Korea’s Inbound and Outbound Tourism Performance in the First Half of 2025

Inbound Tourism: Record-High Visitor Numbers, But Tourism Revenue Falls Short of Expectations

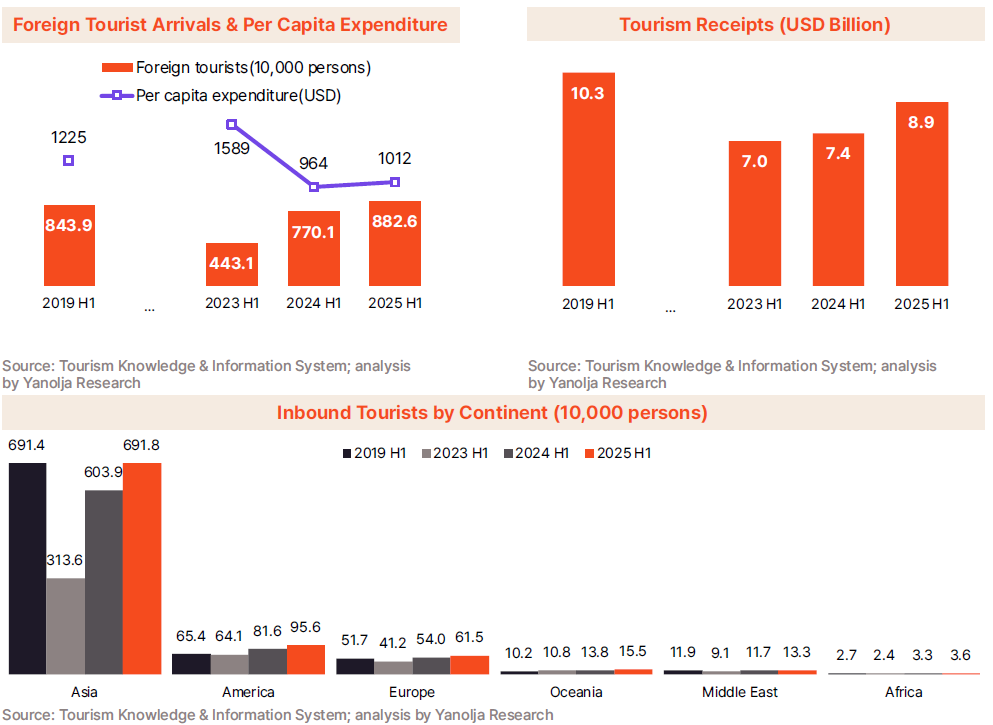

· In the first half of 2025, the number of foreign tourists visiting Korea reached approximately 8.826 million, a 4.6% increase compared to the same period in 2019 (8.439 million) before the pandemic, marking an all-time high. Compared to 2024 (7.701 million), this was a 14.6% increase, showing that Korea’s inbound tourism market has not only recovered from the pandemic shock but has also entered a growth phase.

· Recovery varied significantly across regions. Asia was the slowest to rebound. Arrivals plunged from 6.914 million in the first half of 2019 to 3.136 million in 2023, making Asia the region most heavily impacted by COVID-19. However, arrivals surged to 6.039 million in 2024 and 6.918 million in 2025, slightly surpassing pre-pandemic levels. In contrast, the Americas recovered the fastest: from 654,000 in 2019 to 816,000 in 2024, and 956,000 in 2025—a 46.2% increase compared to 2019. Europe also grew by 18.8% compared to 2019, while Oceania, the Middle East, and Africa increased by 51.5%, 12.3%, and 32.7%, respectively, though their absolute numbers remain smaller.

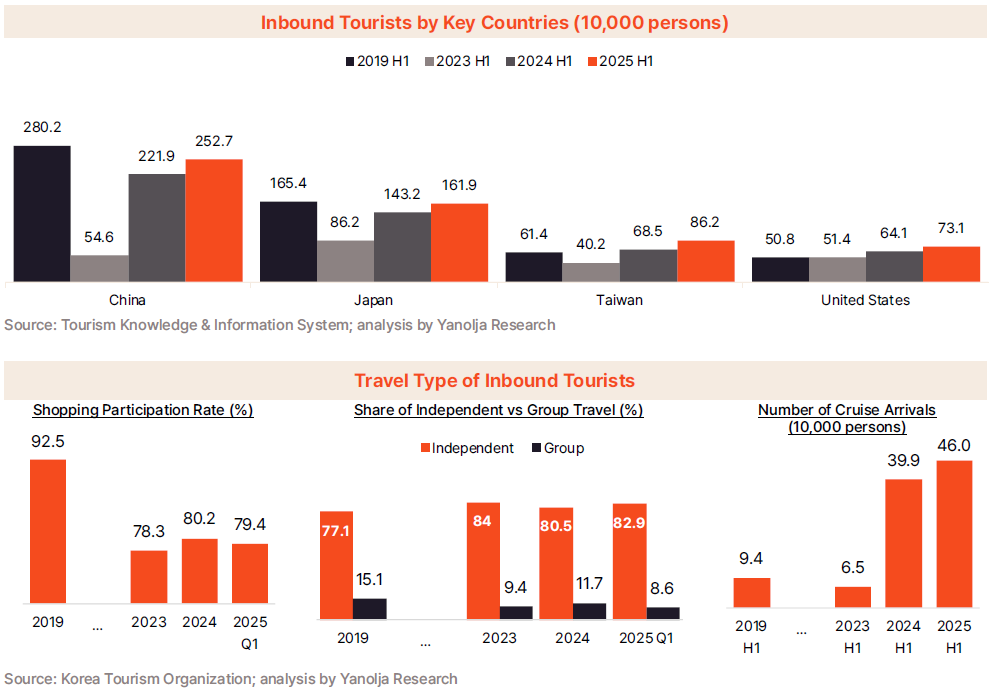

· By country, China remained Korea’s largest inbound market. Visitor numbers dropped from 2.802 million in 2019 to 546,000 in 2023, but rebounded to 2.219 million in 2024 and further to 2.527 million in 2025, maintaining its position as the core market. Japan fell from 1.654 million in 2019 to 862,000 in 2023, but recovered to 1.432 million in 2024 and 1.619 million in 2025, nearly regaining pre-pandemic levels. Taiwan declined from 614,000 in 2019 to 402,000 in 2023, but rose to 685,000 in 2024 and 862,000 in 2025—40.4% higher than 2019. The United States (508,000 in 2019) quickly rebounded, climbing from 514,000 in 2023 to 641,000 in 2024 and 731,000 in 2025, representing a 43.7% increase from 2019.

· However, the increase in visitor numbers did not translate into a proportional rise in tourism revenue. In the first half of 2019, 8.439 million tourists generated USD 10.34 billion in tourism receipts, with an average per capita expenditure of USD 1,225. By 2023, despite arrivals falling to nearly half of 2019 levels, per capita spending surged to USD 1,589, resulting in receipts of USD 7.04 billion. In 2024, tourist arrivals recovered sharply to 7.7 million, but per capita spending plummeted to USD 964, keeping receipts at USD 7.43 billion. In 2025, despite record-high arrivals (8.826 million), per capita spending was only USD 1,012—17.4% lower than in 2019—and total receipts stood at USD 8.94 billion, 13.6% below 2019 levels. This indicates that while Korea’s inbound tourism achieved quantitative growth in visitor numbers, it faced limits in qualitative spending growth.

· The decline in receipts reflects structural changes in visitor composition and travel behavior before and after the pandemic. According to the Ministry of Culture, Sports and Tourism’s Foreign Visitor Survey, the share of tourists citing shopping as a major activity dropped significantly from 92.5% in 2019 to 80.2% in 2024, and further to 79.4% in Q1 2025. Travel formats also shifted: independent travel rose from 77.1% in 2019 to 80.5% in 2024, and 82.9% in Q1 2025, while group travel fell from 15.1% to 11.7% and then to 8.6% over the same period. Independent travelers have greater flexibility but typically spend less at duty-free shops, on tour buses, and at designated restaurants, resulting in lower overall expenditures. Additionally, the number of cruise passengers—who tend to be short-stay visitors with limited spending—soared with the resumption of Chinese cruise operations: from 94,000 in 2019 and 65,000 in 2023 to 399,000 in 2024 and 460,000 in 2025, further contributing to weaker tourism receipts.

Outbound Tourism: Both Tourist Numbers and Spending Increase, Widening the Tourism Deficit

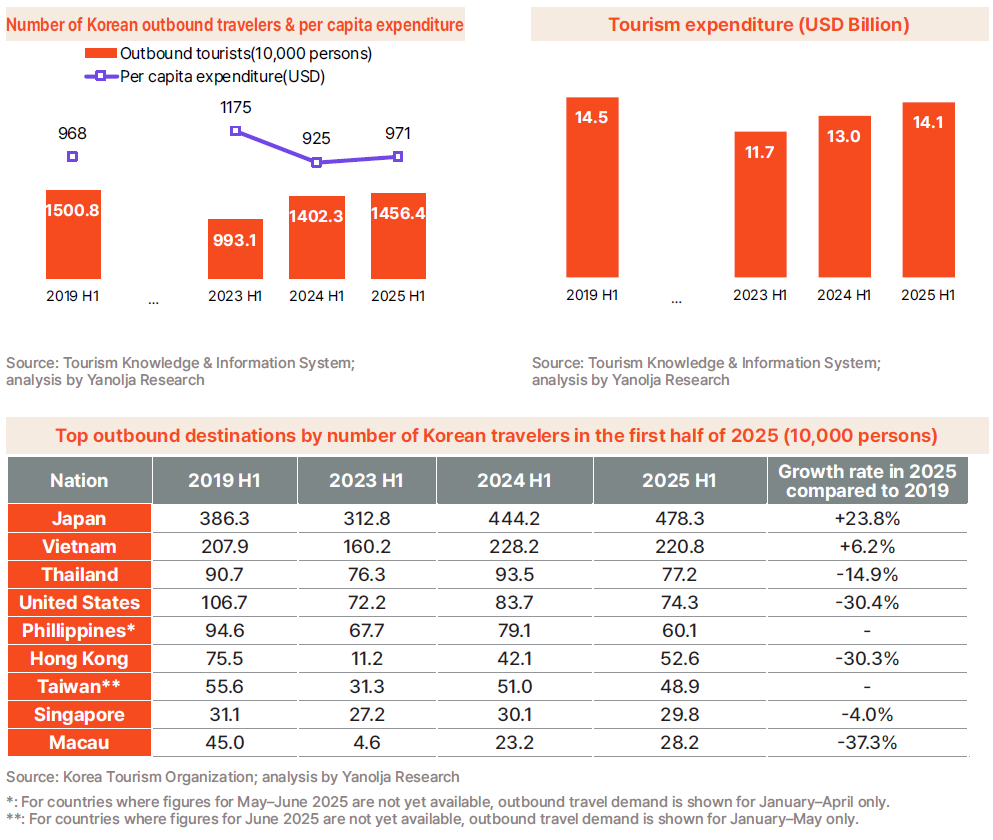

· In the first half of 2025, the number of Koreans traveling abroad was estimated at 14.564 million, nearly returning to pre-pandemic levels. This represented a 3.9% increase from 14.023 million in 2024, indicating that the pent-up demand for overseas travel following COVID-19 is gradually becoming entrenched. Immediately after the pandemic, outbound travel had dropped to 9.931 million in the first half of 2023—33.8% lower than the 15.008 million recorded in 2019. However, the number surged by 41.2% in 2024, and by 2025, it had recovered to just 3.0% below 2019 levels, effectively regaining pre-pandemic scale.

· By region, Asia showed particularly strong outbound growth, with Japan standing out the most. Excluding countries like China where detailed statistics are unavailable, Japan saw outbound numbers drop from 3.863 million in the first half of 2019 to 3.128 million in 2023, before rebounding to 4.442 million in 2024 and 4.783 million in 2025—23.8% higher than in 2019. Vietnam also exceeded pre-pandemic levels, rising from 2.079 million in 2019 to 2.282 million in 2024, and recording 2.208 million in 2025—6.2% higher than in 2019.

· In contrast, destinations such as Thailand, the United States, Hong Kong, Taiwan, and Macau showed declines. Thailand recovered from 907,000 in 2019 to 935,000 in 2024, but fell back to 772,000 in 2025 (–14.9% compared to 2019). The U.S. saw 1.067 million Korean visitors in 2019, but only 837,000 in 2024 and 743,000 in 2025 (–30.4% compared to 2019). Hong Kong dropped from 755,000 in 2019 to 421,000 in 2024 and 526,000 in 2025, remaining –30.3% below 2019. Taiwan rebounded from 556,000 in 2019 to 510,000 in 2024, but reached only 489,000 by May 2025, staying close to pre-pandemic levels. Macau experienced a sharp fall, from 450,000 in 2019 to 232,000 in 2024 and 282,000 in 2025.

· More notable than the growth in traveler numbers was the faster rise in outbound spending. In the first half of 2019, overseas tourism expenditure totaled USD 14.53 billion. In 2023, although outbound travelers fell by 33.8% compared to 2019, total spending declined by only 19.0% to USD 11.67 billion, thanks to a surge in per capita spending from USD 968 to USD 1,175. In 2024, the number of travelers jumped to 14.023 million, but per capita spending fell to USD 925, keeping total spending at USD 12.98 billion. In 2025, with 14.564 million travelers and per capita spending rebounding slightly to USD 971, total outbound expenditure expanded to USD 14.14 billion.

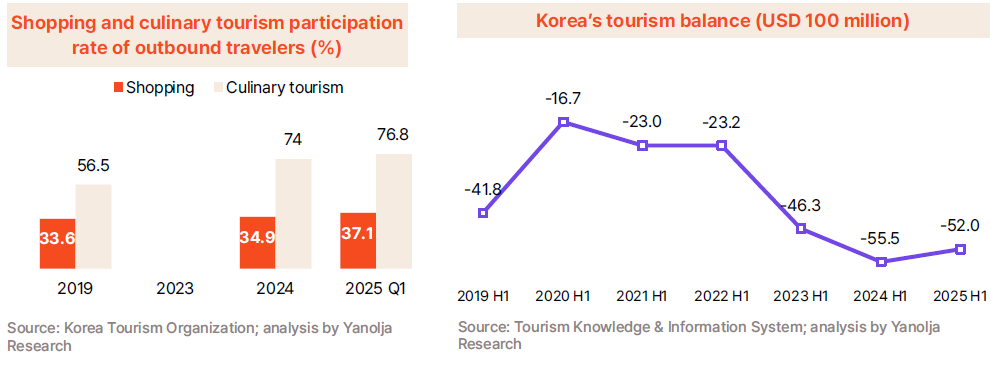

· The rapid increase in outbound spending reflects not only exchange rate effects but also changes in travel behavior. According to the Ministry of Culture, Sports and Tourism’s National Travel Survey, participation in culinary tourism and shopping abroad expanded significantly. The share of travelers citing gastronomy as a major activity jumped from 56.5% in 2019 to 74.0% in 2024, and further to 76.8% in Q1 2025. Shopping also rose from 33.6% in 2019 to 38.8% in 2023, and remained higher than pre-pandemic levels at 34.9% in 2024 and 37.1% in Q1 2025

· While inbound receipts stagnated, outbound expenditure surged, preventing any improvement in the tourism balance. Korea’s tourism balance stood at –USD 4.18 billion in the first half of 2019, but the deficit widened to –USD 4.63 billion in 2023, –USD 5.55 billion in 2024, and –USD 5.20 billion in 2025, solidifying a structural deficit. This reflects the combined effect of weak inbound consumption and strong outbound spending growth.

Chinese Group Tourism: Will Visa-Free Entry Be the Key to Reviving Tourism Revenue?

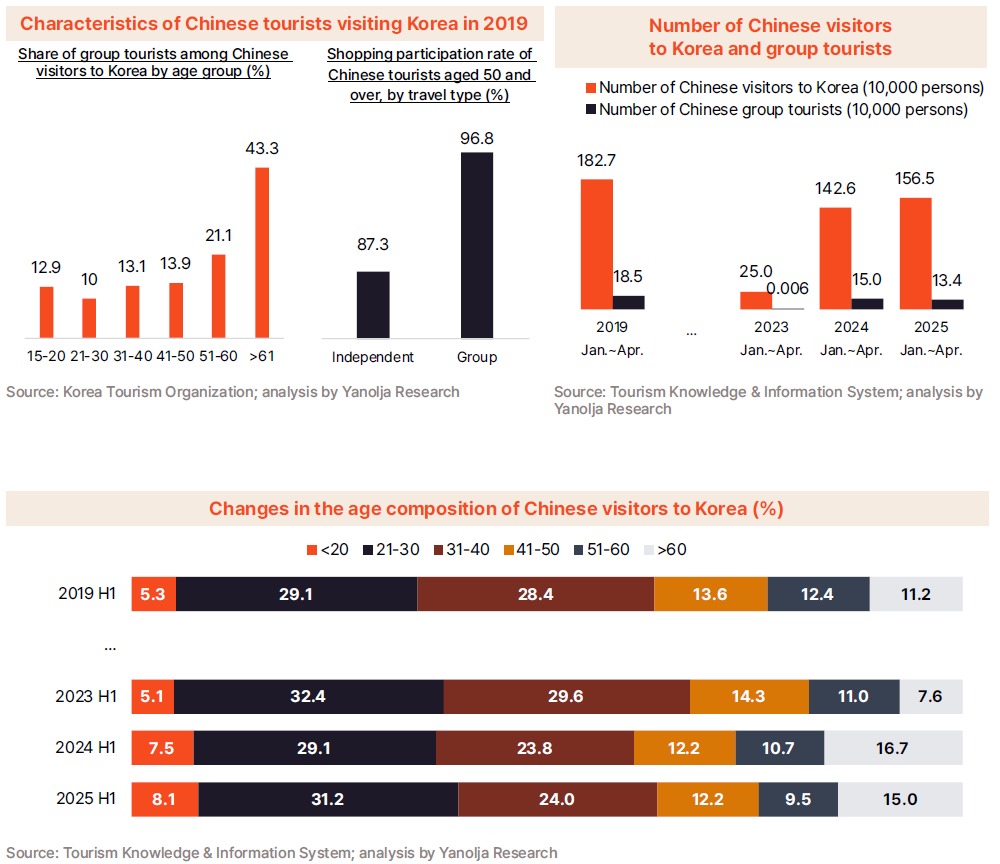

· Despite inbound tourism to Korea reaching a record high in visitor numbers in the first half of 2025, tourism revenue has yet to recover to 2019 levels. A major factor behind this is the sluggish recovery of the Chinese group tourism market. Traditionally, Chinese group travelers have been dominated by middle-aged and older cohorts, whose stable income and purchasing power translated into high spending on chartered buses, group tours, and shopping. In the 2019 Foreign Visitor Survey, 21.1% of Chinese group tourists were in their 50s and 43.3% were 61 or older, far higher than the 10–13% share for those in their 20s–40s. Moreover, the shopping participation rate among Chinese group tourists aged 50 and above was 96.8%, compared to 87.3% among independent travelers. This illustrates that Chinese group tourism was a crucial pillar supporting Korea’s tourism revenue.

· However, the delayed recovery of group tourism since COVID-19 has eroded this consumption base. The number of Chinese group tourists stood at 185,000 in January–April 2019, but collapsed to just 55 in 2023. It rebounded to 150,000 in 2024, yet slipped back to 134,000 in 2025, which was 27.3% below 2019 levels. By comparison, total Chinese visitors to Korea were down 14.3% from 2019. Age composition also shifted: the share of younger independent travelers aged 21–30 rose from 29.1% in 2019 to 31.2% in 2025, while the share of higher-spending 40–60-year-olds declined steadily from 26.0% in 2019 to 25.3%, 22.9%, and 21.7% in subsequent years.

· Starting September 29, 2025, visa-free entry for Chinese group tourists will be implemented, potentially changing the outlook in the second half of the year. The return of Chinese group tourism could serve not only to boost visitor numbers but also to act as a direct catalyst for tourism revenue recovery. The extent of recovery and spending behavior among these tourists will determine whether Korea’s tourism receipts rebound. If spending patterns remain similar to pre-COVID levels, revenues could improve in the second half. However, structural constraints such as China’s economic conditions, shifting consumer trends, the rise of online duty-free and cross-border e-commerce, and exchange rate factors may limit the rebound. Visa-free entry for Chinese group tourists could thus mark not just a quantitative expansion but a turning point for qualitative recovery in consumption patterns, making the second half of 2025 a potential inflection point for Korea’s tourism performance.

· The first half of 2025 marked an important turning point for Korean tourism. This was the period when both inbound and outbound visitor numbers returned to pre-pandemic levels. However, the underlying structural issues of Korea’s tourism industry remain unresolved. Inbound tourism revenue has declined, while outbound spending has risen significantly, leaving the tourism deficit unimproved. Of particular concern is that per capita spending by inbound visitors is still well below pre-COVID levels, highlighting that low-value mass tourism continues to dominate. Structural issues—such as the lack of high-value-added tourism products and the heavy concentration of short-stay trips in Seoul and the capital region—remain urgent challenges

· Whether voluntarily or not, Koreans have already become adept at overseas travel. Without institutional measures to balance this trend, outbound tourism cannot be contained. Therefore, policymakers must recognize that the fastest route to restoring balance in the tourism account lies in stimulating domestic tourism among Koreans and boosting inbound demand from foreigners. Korea should take a lesson from Japan, which until 2014 had inbound visitor numbers similar to Korea’s but quickly transformed from a chronic tourism deficit country to a surplus nation.