South Korea’s lodging industry in Q1 2026 showed overall year-over-year improvement across most accommodation categories; however, the pace of recovery varied significantly by property type and region. In particular, inbound-sensitive segments—including 5-star hotels, 3-star hotels, vacation rentals, and resorts—recorded increases in Revenue per Available Room (RevPAR), whereas pensions and budget hotels, which rely more heavily on domestic leisure demand, continued to underperform. These results indicate a widening polarization within the lodging sector.

Yanolja Research, a travel and tourism industry research institute led by Dr. SooCheong (Shawn) Jang, released its Q1 2026 Quarterly Trends in the Korea Lodging Industry on April 29, based on proprietary market data and a nationwide operator survey. The report analyzes performance trends across hotels, motels, pensions, and vacation rentals, while also examining how the recent surge in Chinese inbound demand following China’s so-called “Anti-Japan Restrictions” has been perceived within the domestic lodging market.

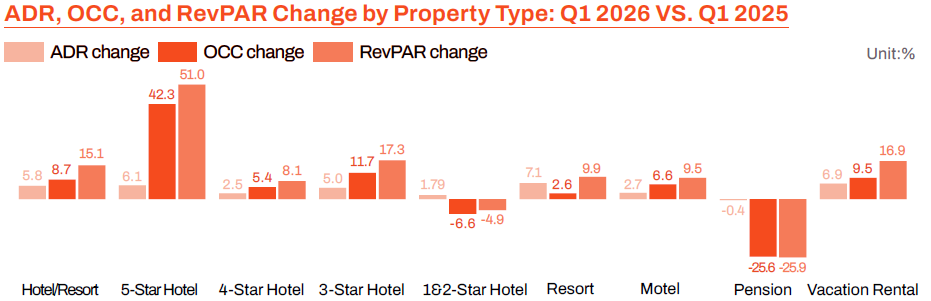

According to the report, the strongest performance growth in Q1 2026 was recorded by the 5-star hotel segment. Occupancy rate (OCC) increased 42.3% year-over-year, while RevPAR rose 51.0%. The data suggest that performance improvement was driven less by rate inflation and more by demand recovery—particularly expanding demand from international visitors for upscale accommodations.

RevPAR growth by accommodation type was as follows: 3-star hotels (+17.3%), vacation rentals (+16.9%), resorts (+9.9%), motels (+9.5%), and 4-star hotels (+8.1%). In particular, both ADR and OCC improved simultaneously in the 3-star hotel and vacation rental segments, indicating recovery momentum within the midscale and alternative accommodation markets. Motels also demonstrated demand-driven improvement, with OCC growth contributing more significantly than ADR increases.

In contrast, the pension segment recorded the steepest decline, with RevPAR falling 25.9% year-over-year. Although Average Daily Rate (ADR) declined only 0.4%, OCC dropped 25.6%, indicating that weakening demand—not pricing pressure—was the principal driver of deteriorating performance. Re

vPAR for 1–2 star hotels also declined 4.9%. These findings imply that the current recovery cycle is not broad-based across the lodging industry, but rather concentrated in accommodation types with stronger exposure to inbound tourism demand.

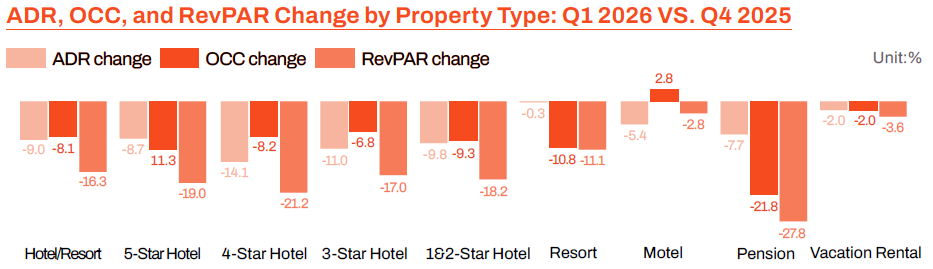

Compared with Q4 2025, the domestic lodging market entered a broad correction phase in Q1 2026 due to seasonal off-peak effects. RevPAR declined across all accommodation categories, while hotel RevPAR fell between 17.0% and 21.2% across all star grades.

Nevertheless, the outlook for Q2 remains comparatively positive. According to Yanolja Research’s Lodging Business Outlook Index, both hotel and motel operators expect simultaneous increases in ADR and OCC, with all forward-looking indicators exceeding the neutral benchmark of 100. Most notably, the motel OCC outlook index reached 129.2—the highest among all indicators surveyed—reflecting strong expectations for recovery in short-stay and regional travel demand during the spring leisure season.

Kwanyoung Lee, Associate Research Fellow at Yanolja Research, commented:

“While Q1 2026 confirmed a year-over-year recovery trajectory, quarter-over-quarter performance clearly reflected the effects of seasonal low demand. In particular, upscale hotels and vacation rentals linked to inbound demand maintained relatively resilient performance, whereas pensions experienced sharper deterioration due to weakening domestic leisure demand and seasonality, widening the performance gap across accommodation types.”

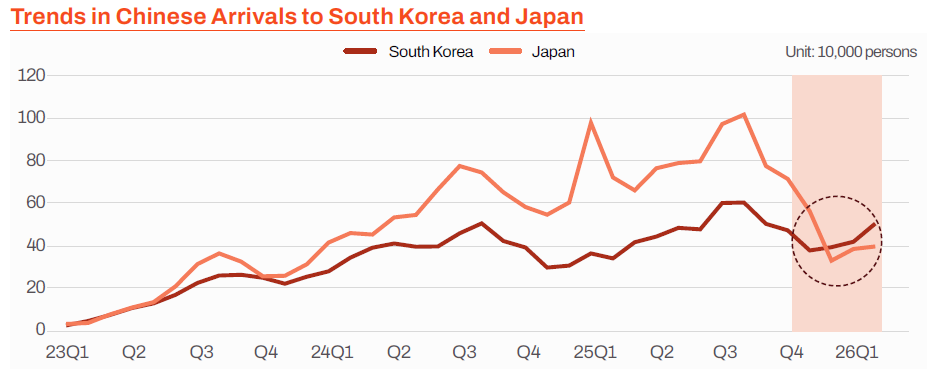

The report also highlights diverging tourism demand trends between Korea and Japan following China’s informal “Anti-Japan Restrictions” introduced in November 2025. In December 2025, Chinese arrivals to Korea reached 394,000, surpassing Chinese arrivals to Japan at 330,000. On a combined January–February basis, Chinese arrivals to Korea increased 31% year-over-year, whereas Chinese arrivals to Japan declined 54%. These trends suggest that a portion of Chinese outbound demand originally destined for Japan may have shifted toward Korea.

However, Professor Kyuwan Choi of Kyung Hee University cautioned against attributing the trend solely to geopolitical factors:

“It is still premature to isolate this trend as a pure effect of the China–Japan restrictions. Q1 includes the Lunar New Year holiday season, and Chinese demand also appears concentrated in specific accommodation types and destinations. Additional quarters of observation are necessary before drawing definitive conclusions.”

Although macro-level indicators confirm increased Chinese inbound demand, perceived benefits varied significantly across accommodation types and regions. In Q1 2026, 28.3% of hotel operators reported increased Chinese bookings, compared with only 10.4% of motel operators, indicating that the recovery impact was concentrated primarily within the hotel sector.

Regionally, perceived demand growth was strongest in major tourism and gateway cities, including Busan (39.1%), Seoul (35.6%), Incheon (30.0%), and Jeju (20.8%). By property type, the strongest concentration appeared among hotels in major entry hubs, including Incheon hotels (60.0%), Busan hotels (46.2%), and Seoul hotels (45.8%), suggesting that accessibility to international airports and ports played a critical role. In contrast, spillover effects remained limited in non-metropolitan regions such as Gangwon and Gyeongnam–Ulsan.

Hyo Won Yoon, Senior Researcher at Yanolja Research, explained:

“Current Chinese inbound demand is concentrated in destinations combining airport accessibility, upscale lodging infrastructure, and major tourism content. To expand the practical economic benefits to regional lodging markets, transportation accessibility improvements—such as establishing direct international routes connecting regional airports with major neighboring cities—will be necessary.”

Chinese visitor demand was overwhelmingly concentrated among FIT travelers (Free Independent Travelers, 1–3 persons), accounting for 76.0% of all responses. In contrast, small groups accounted for 35.0%, business travelers 10.0%, and large group tours only 8.0%. These results indicate that recent growth in Chinese inbound demand differs structurally from previous demand cycles dominated by large-scale group tourism, instead reflecting a shift toward small-scale independent travel.

Dr. SooCheong (Shawn) Jang, Director of Yanolja Research, stated:

“The increase in Chinese inbound demand presents a significant opportunity for Korea’s tourism industry. However, if the benefits remain concentrated in a limited number of upscale accommodations and major metropolitan cities, it will be difficult for the industry as a whole to establish sustainable growth momentum. Future policy priorities should extend beyond simply increasing inbound arrivals toward improving regional accessibility, differentiating accommodation strategies by property type, and upgrading regional tourism content in order to distribute inbound demand more broadly across the national lodging market.”