Kwanyoung Lee, Associate Research Fellow at Yanolja Research / [email protected]

SooCheong Jang, Professor at Purdue University & Director at Yanolja Research / [email protected]

Kyuwan Choi, Professor at Kyung Hee University & Director H&T Analytics Center / [email protected]

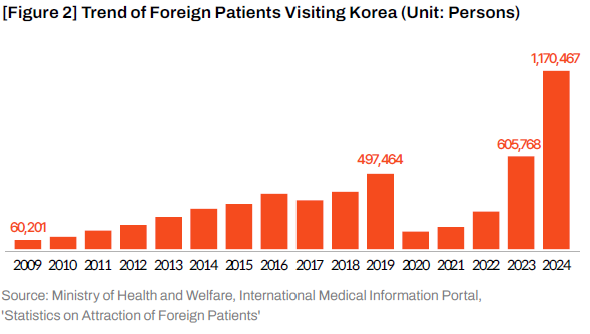

South Korean medical tourism has transcended "complete recovery" and entered a "new phase." In 2024, the number of foreign patients visiting Korea reached 1.17 million, marking not only the highest figure since medical tourism was institutionalized in 2009 but also more than double the pre-pandemic peak of 497,000 in 2019. This is a monumental achievement demonstrating that Korea's medical tourism industry is no longer a peripheral player evaluated merely on potential, but has emerged as a major supplier capable of absorbing global medical and wellness demand.

At the same time, this achievement aligns precisely with the need for a transformation facing the entire Korean tourism industry. Post-pandemic, Korea's tourism industry stands at a critical juncture where a shift toward qualitative growth is imperative, moving beyond a simple recovery phase. There are clear limitations to the low-value-added model centered on mass tourism; a paradigm shift toward high-value-added tourism is essential. Medical tourism lies at the center of this transition. Unlike general tourism, which often ends as a one-time visit, medical tourism possesses a structure that extends the length of stay through the full cycle of "pre-consultation – procedure/surgery – recovery – follow-up care." It simultaneously generates tourism and shopping consumption by accompanying persons and induces repeat visits from a customer lifecycle perspective. In other words, in the current situation where expenditure per foreign tourist is slowing, medical tourism is the most realistic and impactful sector capable of elevating the "quality" of the tourism industry.

So, why is medical tourism seen as having such great potential now? First, while medical costs are skyrocketing and waiting times are lengthening in developed countries, patients' options for treatment are expanding beyond borders due to the normalization of aviation and visa environments and the reduction of information costs. If Korea proactively enters the market at this point where structural demand shifts are accelerating, it can secure not just short-term inflows but "repeat visits" and "inertia of sustained demand." Second, the trust in the Korean Wave (Hallyu), accumulated through K-Drama, K-Pop, and creator content, is naturally transferring to "services entrusted with one's body," such as beauty, dermatology, dentistry, and body contouring. As global fandoms and beauty communities voluntarily share their Korean medical experiences, language and information barriers are lowered, and K-Beauty, wellness, and spas are easily combined before and after treatment. Hallyu is operating as a highly cost-efficient amplifier. Third, unlike existing tourism where demand is concentrated in peak seasons and weekends, medical tourism can fill occupancy rates during off-peak seasons and weekdays, as well as boost sales in downtown commercial districts, thereby complementing the structural vulnerabilities of the tourism industry.

However, the dazzling performance of medical tourism in 2024 does not immediately lead to a "sustainable industry." Current growth is a typical "concentrated growth," driven 68% by aesthetic medicine such as dermatology and plastic surgery linked to K-Beauty, and geographically concentrated in Seoul (85.4%). This means there is a powerful engine, but the risks are also significant. If Korea fails to industrialize other comparative advantages such as severe disease treatment, rehabilitation, check-ups, and K-Wellness, the market may be excessively exposed to economic and trend fluctuation risks associated with beauty demand. Moreover, as institutional foundations and management systems fail to keep pace with the speed of market expansion, the core axis of medical tourism competitiveness is shifting from "price" and "procedure speed" to "trust" and "follow-up care." Problems caused by unlicensed brokers and the absence of follow-up care can immediately transfer to national and city brand risks. With policies currently dispersed across the Ministry of Culture, Sports and Tourism, the Ministry of Health and Welfare, and the Ministry of Justice, it is difficult to design the entire patient journey as a single service. This is why it is urgent to bundle "medical services – tourism/shopping – stay – follow-up care" into a single "Integrated Patient Journey" and unify the evaluation and tracking system at the national level to support it.

Building on this awareness, this Insight aims to comprehensively address four areas: ① how global medical tourism demand is being restructured; ② an assessment of Korea’s performance in 2024 and the limits of regional and sectoral concentration revealed alongside that success; ③ a comparison of how major competitors like Thailand, Singapore, Malaysia, and Türkiye are packaging medical care, wellness, and leisure stays to enhance value; and ④ proposals for the key conditions required to establish a Korean model of medical tourism. Our goal is to move beyond merely achieving a “record year” for medical tourist arrivals and instead propose practical strategies to develop Korean medical tourism into a national strategic industry – elevating it into a global medical tourism hub with a multipolar structure not solely reliant on Seoul.

Structural Changes and Drivers of the Global Medical Tourism Market

The global medical tourism market is now not just a niche offshoot of tourism, but a growing market underpinned by structural demand. This is driven by three main factors: ① population aging and the rise of chronic diseases, ② skyrocketing healthcare costs and overburdened public systems in advanced countries, and ③ the post-pandemic travel rebound coupled with expanding demand for “treatment + tourism” experiences.

Drivers of Change in Global Medical Tourism Demand

① population aging and the rise of chronic diseases

Due to the global trend of aging, demand for medical services is increasing overall. According to the World Health Organization (WHO), the proportion of the world's population aged 60 and over is expected to nearly double from 12% in 2015 to 22% in 2050, and by 2030, 1 in 6 people worldwide will be aged 60 or over. As the elderly population increases, the prevalence of chronic diseases such as cardiovascular diseases, joint diseases, and cancer is also rising, leading to a rapid increase in demand for long-term care and specialized medical services. According to a study, about 74% of deaths worldwide are currently caused by non-communicable diseases (NCDs) such as cardiovascular disease, cancer, and diabetes, indicating that the disease structure has already shifted to center on chronic diseases.

Amid these changes, if domestic medical resources are insufficient or medical costs are excessively high, the number of patients going abroad to receive better medical services is rapidly increasing. In other words, medical tourism is emerging as a new alternative to fill the global medical demand gap caused by population aging and the increase in chronic diseases.

② skyrocketing healthcare costs and overburdened public systems in advanced countries

Another factor promoting medical tourism is the soaring costs and public healthcare overload faced by medical systems in developed countries. In major developed countries such as the United States, the United Kingdom, and Canada, as medical costs skyrocket and the inefficiency of public healthcare systems deepens, it is becoming difficult for patients to receive treatment at a reasonable cost in a timely manner. Patients from these countries have a clear purpose for treatment, so they are evaluated as a stable medical tourism demand group that is not significantly affected by external variables such as exchange rates or climate.

According to a report by The Commonwealth Fund, a US non-profit organization related to healthcare, medical expenditure relative to GDP in the US was 17.8% as of 2021, double the OECD average, and per capita medical expenditure is more than three times that of Korea. The cost per medical procedure is also several times higher than in countries with well-equipped medical tourism infrastructure such as Thailand, Malaysia, and Turkey.

In addition to cost issues, the problem of waiting for treatment due to the overload of the public healthcare system is also serious. The UK's National Health Service (NHS) recorded a record high of approximately 7.6 million people on waiting lists as of mid-2023. Cases have been reported where some heart disease patients have to wait more than a year to receive treatment. The UK media outlet The Independent, citing an announcement by the UK Labour Party, reported that the number of patients who died while waiting for treatment in 2022 could reach approximately 120,000. This is a representative example showing that the public healthcare system has already reached its limit. The situation is no different in Canada. According to a report by the Fraser Institute, a Canadian think tank, the average wait time for specialist consultation in 2024 is 30 weeks (about 7 months), a figure that has more than tripled compared to the 1990s (about 9 weeks wait).

As access to medical care in developed countries deteriorates rapidly, patients are choosing overseas medical tourism as an alternative to escape the constraints of cost and time. Consequently, medical tourism acts as a powerful "Push Factor" that drives "essential medical demand"—patients unable to receive treatment at a reasonable cost in a timely manner domestically—outside their borders.

③ post-pandemic travel rebound coupled with expanding demand for “treatment + tourism” experiences

Medical tourism demand, which had been suppressed as international movement was restricted and elective medical procedures were postponed during the COVID-19 pandemic, is appearing in the form of explosive "revenge consumption" after the pandemic resolved. As countries reopened their borders in 2022, the number of patients heading overseas to undergo postponed surgeries or health check-ups surged, and demand for complex medical tourism combined with general tourism is also rapidly increasing. In particular, as the trend of so-called "Healing Travel," which pursues travel and health management simultaneously, spreads, wellness tourist destinations are attracting new attention. Accordingly, hospitals are developing tourism packages linked to treatment, and resort hotels are launching stay-type wellness products in cooperation with medical institutions, accelerating the convergence of medicine and tourism.

Looking at the case of South Korea, the number of foreign tourists visiting Korea in 2024 was 16.37 million, recovering to only 80-90% of pre-pandemic levels, but the number of foreign patients increased 2-3 times compared to 2019, significantly exceeding pre-pandemic levels. Specifically, for some countries like Japan and Taiwan, while the overall inbound tourism recovery rate is only around 90%, medical purpose visitors surged by more than 500%, showing an explosive increase in complex demand combining treatment and travel.

This indicates that the accumulated demand for delayed medical services during the pandemic has erupted at once, and a new emerging medical tourism class seeking health check-ups or beauty/procedures during travel has appeared in earnest. In other words, medical tourism is now evolving beyond simple treatment purposes into a new travel pattern combining "treatment, recovery, and experience."

Structure of Global Medical Tourism Demand and Market Size Outlook

Analyzing these drivers comprehensively reveals that the global medical tourism market is essentially bifurcating into two distinct axes: the "Need-Driven Market" and the "Desire/Value-Driven Market." This distinction provides a key analytical framework for diagnosing the current status of the Korean medical tourism market and setting future strategic directions.

First, Need-Driven demand stems primarily from developed countries such as the US, UK, and Canada. In these countries, many patients find it difficult to receive timely treatment domestically due to soaring medical costs and overloaded public healthcare systems. Accordingly, "essential medical migration" for high-difficulty severe disease treatments such as cancer treatment, heart surgery, and hip joint surgery is actively occurring. The key determinants in this market are "Trust" and "Clinical Outcomes," and patients prioritize the expertise of medical institutions, the experience of medical staff, and treatment results.

On the other hand, Desire/Value-Driven demand is spreading thanks to cultural influence such as K-Culture and improved information accessibility due to ICT development. Medical services centered on mild cases, beauty, and prevention, such as dermatology, plastic surgery, dentistry, and health check-ups, form the mainstream of this market. This market is sensitive to "Price," "Trend (K-Culture)," and "Access," and consumer behavior is characterized by relatively short-term and elastic responses to trends.

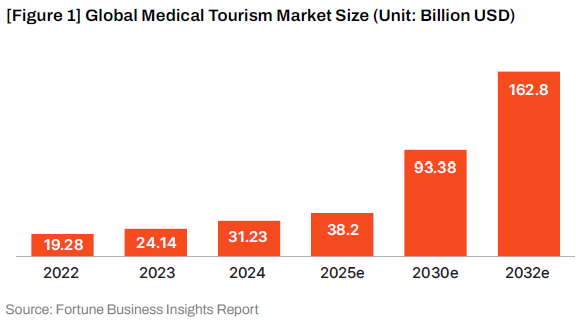

According to a report by market research firm Fortune Business Insights, the global medical tourism market size is expected to recover quickly from the shock of COVID-19 and grow at an annual average rate of 23.0% from 2025 to 2032. In other words, as structural pressures of aging, costs, and waiting times coincide with the travel recovery trend, medical tourism is operating as leverage for long-term growth in countries equipped with a combination of "price competitiveness + accessibility + trust."

Therefore, now is the strategic golden time for Korea to preempt the global medical tourism market. Through the combination of medical reliability, the spread of Hallyu culture, and digital infrastructure, Korea has sufficient potential to leap forward as a complex medical tourism hub covering both markets.

Development and Status of the Korean Medical Tourism Industry

Based on the growth drivers of the global medical tourism industry examined above, Korea is evaluated to have entered a structural leap phase by explosively absorbing medical tourism demand immediately after the pandemic resolution. In other words, strong leverage combining price competitiveness, accessibility, trust, and Hallyu (K-Culture) is converting medical tourism demand into actual performance.

Growth and Structural Characteristics of the Korean Medical Tourism Industry

① Leap in Scale

Post-pandemic, Korea's medical tourism industry has entered a stage of qualitative and quantitative growth beyond simple recovery. The number of foreign patients in 2024 was 1.17 million, an increase of 93% compared to the previous year, recording an all-time high. This shows not just a simple return of demand from before COVID-19, but the formation of a new structural growth trend.

Notably, this growth rate is much steeper than the inflow of general inbound tourists. As mentioned earlier, this is a result of the combination of reduced medical accessibility in developed countries, avoidance psychology regarding high-cost structures, and increased trust in Korean medicine combined with Hallyu. In other words, global medical tourism demand has been gradually shifting to Korea since the pandemic.

② Diversification of Demand Sources

On the demand side, a combination of high Hallyu familiarity and close proximity has led major neighboring countries—Japan, China, and Taiwan—to emerge as key sources of medical tourists to Korea. In 2024, Japan (441,000 patients), China (261,000), and Taiwan (83,000) all showed striking growth in medical visitor number. Japan’s medical tourists, for instance, surged about 6.4× compared to 2019 (68,000), and Taiwan’s surged ~35× (from just 2,300 in 2019) to become new growth drivers. China has also sustained a steady recovery since 2020, helping revive Korea–China medical exchanges.

These shifts indicate that Korean medical tourism has transitioned from a once unipolar structure (heavily dependent on a single country like China) to a multipolar demand portfolio encompassing Japan, China, Taiwan, and others. Importantly, patients from nearby countries tend to have shorter stays but higher repeat visit rates, which helps form a sustainable demand base over the long run.

③ Change in Medical Expenditure Portfolio

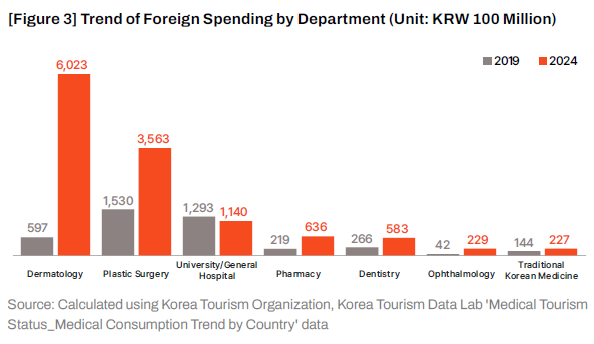

Changes are also very distinct on the expenditure side. From 2019 to 2024, total medical expenditure by foreign medical tourists expanded about threefold from KRW 409.1 billion to KRW 1.2401 trillion. Notably, the center of the expenditure structure is shifting rapidly from existing internal medicine and dentistry to dermatology and plastic surgery. Specifically, dermatology medical expenses increased about 10 times from KRW 59.7 billion in 2019 to KRW 602.3 billion in 2024, and when combined with plastic surgery, these two departments account for 77.3% of total medical expenses. This shows that post-pandemic medical tourism demand is concentrated on procedure-type and outpatient-type treatments characterized by quick decisions and short stays. On the other hand, university hospitals are showing relatively slower growth due to bed and surgery slot constraints, given the characteristics of high-difficulty surgeries and long-term inpatient-centered care.

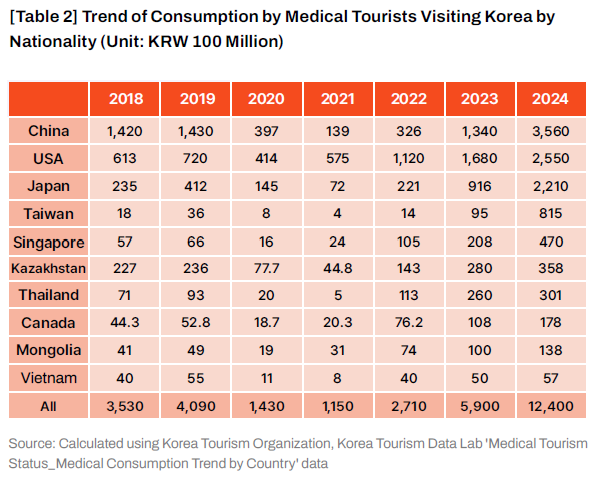

By country, China, the US, and Japan have been reorganized as the core markets for Korean medical tourism. China settled as the largest spending country, increasing about 2.5 times from KRW 143 billion in 2019 to KRW 356 billion in 2024. The US expanded from KRW 72 billion to KRW 255 billion, maintaining steady demand for high-cost treatments. Japan increased about 5 times from KRW 41.2 billion to KRW 221 billion, leading the high growth trend of medical tourism in the neighboring region. The growth of the Taiwan market is particularly notable, surging from KRW 3.6 billion in 2019 to KRW 81.5 billion in 2024.

This increase in consumption by major countries and the structural change in medical expenses centered on dermatology and plastic surgery suggest that Korean medical tourism is transforming into a high-value-added consumption industry centered on beauty and wellness. In other words, a new consumption pattern combining "health management and self-care" beyond simple treatment purposes is being formed.

④ Possibility of Regional Medical Tourism Amid Seoul-Centric Concentration

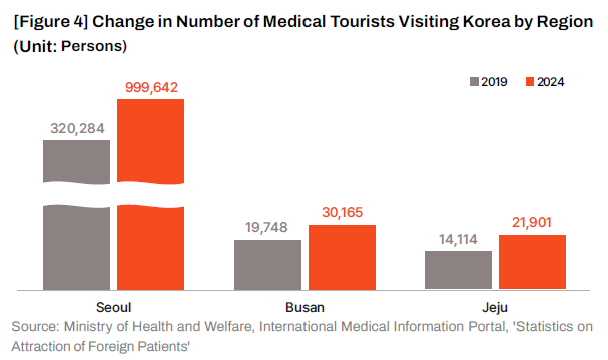

From a spatial perspective, the concentration of Korean medical tourism in Seoul is intensifying, but at the same time, the growth potential of regional medical tourism is also clearly appearing. As of 2024, 85.4% of all foreign patients receive treatment in Seoul, an increase of about 21% compared to 2019 (64.4%). This concentration is attributed to Seoul's competitive advantages, such as excellent medical infrastructure, hospitals with high global recognition, and transportation convenience.

However, it is noteworthy that even as Seoul's absolute share grows, regional hub cities like Busan and Jeju are securing independent growth bases. In 2024, Busan attracted about 30,000 foreign patients and Jeju about 22,000, successfully implementing models combining specialized medical treatments with tourism resources. Busan is attracting attention as a complex medical tourism model linking medical services and marine tourism, with specialized clinics developing in dentistry and orthopedics as well as beauty and plastic surgery. Jeju is establishing itself as a recovery-oriented medical tourism destination centered on check-ups and wellness, based on its clean environment and resort infrastructure.

As the number of medical tourists increases significantly in quantity, demand shows potential to expand from a mono-polar structure centered on Seoul to a multi-polar structure in the regions.

⑤ High Experience Value

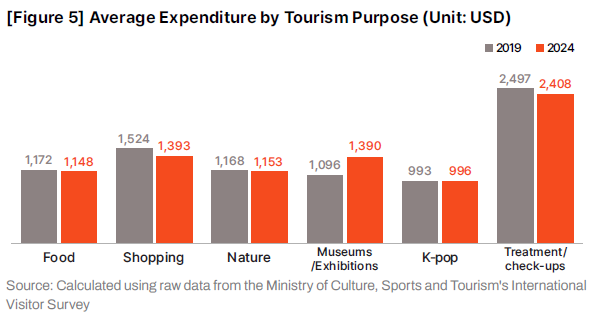

Medical tourism is establishing itself as a high-value-added tourism form with high experience value and strong loyalty, beyond simple treatment purposes. As of 2024, the average expenditure per person for medical tourists whose main purpose is treatment or health check-ups is $2,408, which is significantly higher than the average expenditure of general tourists. This shows that medical tourism is a complex high-spending segment accompanied by linked consumption such as luxury accommodation, food and beverage, and shopping during the stay, rather than simple consumption.

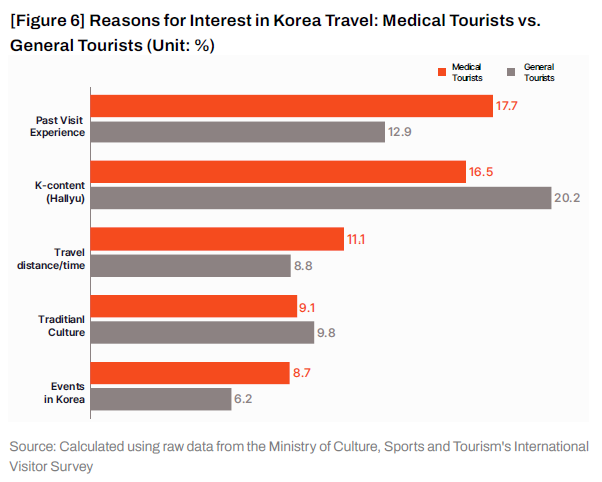

Also, in terms of satisfaction and revisit rates, medical tourism significantly outperforms general tourism. The proportion of medical tourists visiting Korea 4 or more times reached 38.6%, and "past visit experience" was cited most frequently as the "reason for interest in traveling to Korea." This suggests that medical tourism is developing into a relationship-building tourism form rather than a one-time visit. In other words, the quality and trust of medical services lead to revisits, forming a loyal demand base in the long term.

Analyzing this demand structure, the core engine of current Korean medical tourism growth is clear. It is centered on "Japanese and Chinese tourists visiting dermatology and plastic surgery clinics in Gangnam and Myeong-dong." This is a representative success story where the powerful cultural brand of K-Beauty combined with the reliability of medical services, successfully targeting the aforementioned "Desire/Value-Driven" market.

However, at the same time, this reveals the market concentration risk of Korean medical tourism. To secure long-term industrial stability and sustainability, diversification of the treatment portfolio and expansion of regional and stay-type medical tourism models are essential. It is necessary to expand the horizon beyond the short-term procedure-based market centered on beauty and dermatology to mid-to-long-term stay-type medical services such as wellness, recovery, and health check-ups.

Legal Foundation and Operational Mechanisms of Korea’s Medical Tourism

Korea’s Medical Tourism System and Development Stages

Medical tourism refers to travel for the purpose of treatment. The "Tourism Promotion Act" defines medical tourism as tourists receiving medical services such as diagnosis, treatment, and surgery at domestic medical institutions, and their accompanying persons engaging in tourism in parallel with medical services.

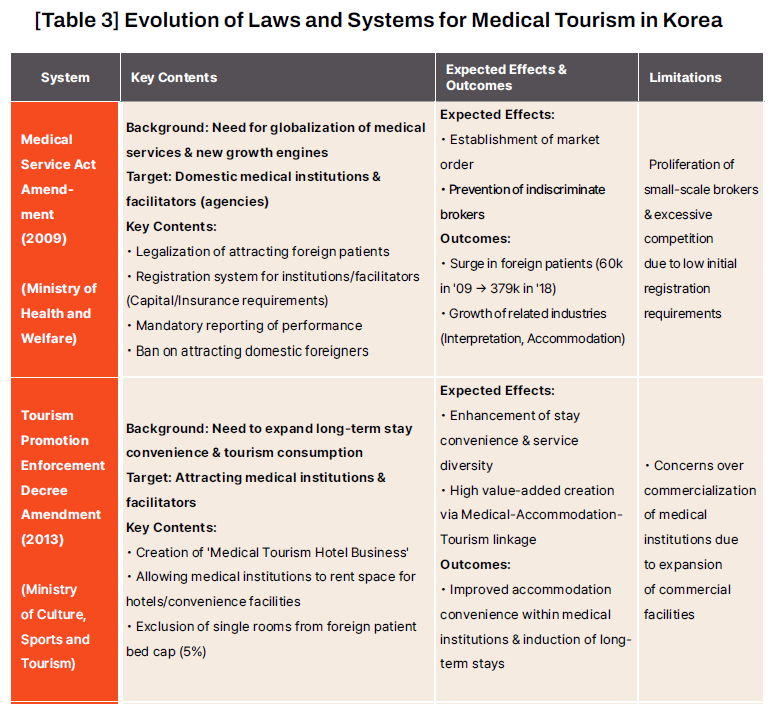

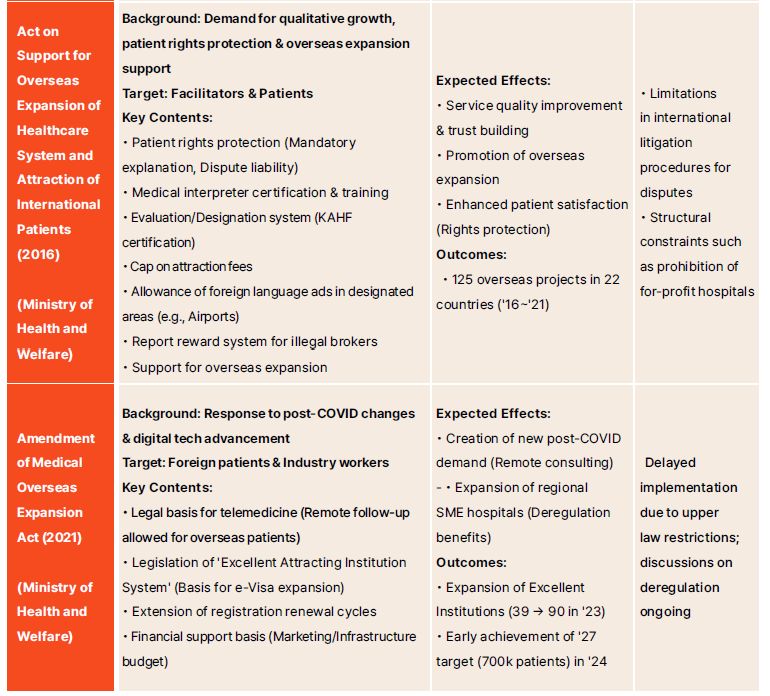

Korea's medical tourism system has evolved through a stepwise path: Market Opening → Establishment of Operational Discipline → Enhancement of Patient Rights & Quality → Advancement of Digital & Visa Infrastructure. The policy design focused on attracting global demand by enhancing accessibility and reliability of medical services rather than simple expansion of the tourism industry. The amendment of the Medical Service Act in 2009 legalized the attraction of foreign patients and established the basic framework for market order by introducing a registration system for attracting institutions and agencies and imposing reporting obligations. In addition, supplementary clauses such as restrictions on participation by insurance companies/agents, limiting foreign patient beds in general hospitals to within 5%, prohibiting medical advertisements targeting foreigners, and prohibiting attraction activities targeting foreigners residing in Korea were introduced to prevent side effects. However, in the early stages of the system, side effects occurred during the implementation period, such as the proliferation of small-scale brokers due to insufficient registration requirements.

In 2013, the Tourism Promotion Act Enforcement Decree was amended to create the "Medical Tourism Hotel Business," allowing accommodation and convenience facilities within medical institutions. This expanded patient stay convenience and consumption flow, and secured flexibility in bed operation by excluding single rooms when calculating foreign patient bed occupancy rates.

A qualitative turning point was the enactment of the "Act on Support for Overseas Expansion of Healthcare System and Attraction of International Patients" (Medical Overseas Expansion Act) in 2016. This law introduced mandatory prior explanation, dispute mediation/compensation systems, medical interpreter certification, professional training, evaluation/designation of attracting medical institutions (KAHF), caps on attraction fees (15% for tertiary general hospitals, 20% for general hospitals/hospitals, 30% for clinics), and permission for foreign language medical advertisements in designated areas (airports, trade ports, duty-free shops, etc.) to simultaneously strengthen quality, order, and branding. It also prepared grounds for supporting overseas expansion, creating over 120 business outcomes in 22 countries between 2016 and 2021, although global expansion was limited due to the prohibition of for-profit hospitals and limitations in international medical dispute procedures.

Post-COVID-19, the 2021 amendment advanced institutional infrastructure centered on digital-based management and visa system advancement. It prepared legal grounds for remote pre- and post-care between medical professionals for overseas foreign patients and legislated the "Excellent Attracting Institution System," establishing a basis for expanding electronic visas (e-Visa). Also, barriers to entry were lowered by adjusting registration renewal cycles and establishing regulations for supporting promotion and marketing for regional and small-to-medium medical institutions. As a result, the number of excellent attracting medical institutions increased from 39 in 2023 to 90 in 2024, and the government's target for attracting foreign patients (700,000 per year) was achieved early in 2024.

Over the past 15 years, Korea has rapidly improved the accessibility and trust of medical tourism through institutional infrastructure, but the policy focus still remains on medical providers. While successful in increasing the number of foreign patients, policy linkage in terms of expanding tourism demand, such as extending length of stay, consumption by companions, and linking to regional tourism, remains insufficient.

Structure and Functional Mechanism of Korea’s Medical Tourism System

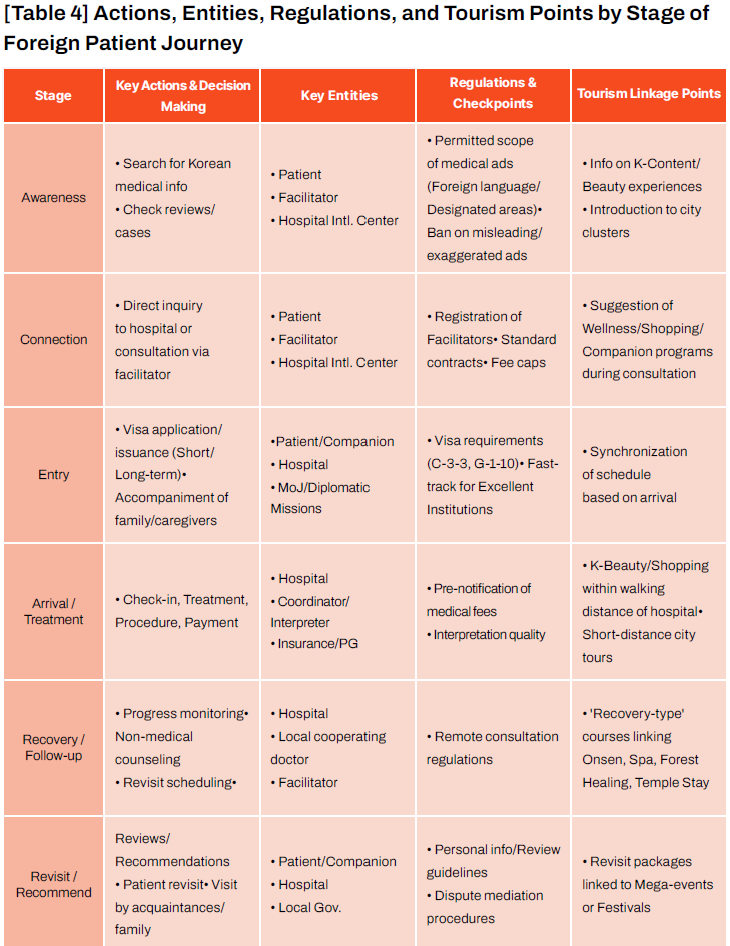

Korea's medical tourism industry consists of a complex system where various entities such as medical institutions attracting foreign patients, facilitators (agencies), and government agencies are linked through division of labor. Legal contact points such as visas, contracts, fees, and notification/compensation obligations are set at each stage leading to patient Awareness - Connection - Entry - Treatment - Follow-up Care. The development of this institutional infrastructure has evolved toward minimizing friction in the medical service usage process and enhancing trust in Korean medicine—a structure centered on medical supply capabilities—rather than inducing tourism.

The operating principle of Korean medical tourism from the perspective of a foreign patient is as follows: First, patients access Korean medical information in their home countries through internet searches, acquaintances' recommendations, or overseas briefings. Afterwards, they connect to hospitals directly through international medical centers of domestic hospitals or through facilitators (medical tourism agencies) registered with the Ministry of Health and Welfare. The former is a direct management type by medical institutions, and the latter is a brokerage network type path. After discussing the treatment plan and estimate, if the patient decides on treatment, they apply for a medical tourism visa. The C-3-3 visa (up to 90 days) is used for short-term treatment, and the G-1-10 visa is used for long-term care. The subjects are patients, family members, and caregivers (up to 2 people) invited by attracting institutions designated by the Ministry of Health and Welfare. Invitations from excellent attracting institutions designated by the Ministry of Justice can be issued quickly via electronic visa (e-Visa), usually processed within 3 days, greatly improving accessibility.

After entering the country, the patient proceeds with treatment and procedures under the guidance of the hospital's interpretation coordinator. Ancillary services such as aviation, accommodation, and tourism are linked in package form by facilitators registered with the Ministry of Health and Welfare. After the procedure, follow-up care is conducted within the scope of "ICT-based pre/post-care" (remote cooperation between medical professionals, counseling, education, etc.) stipulated in Article 16 of the "Medical Overseas Expansion Act." Since regular telemedicine between patients and doctors is not yet fully permitted institutionally, a three-way remote consultation involving the patient, local doctor, and Korean doctor is generally used in the field.

The roles of major service entities related to this are as follows: First, attracting medical institutions must meet statutory registration requirements such as medical malpractice liability insurance to legally treat foreign patients. Foreign inpatient beds in tertiary general hospitals are limited to within 5% of licensed beds, but single rooms are excluded from the calculation, ensuring a certain level of operational autonomy. Second, facilitators (medical tourism agencies) can legally provide patient mediation, interpretation, and accommodation/tourism linkage services through registration with the Ministry of Health and Welfare (capital, guarantee insurance, domestic office requirements), acting based on attraction agreements with hospitals. Third, the roles of government and public sectors are segmented. The Ministry of Health and Welfare oversees laws/systems and registration; the Korea Health Industry Development Institute (KHIDI) handles branding, promotion, and statistics. The Ministry of Culture, Sports and Tourism and the Korea Tourism Organization foster wellness and regional medical tourism, while the Ministry of Justice and the Ministry of Foreign Affairs handle visa policies and e-Visa operation. Local governments promote regional specialized medical tourism projects to spread the industry regionally.

Cost and contract structures are centered on self-payment and private insurance. Foreign patients are not covered by National Health Insurance and settle costs through out-of-pocket payments or overseas private insurance pre-approval or direct billing (pay & claim). The revenue of facilitators consists of patient service fees and medical institution attraction fees, capped at 15% for tertiary general hospitals, 20% for general hospitals/hospitals, and 30% for clinics. The contract structure generally consists of a dual system: patient-facilitator (service scope/fee) and facilitator-medical institution (referral/settlement/liability), utilizing standard contract forms to prevent disputes. To share risks, attracting medical institutions maintain liability insurance, and facilitators secure basic compensation capability by meeting guarantee insurance and capital requirements.

Advertising and attraction activity regulations are also enforced to maintain market order. Medical advertisements aimed at attracting foreign patients are prohibited in principle, but foreign language advertisements are exceptionally allowed in designated zones such as international airports, trade ports, duty-free shops, and special tourist zones. Even in these cases, detailed regulations such as prior review, prohibition of deceptive expressions, and restrictions on bias toward specific departments apply. Attraction activities are limited to introduction/mediation and provision of convenience; medical acts such as diagnosis or procedures must be performed by licensed medical personnel. Insurance companies, agents, agencies, and brokers are prohibited from attraction activities. While the obligation to display registration numbers is not uniformly prescribed by law, general obligations such as posting registration certificates and notifying rights and costs exist. When participating in public projects, demanding registration number display according to practical guidelines is increasing.

In conclusion, Korea's medical tourism industry operates in a direction where the roles and responsibilities of each entity are clearly divided under legal and institutional frameworks to standardize patient experience and minimize risks. While this structure has strengths in terms of trust, safety, and compliance, it still holds structural limitations in terms of tourism scalability and inter-industry connectivity, such as linking stay-type consumption, balanced regional development, and convergence with the wellness industry.

Strengths and Weaknesses of Korea’s Medical Tourism

Strengths of Korea’s Medical Tourism

The competitiveness of Korean medical tourism is based on the rapid growth of the beauty/dermatology sector, international trust in severe disease treatment, K-Culture (Hallyu) and price competitiveness, and excellent accessibility. First, the fact that beauty, dermatology, and plastic surgery are driving growth is evident in the 2024 statistics. Among foreign patients, dermatology accounted for about 705,000, or 56.6% of the total, followed by plastic surgery (140,000) and integrated internal medicine (124,000). Skin and beauty procedures have relatively short stay durations and are easy to combine with tourism, increasing the elasticity of medical tourism demand and hospital revenue.

Competitiveness is also prominent in severe disease treatment. Large university hospitals possess strengths in high-difficulty medical technologies such as cancer treatment, organ transplantation, heart surgery, and spine/joint surgery, leading patients from neighboring countries to visit Korea for severe disease treatment. According to the OECD's Health at a Glance 2023 report, Korea's Treatable Mortality rate is 43 per 100,000 population, significantly lower than the OECD average of 79. Additionally, according to a study published in the cancer journal Cancers in 2024, Korea's 5-year survival rate for stomach cancer is 68.9%, a very high level considering most countries are below 40%.

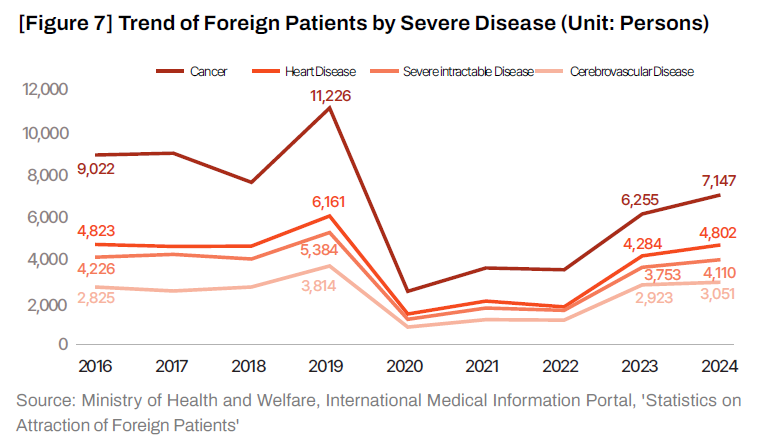

However, despite proven medical competitiveness, the growth of medical tourism in the severe disease treatment sector remains slow. Looking at the number of foreign patients for severe disease treatment such as cancer, heart disease, severe incurable diseases, and cerebrovascular diseases, there is a gradual recovery trend after COVID-19, but the speed is significantly slower compared to mild/beauty sectors like dermatology or plastic surgery.

For example, the number of foreign cancer patients visiting Korea in 2024 was 7,147, still falling short of the pre-pandemic level of about 11,000 in 2019. In contrast, the number of dermatology patients increased by 727.6% from 85,000 (2019) to 705,000 (2024) during the same period, showing a distinct contrast. The fact that the number of patients visiting Korea has decreased despite the continuous global increase in cancer incidence implies that severe treatment demand is dispersing to countries other than Korea. In other words, compared to the rapid growth centered on beauty/dermatology, Korea's medical tourism still faces limitations in expanding global competitiveness in the severe treatment sector.

Another growth engine for Korean medical tourism is cultural appeal, specifically the global spread of K-Culture. Awareness of Hallyu increases the combination of medicine and tourism, acting as a positive factor that increases both length of stay and consumption expenditure. According to a study, a 0.1-point increase in the Hallyu Index leads to a 5.02% increase in total demand for medical tourism to Korea (5.55% for women). Also, in a survey of 1,200 foreign patients conducted by the Korea Health Industry Development Institute in 2023, 49.7% of respondents answered that "K-Culture influenced their decision for medical travel." In particular, the group familiar with K-Culture showed an average expenditure per person about 27% higher than the group that was not ($7,308 vs $5,745). This result suggests that exposure to Hallyu goes beyond simply influencing medical tourism visit intentions and induces substantial economic effects leading to expanded consumption during the stay. In other words, the complex brand power combining K-Beauty and K-Health is strengthening the competitiveness of Korean medical tourism.

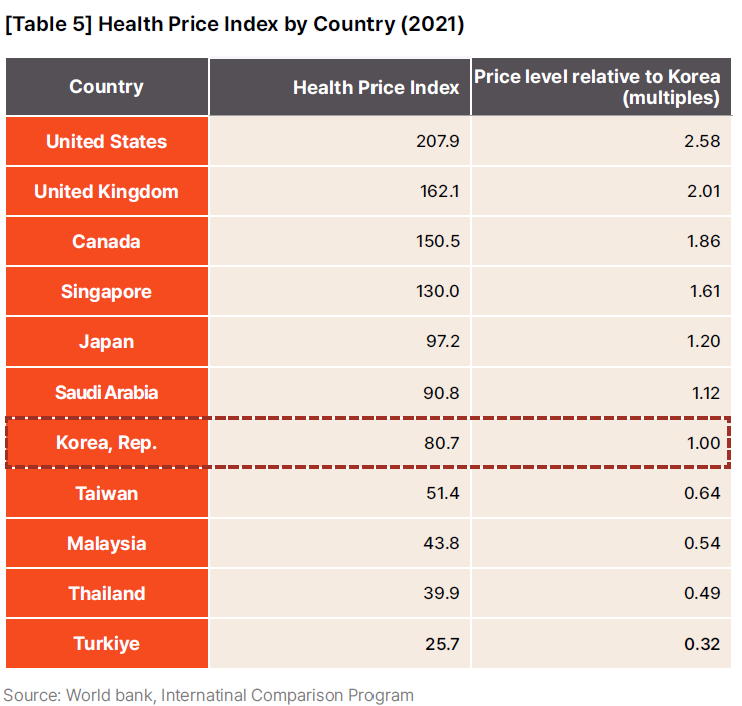

Finally, another factor that allowed Korean medical tourism to secure competitiveness in the global market is excellent price competitiveness. While possessing globally verified medical technology and reliability, Korea's medical service price level is much lower than major developed countries. According to the World Bank's International Comparison Program (ICP), as of 2021, when the world average is 100, Korea's health price index was 80.7, showing a price level lower than the average. In contrast, the US was 207.9 (2.58 times Korea), the UK 162.1 (2.01 times), Canada 150.5 (1.86 times), and Japan 97.2 (1.20 times), indicating that medical costs in Korea are significantly cheaper than most developed countries.

In summary, the strengths of Korean medical tourism can be summarized in four axes:

① Overwhelming demand for beauty/dermatology (especially dermatology/plastic surgery) combined with K-Beauty and high revisit convenience: Short stays allow for procedures/check-ups and easy combination with shopping/city experiences, leading to high revenue elasticity.

② Accumulated severe treatment capabilities centered on tertiary general hospitals: Holding performance indicators with international comparative advantage in high-difficulty fields such as cancer, transplantation, heart, and orthopedics, and trust verified by cases from the Middle East and Central Asia.

③ K-Culture Effect: Hallyu familiarity expands visit intentions and stay expenditure, and downtown clusters (e.g., Gangnam) and tourism infrastructure grow the connection value of "Medical + Experience."

④ Price and Accessibility: Low health price levels in international comparison and fast reservation/waiting structures (centered on clinics/specialized clinics) create a clear reason for choice: "rapid treatment at reasonable cost."

As these four axes interlock, holding the potential to drive high growth in the beauty sector for the time being while re-accelerating severe treatment through a trusted value chain of "overseas pre-consultation - domestic treatment - local follow-up care" constitutes the core competitiveness of Korean medical tourism.

Weaknesses of Korean Medical Tourism

On the other hand, for Korea to grow into a global medical tourism hub, the following weaknesses need to be addressed.

First is the lack of foreign patient service experience and usage convenience. In the 2024 overseas awareness survey by the Korea Health Industry Development Institute, "Excellent medical technology and treatment effect (54.9%)," "State-of-the-art medical equipment and facilities (49.2%)," "Hospital reputation (37.9%)," and "Reasonable price (35.7%)" were major reasons for choice, but the proportion of "Usage convenience (12.7%)" and "Foreign patient service infrastructure (3.8%)" was very low. Convenience-related satisfaction was also at the bottom (signs/directions ranked 35th out of 37 items, medical bill explanation 32nd, pre-guidance 28th, side effect explanation 29th, sufficient explanation by doctor 31st). While the etiquette of interpreters/coordinators had high satisfaction, overall, the evaluation of actual medical usage convenience falls short compared to treatment trust and technology.

Second is the inadequacy of the follow-up care system. There is significant concern that recovery management and post-treatment consultation are difficult as patients return to their home countries immediately after procedures/surgeries. In a 2022 survey, 39.5% cited post-treatment recovery management and 31.2% cited contacting medical staff as difficulties. Current laws only allow telemedicine between medical professionals, prohibiting telemedicine between patients and doctors, limiting systematic follow-up services.

Third is the limitation of supply-centered policies and insufficient tourism experience design. As performance is managed centered on the number of patients and medical expenses, key tourism KPIs such as length of stay, companion tourism expenditure, and weekday/off-peak activation are not sufficiently reflected in policies. In 2024, the entire treatment portfolio was concentrated 77.3% in dermatology/plastic surgery, and 85.4% of foreign patients flocked to Seoul, showing severe regional and department bias. There is a lack of systematic planning for stay experiences other than medical acts, showing limitations in connecting to actual expenditure expansion and regional tourism activation. Institutionally, while medical access such as cosmetic VAT refunds, attraction, visas, and interpretation has progressed rapidly, mechanisms for expanding stay/consumption based on recovery wellness and K-Culture lack standardization and incentives. Consequently, while medical technology and trust competitiveness are high, the policy frame to convert/expand this into a tourism value chain is weak, limiting high-value-added performance improvement.

The final weakness is the absence of a medical tourism control tower. Currently, medical tourism tasks are fragmented across the Ministry of Health and Welfare/KHIDI, Ministry of Culture, Sports and Tourism/Korea Tourism Organization, Ministry of Justice, and local governments, making integrated national strategies and inter-ministerial cooperation difficult. For example, attraction institution management and dispute mediation are managed by the Ministry of Health and Welfare, product development and overseas promotion by the Ministry of Culture, Sports and Tourism, and visa policies by the Ministry of Justice, reducing policy consistency and execution speed.

In summary, the weaknesses of Korean medical tourism are:

① Lack of Patient Experience & Usage Convenience: Satisfaction is low at key touchpoints like signs, movement paths, pre/post explanations, and cost notifications, creating a gap between technology-trust and perceived convenience.

② Gap in Follow-up Care System: Despite high demand for recovery/inquiry from returning patients, a consistent tracking system is absent due to the prohibition of patient-doctor telemedicine.

③ Limitations of Medical Supply-Centered Policy: Policy/performance indicators are biased toward patient numbers/medical fees, failing to reflect tourism KPIs (stay, companion spending, off-peak demand), with severe department/regional bias.

④ Fragmented Governance & Lack of Control Tower: Divided responsibilities reduce policy consistency and execution speed in visas, dispute mediation, branding, and product development.

These four weaknesses act as bottlenecks hindering the virtuous cycle structure connecting demand influxed by accessibility and trust to stay/consumption and weekday (off-peak) demand, necessitating policy supplementation.

Strategies of Leading Medical Tourism Nations

To leap forward as a global medical tourism powerhouse, Korea needs to accurately identify its strengths and weaknesses and refer to the cases of major competitors. Singapore, Thailand, Malaysia, and Turkey are representative countries that have fostered medical tourism with different strengths and strategies.

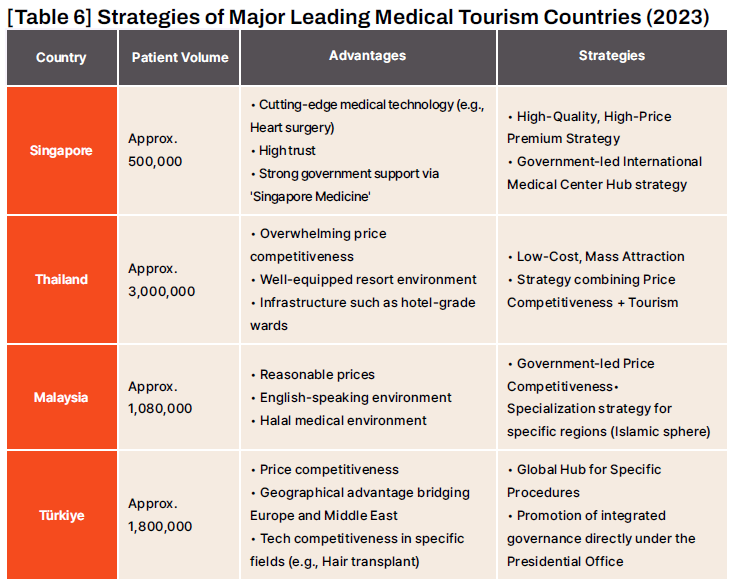

Singapore - High-Trust High-Tech Medical Hub Strategy

Singapore has long aimed to be a high-end medical tourism hub in Asia. Government-led collaborative policies are prominent; in 2003, the multi-agency medical tourism initiative "Singapore Medicine," operated jointly by the Ministry of Health, Tourism Board, and Economic Development Board, was launched to revitalize the sector. Leveraging an English-speaking environment, cutting-edge medical technology, and hospitals with world-class medical staff, it has grown by attracting patients from Indonesia and Malaysia as well as the US and Europe since the mid-2000s. Various measures were implemented, including establishing overseas promotion offices, recruiting overseas medical professionals (relaxing foreign nurse visa restrictions), and public-private joint marketing. Singapore's strength lies in sophisticated high-tech surgeries and specialized treatment fields. In the 2021 World Index of Healthcare Innovation (WIHI) published by the US non-profit think tank FREOPP, Singapore ranked 7th globally, and in the Medical Tourism Index (MTI), Singapore ranked 2nd after Canada, emerging as a preferred destination for Americans. It is evaluated as the best in the region for complex heart surgeries, organ transplants, and cancer treatments, targeting wealthy patients with high-quality medical environments and services.

Thailand - Price Competitiveness, Hospitality, and "Wellness" Combination Strategy

Thailand is a top-tier country globally in terms of medical tourism patient numbers. Since the early 2000s, centered on Bumrungrad Hospital in Bangkok, it has attracted patients by promoting affordable yet high-quality medical services. According to ISEAS, a research institute under Singapore's Ministry of Education, the number of foreign patients in Thailand increased to about 2 million in 2012 and 3.5 million in 2019, recovering to about 3 million in 2024 after a temporary decline due to COVID-19. Foreign currency revenue from medical tourism is also expected to increase from about $9.1 billion in 2019 to $24.4 billion in 2027. The Thai government designated medical tourism as a national strategic industry, implementing policies such as encouraging overseas marketing by hospitals, medical expense refunds, and immigration relaxation. It built an image of healing travel in a resort destination by developing programs linking wellness spas and tourism. Price competitiveness, tourism infrastructure, and hospitality services are the main success factors. There are many English-speaking medical staff, and patient-tailored services such as hotel-style patient rooms, interpretation coordinators, and airport pickups are well-received. It is also investing about $131 million to create a Phuket International Medical Tourism Hub to strengthen tourism appeal.

Malaysia - Government-Led "Halal Medical" Specialization Strategy

Malaysia designated medical tourism as a national strategic industry in the early 2000s and pushed for institutional improvements. In 2009, it established the Malaysia Healthcare Travel Council (MHTC) under the Ministry of Health to oversee policy, overseas promotion, and certification, targeting international markets with the brand "Malaysia Healthcare Travel." Its strengths are reasonable costs and an English-speaking environment. Major surgery costs are 70-80% cheaper than in the US, and most medical staff can treat in English, making it accessible to Western patients. It supports patient convenience through medical expense tax benefits, simplified electronic visas, and long-term stay program development. It increased trust by transparently disclosing medical costs through the "OpenMenu Plus" system. It has competitiveness in heart disease, In Vitro Fertilization (IVF), and comprehensive check-ups, attracting patients from Southeast Asia and the Middle East. A medical/wellness hub was built in the Iskandar region, forming a complex cluster combining hospitals, recreational facilities, and resorts. Targeting the Middle East market, it introduced the concept of "Halal Medicine," providing treatment environments tailored to Islamic law, female-only treatment spaces, prayer rooms, and Halal-certified meals, allowing upper-class Middle Eastern patients to receive treatment with peace of mind. It expanded direct flight routes in cooperation with major Middle Eastern airlines and established local promotion networks.

Türkiye - Integrated Strategy Targeting Middle Eastern/European Patients via Presidential Direct Governance

Türkiye actively fostered medical tourism after the 2010s utilizing its geopolitical advantage between Europe and the Middle East. The medical tourism agency USHAS, established in 2019, is directly under the Presidential Office. It established a "Health Tourism Master Plan" in cooperation with the Ministry of Health and Ministry of Tourism, developing clusters and conducting international marketing. It provides products combining hospitals, hotels, and tourism packages in Istanbul and Antalya, which have good aviation accessibility. Türkiye's strengths are low costs and competitiveness in specific fields. It offers plastic surgery, dental treatment, ophthalmology (LASIK/LASEK), and infertility treatment at 20-30% of the cost of the US and Western Europe, making it popular in the Middle East and Europe. It is a global powerhouse in hair transplantation, visited by hundreds of thousands annually. The government built patient-friendly infrastructure through tax benefits, support for overseas marketing of internationally accredited hospitals, and packages/airport-hospital pickup services linked with Turkish Airlines.

The cases of leading medical tourism countries examined above show a clear commonality. Successful medical tourism countries all have a clear strategic positioning at the national level and operate a strong single governance, a "Control Tower," to execute it.

Strategic Proposals: Plan for Building a Sustainable Medical Tourism Ecosystem

The achievement of 1.17 million patients in 2024 can be interpreted as the success of "Act 1" of K-Medical Tourism. Now, based on this achievement, it is time to add new growth axes and move toward "Act 2" of "Sustainable Qualitative Growth." To this end, a fundamental policy transformation beyond fragmentary improvements is needed, which should be promoted around the axes of Governance, Trust (Regulation), Experience (Tourism/Wellness), and Industry (Platform).

The following are strategic proposals presented by the authors of this Insight.

Proposal 1: [Strong Integrated Control Tower] Establishment and Operation of (Tentative) 'K-MTA (Korea Medical Tourism Promotion Agency)'

The first step and most urgent task is governance innovation. There is a need to establish a strong control tower to integrate currently fragmented policy functions and oversee strategies at the national level. To this end, we propose the establishment of the (tentative) 'K-MTA (Korea Medical Tourism Promotion Agency)', an independent organization under the Presidential Office or the Prime Minister's Office that transfers, integrates, and coordinates medical tourism-related functions of relevant ministries (Benchmarking models: Turkey's USHAS, Malaysia's MHTC). This organization should have strong authority to oversee policies, such as establishing national mid-to-long-term roadmaps, integrated accreditation/evaluation of attracting medical institutions and agencies, integrated management of the "Medical Tourism, Korea" national brand, and establishment/operation of an ICT-based national integrated follow-up care platform. In the current fragmented structure (As-Is), the Ministry of Health and Welfare, Ministry of Culture, Sports and Tourism, and Ministry of Justice pursue their own policies, leading to mismatches. The K-MTA needs to become a Hub (To-Be) to coordinate the functions of related ministries, communicate directly with the industry, and execute a consistent national strategy.

Proposal 2: [Trust Recovery - Regulatory Improvement] Building a 'Transparent Market Ecosystem'

If strong governance is established, the next task is to focus on regulatory improvement for "Trust Recovery," i.e., market transparency. To this end, it is necessary to abolish the "registration system," which has virtually become nominal, and switch to a "K-MTA Official Attraction Agency Accreditation System" that grants qualifications only to companies meeting strict requirements. These accreditation requirements should include upward adjustment of capital and guarantee insurance, "mandatory subscription to medical malpractice liability insurance," and "mandatory use of standard contracts." In particular, strong penalties should follow if involved in "ghost surgeries" that threaten patient safety. In addition, to resolve medical disputes quickly and fairly, the use of K-MTA certified standard contracts should be mandatory, and a clause stating that mediation by the "Korea Medical Dispute Mediation and Arbitration Agency" applies first in case of disputes should be specified in the contract to resolve patient anxiety and secure procedural transparency. Through this, by guaranteeing the rights and interests of overseas patients at a level equal to domestic patients, we must raise the international credibility of "K-Medical Tourism" and ensure that trust in the Korean medical system becomes a stepping stone for sustainable growth.

Proposal 3: [Experience Innovation - Regulatory Improvement] Establishment of 'K-Smart Follow-up Care' System

If trust recovery is a matter of market purification, "Experience Innovation" is a matter of sustaining relationships with patients. For this, the establishment of a "K-Smart Follow-up Care" system and related regulatory improvements are necessary. Patients who have received Korean medical services abroad may feel great anxiety about "disconnection" afterward. To resolve this, an amendment to the Act on Support for Overseas Expansion of Healthcare System and Attraction of International Patients is necessary. In particular, it is necessary to create a special clause explicitly permitting ICT-based communication (remote consultation) between patients and doctors for "non-medical purposes (consultation, monitoring, education, medication guidance)" limited to "foreign patients who have received treatment in Korea and returned home." Based on this, a plan to build a "National Integrated Follow-up Care Platform" organized by K-MTA (Government) and participated in by tourism platforms (Private) can be considered. This platform aims for an integrated medical/tourism service system that continuously manages patients from post-treatment to recovery stages. For example, primary multilingual counseling services can be provided via AI chatbots to minimize language barriers, and wearable devices (IoT) can be linked to monitor the patient's vital signs in real-time after surgery. Also, if abnormalities are detected, a method of immediately connecting to a 3-way video consultation system between the local cooperating doctor, the Korean attending physician, and the patient is possible. Such a collaborative system can be sufficiently implemented within the scope of remote collaboration under current medical laws. Especially for severe treatment patients, such a collaboration system is essential for securing patient trust and guaranteeing treatment continuity. Beyond short-term treatment, it will play a key role in building a sustainable medical tourism ecosystem including follow-up care and long-term relationship formation.

Proposal 4: [Strengthening Tourism and Expanding to Wellness] Maximizing 'Medical + Tourism' Synergy

Furthermore, to maximize the immense tourism ripple effect of medical tourism and alleviate the concentration on K-Beauty, a strategy of "Strengthening Tourism and Expanding Wellness" must be pursued in parallel. Medicine should be redefined as an "Anchor Product" attracting high-value tourists, and "Recovery Tourism Products" aimed at extending lengths of stay and creating high added value need to be developed. It is particularly important to expand medical tourism to "K-Wellness" as a new growth engine. For example, after receiving a procedure in Gangnam, private spas and healing stays can be linked at Jeju 'Haevichi Hotel & Resort' (sunset yoga, meditation) or Seoul Seocho 'Heidi House' (12 themed spas). Also, a model linking check-ups or treatments at large Seoul hospitals with oriental medicine/natural healing programs at Jeonnam Jangheung 'Mind Health Healing Center' (customized healing) or Jeonbuk Gochang 'Wellpark City' (germanium hot springs) is possible. Strategies to package newly selected excellent wellness tourist destinations for 2025, such as Incheon Ganghwa 'Yakseokwon' (Ganghwa mugwort oriental experience) or Incheon Jung-gu 'Cha Deok Bun' (Tea Omakase), can also be considered. To support global marketing of these regional wellness products, regulatory relaxation allowing limited medical advertising for non-covered items including foreign languages within regional specialized development zones and government-designated wellness clusters is also necessary.

Proposal 5: [Future Strategy - Industry Preparedness] A Market Led by 'Trusted Platforms'

The future global medical tourism market will be reorganized into a "High-Trust, High-Value Market" centered on transparency of information and trusted platforms. Patients in the post-pandemic era recognize Safety and Trust as core values alongside simple Cost factors. Accordingly, large travel/tourism platforms like Yanolja (NOL) and Klook need to pioneer the global medical tourism market based on core competencies of "Trust" and "Integrated Journey Management." Platforms can solve structural problems of trust, quality, and information asymmetry that individual hospitals or small agencies find difficult to resolve independently, through technology and trust mechanisms. In other words, future medical tourism competition will come down to "who designs and continuously manages a more trustworthy journey."

Along with this, the government must expand participation opportunities through segmentation of excellent attracting institution selection criteria and provision of policy incentives so that the market structure centered on large platforms does not act as a barrier to entry for small and medium-sized facilitators. Ultimately, when the technology of large platforms and the field expertise of small and medium institutions are combined, the Korean medical tourism industry can develop into a next-generation medical tourism ecosystem that satisfies trust, safety, and integrated experience.

Conclusion: Toward Genuine 'K-Medical Tourism' Combining Tourism and Wellness Beyond K-Beauty

The Korean medical tourism industry achieved a remarkable result of attracting 1.17 million foreign patients in 2024 based on world-class medical technology, the combined effect of K-Beauty and Hallyu culture, and reasonable price competitiveness. This is a signal of a structural leap proving the possibility of transitioning to a high-value-added industry through medical tourism, beyond simple tourism recovery.

However, there are still significant structural limitations to be resolved. Most foreign patients are concentrated in Seoul, and medical departments are biased toward dermatology and plastic surgery. Patient convenience and follow-up care systems are insufficient, and fragmented policy governance blocks the integrated development of the industry.

The common lesson from leading global medical tourism nations is clear. Establishing a national integrated control tower, creating a transparent market ecosystem based on trust, and a smart follow-up care system that innovates patient experience are key. Here, maximizing the synergy of medical services with tourism and wellness to extend length of stay and combining them into a complex model creating high added value is necessary.

When these strategies are pursued in parallel, Korean medical tourism can evolve from fragmentary growth centered on beauty into a multi-layered industrial structure capable of high-difficulty severe disease treatment and long-term patient management. This must lead to an integrated patient experience management system covering the entire treatment process, multi-nucleation of regional medical tourism, and establishment of a global trust base, beyond simply expanding patient numbers. Now is the time for the public and private sectors to cooperate closely to embark on innovative governance reorganization, such as the establishment of the 'K-MTA (tentative, Korea Medical Tourism Promotion Agency)'. Under strong leadership, policy, industry, and academia must gather to establish strategies to leap forward as a world-class medical tourism hub and boldly execute them.

The future of Korean medical tourism depends on building a unique platform where high-value medical services fuse with tourism, culture, and wellness, and executing global customer-tailored strategies. Ultimately, the vision the industry should aim for is to move beyond procedure-centered "K-Beauty" to complex "K-Medical Tourism." This will go beyond simple economic performance to become a strategic asset of Korea that elevates the national brand and maximizes ripple effects across diplomacy, industry, and culture. The "Golden Time" created by K-Culture is not eternal. Now is the time to utilize that momentum to build trust infrastructure and sustainable systems looking ahead 50 years. The future of K-Medical Tourism ultimately depends on our decisions and actions today.