Korea’s Inbound and Outbound Tourism Performance in 2025

Inbound Tourism Performance

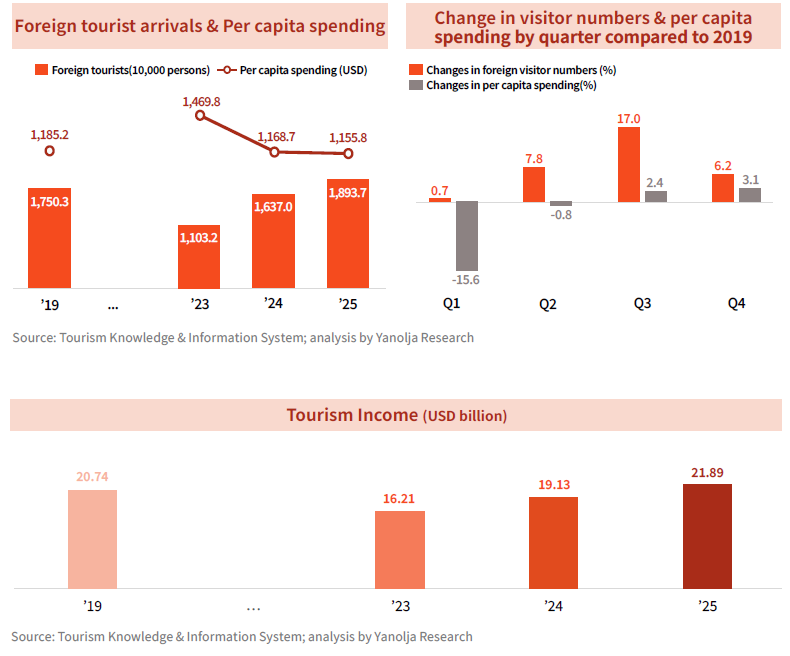

1. Inbound Tourist Arrivals: Breaking Records with 18.93 Million Visitors

In 2025, the Korean tourism market attracted approximately 18.937 million foreign tourists, surpassing the pre-pandemic record of 2019 (17.503 million) by 8.2% and setting a new all-time high. Analyzing quarterly trends, the year began with a modest growth of 0.7% in Q1 compared to 2019, followed by sustained growth rates of 7.8% in Q2, 17.0% in Q3, and 6.2% in Q4. This indicates that the market has moved beyond mere recovery and entered a phase of structural expansion.

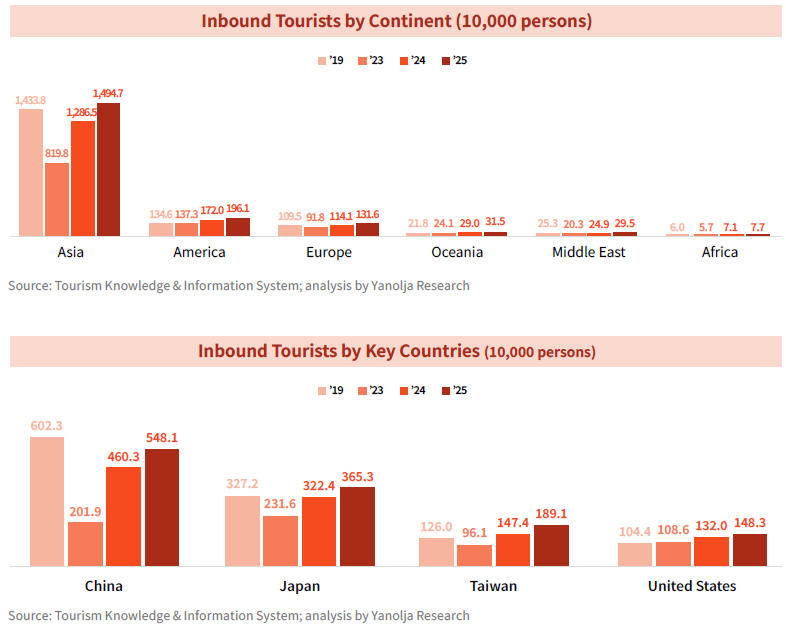

The pattern of recovery varied significantly by continent. While the Asian market reached a stage of full restoration with 14.947 million visitors in 2025 (a 4.2% increase from 2019), the most notable development was the explosive surge from non-Asian regions. Growth in long-haul markets—including the Americas (1.961 million, +45.8%), Europe (1.316 million, +15.3%), Oceania (0.315 million, +44.5%), the Middle East (0.295 million, +18.6%), and Africa (0.077 million, +27.3%)—demonstrates that Korea’s inbound market has reached a turning point, diversifying away from a structure centered on a few neighboring countries toward a truly global base.

By country, China solidified its status as the largest source market with 5.481 million visitors, nearing full normalization by reaching approximately 90% of its 2019 level. Japan also began to exceed its 2019 performance starting in Q3, totaling 3.653 million visitors in 2025—an 11.7% increase from the pre-pandemic figure of 3.272 million.

Taiwan and the United States also provided strong support for inbound growth. Taiwan rapidly overcame the temporary contraction caused by the pandemic to record 1.891 million visitors in 2025, a steep increase of 50.1% compared to 2019. Similarly, the U.S. maintained a steady upward trend, reaching 1.483 million visitors in 2025, representing a high growth rate of 42.1% over 2019.

2. Tourism Income: Total Surpasses 2019, but Per Capita Spending Falls Short

Explosive quantitative expansion did not translate into a proportional increase in profitability. While total tourism revenue in 2025 reached $21.89 billion (a 5.5% increase from 2019), the average expenditure per person stood at $1,155.8, failing to reach the 2019 level of $1,185.2.

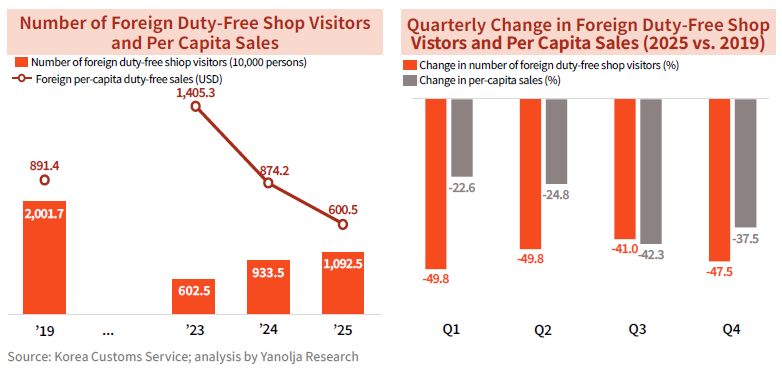

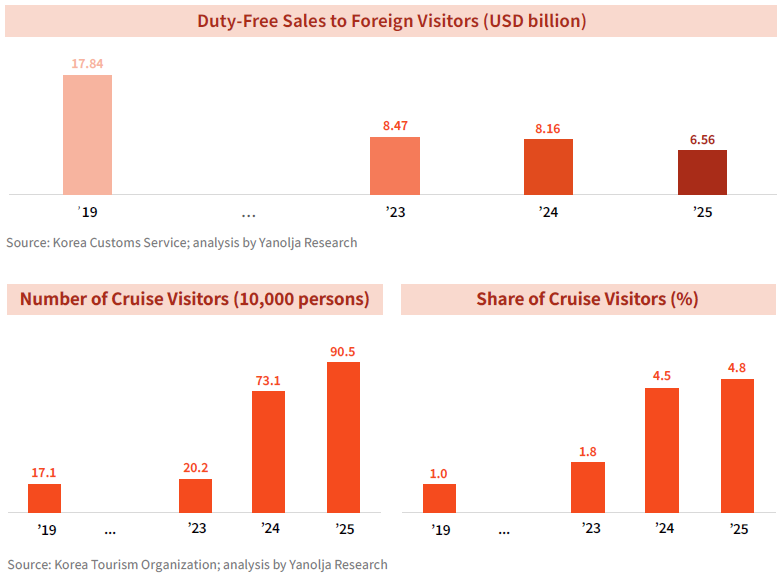

The primary cause for the decline in per-capita profitability is the structural slump in the duty-free sector due to changing consumer patterns. Both the number of foreign duty-free shoppers (10.925 million) and the average sales per person ($600) decreased significantly compared to 2019, causing total duty-free revenue to plummet from $17.84 billion to $6.56 billion. The widening negative growth in per-capita duty-free sales during the second half of the year (Q3: -42.3%, Q4: -37.5%) suggests that the traditional inbound profit model, which relied on "bulk shopping" by group tourists, has reached the end of its lifespan.

Additionally, the number of cruise tourists, which surged more than fivefold compared to 2019 (from 171,000 to 905,000, increasing their share from 1.0% to 4.8%), exerted downward pressure on average spending. Due to the nature of cruise travel—where visitors often stay for only half a day after disembarking—this sector contributed to the increase in total visitor volume but negatively impacted average tourism revenue.

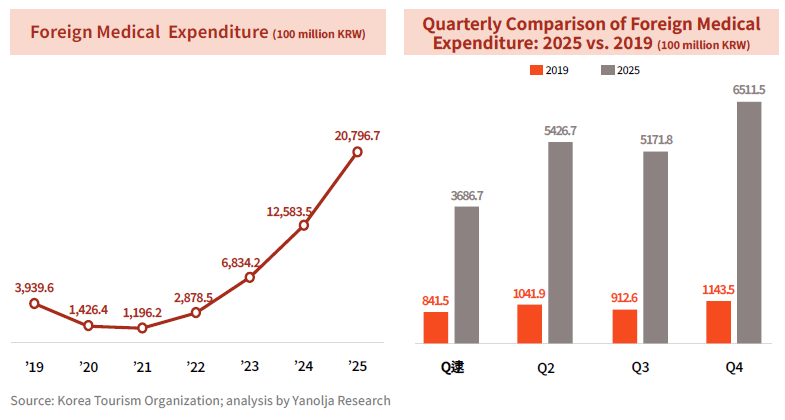

However, a positive signal emerged in the second half of the year as per-capita expenditure showed signs of a rebound, turning slightly positive (+2.4% and +3.1%) compared to 2019. The most powerful new growth engine driving this qualitative improvement is the explosive growth of high-value medical tourism. Foreign medical spending reached an all-time high of approximately 2.0796 trillion KRW in 2025, up from 393.96 billion KRW in 2019—a 5.3-fold increase. The quarterly spending growth compared to 2019 expanded even more sharply in the latter half of the year (from 338% in Q1 to 467% in Q3 and 469% in Q4). This proves that "high-end, locally immersive experience goods" like K-Medical are establishing themselves as a key breakthrough to offset the duty-free slump and lead the rebound in per-capita spending.

Outbound Tourism Performance

1. Outbound Travelers: Normalization Beyond Pent-up Demand and Concentration on Ultra-Short-Haul Destinations

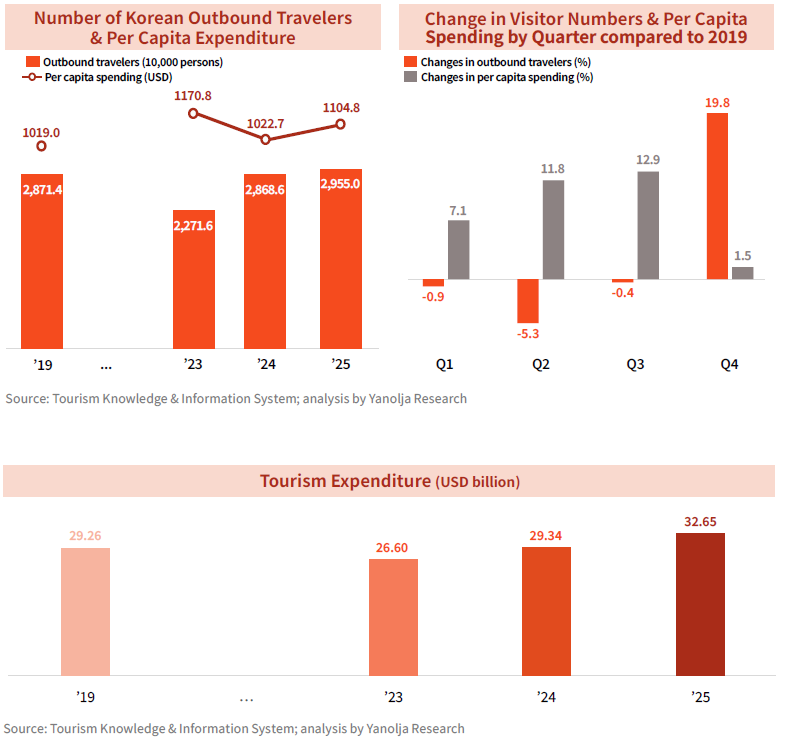

In 2025, the number of Korean outbound travelers was recorded at 29.55 million, surpassing the pre-pandemic 2019 figure (28.714 million) by 2.9%. By quarter, the market overcame a relatively weak first half and was driven to an annual increase by a 19.8% surge in Q4 compared to the same period in 2019. This proves that despite macroeconomic headwinds such as high inflation, the suppressed demand for overseas travel has entered a stage of stable normalization.

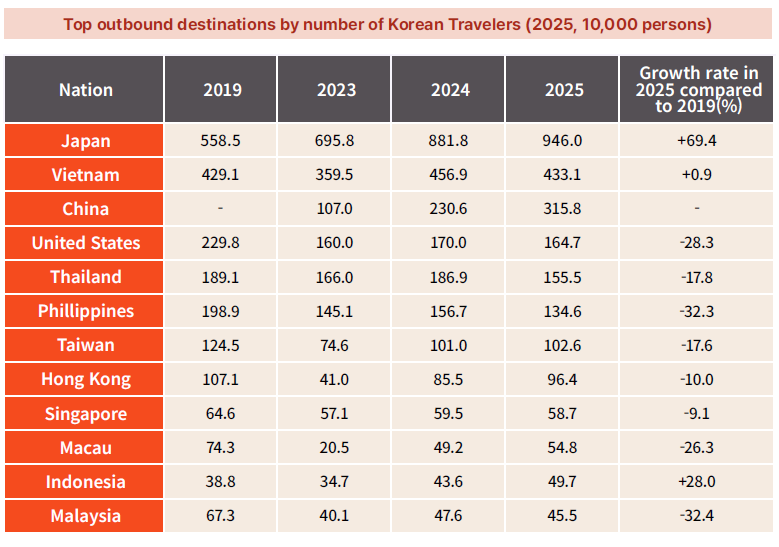

Regarding destination choice, there was a distinct "extreme concentration on ultra-short-haul destinations" and "polarization by country." In particular, visitors to Japan skyrocketed to 9.46 million in 2025, achieving a record growth of 69.4% compared to 2019 and single-handedly driving the outbound market. While Indonesia (0.497 million) and China (3.158 million) also showed clear upward trends, growth in Vietnam stagnated at 4.331 million (+0.9%). Conversely, major destinations such as the U.S. (-28.3%), the Philippines (-32.3%), Malaysia (-32.4%), Macau (-26.3%), Thailand (-17.8%), Taiwan (-17.6%), and Hong Kong (-10.0%) saw significant contractions, failing to close the gap with 2019 levels. This indicates that travelers are actively adopting a "cost-effectiveness strategy" by shortening travel distances to minimize the burden of high airfares.

2. Tourism Expenditure

In terms of tourism spending, the record-high number of departures combined with an increase in per-capita spending led to an explosive expansion of total overseas consumption. Per-capita expenditure rose from $1,019.0 in 2019 to $1,104.8 in 2025. Due to the impact of high exchange rates (averaging 1,423.3 KRW/$ in 2025), per-capita spending converted to Korean Won surged by more than 30% compared to 2019. Consequently, total tourism expenditure in 2025 reached $32.65 billion.

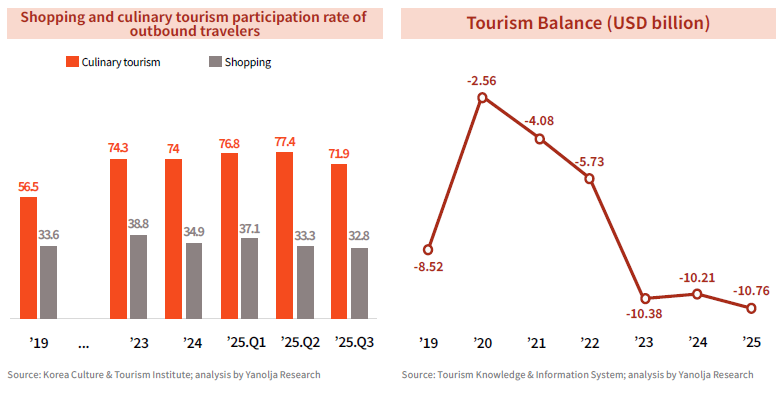

Although the growth rate of per-capita spending slowed slightly in Q4 (+1.5%), the overall upward trend is closely linked to shifts in travelers' "value consumption" patterns. According to Korea Culture & Tourism Institute, the proportions of gastronomy tourism (from 56.5% in 2019 to the 70% range in 2025) and shopping (from 33.6% in 2019 to 37.1% in Q1 2025) have expanded noticeably. In short, a clear behavioral pattern has emerged where travelers save on transportation costs by choosing nearby destinations and reinvest those savings into high-quality dining and shopping experiences locally.

Tourism Balance

2025 Performance: $10.7 Billion Deficit, Continuing the $10 Billion Deficit Streak for 3 Consecutive Years

While both inbound and outbound markets reached record-high volumes, the tourism balance deficit worsened due to the conflicting spending structures of falling inbound unit prices and expanding outbound expenditure. The annual tourism deficit in 2025 widened to -$10.76 billion, marking the third consecutive year of large-scale deficits exceeding $10 billion. This highlights that increasing the sheer number of visitors is insufficient to resolve the current structural imbalance and underscores the urgent need for a qualitative transition in the tourism industry.

Will China’s "Japan Travel Advisory" Provides a Practical Clue to Improving the Tourism Balance of South Korea?

Despite quantitative growth in inbound tourism, the stubborn tourism deficit remains a core challenge for the industry. Amidst this crisis, the diplomatic conflict between China and Japan that erupted in early November 2025 is reshaping the East Asian tourism landscape and emerging as a strategic variable for correcting the imbalance in the Korean tourism market. The Chinese government’s measures to discourage citizens from traveling to Japan has put the brakes on a previously thriving Japanese tourism sector. Chinese arrivals in Japan, which had been growing at over 20% year-on-year, plummeted by 45.3% in December to just 330,000 visitors.

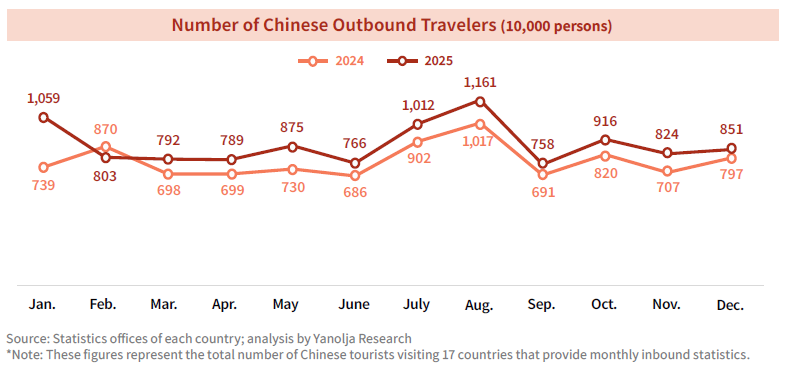

The notable point is that this massive displaced demand did not immediately migrate to other countries but instead remained adrift. In December 2025, total Chinese outbound travel demand (8.51 million) recovered to only 92% of October levels, showing a noticeable slowdown in recovery resilience compared to December 2024 (97% recovery). This suggests that despite the sharp drop in demand for Japan—their top destination—travelers were unable to immediately pivot to alternative locations due to the physical and psychological time lag required to switch travel infrastructure, such as flights and accommodations.

Even amidst this overall contraction in demand, it is estimated that Korea is already reaping some windfall benefits. The growth of Chinese tourists to Korea, which averaged 17.6% from January to October, expanded sharply to 26.9% in November and 28.4% in December. This culminated in a reversal in December, where the number of Chinese visitors to Korea surpassed those going to Japan. However, given that the situation only intensified in mid-November, it is premature to judge the total volume of these windfall benefits based solely on November and December 2025 data. Considering the time lag for switching bookings to alternative destinations, the actual ripple effect—where demand fleeing Japan flows into Korea—is likely to manifest more clearly in the Q1 2026 indicators, which include the Lunar New Year holiday in February. Therefore, if a robust influx of high-spending Chinese tourists is confirmed in the first quarter, it is expected to serve as a major turning point by raising the fallen per-capita expenditure and alleviating the chronic tourism balance deficit.